Bonus Depreciation Real Estate 2026: How to Use 100% Write-Off, Cost Segregation, and REP Strategies to Reduce Taxes and Build Wealth

Bonus Depreciation

for Real Estate in 2026:

The Ultimate Guide to Cost Segregation, REP Status, and 100% Tax Write-Off Strategy

As of 2026, 100% bonus depreciation in real estate has been permanently restored under the One Big Beautiful Bill Act (OBBBA), eliminating the old phase-down schedule and giving qualifying investors a path to full first-year write-offs on eligible components identified through cost segregation.

Most guides on bonus depreciation are written by accountants who do not buy real estate, or by investors who do not fully understand the bigger tax-planning picture. My background spans both. Before transitioning into real estate full-time, I spent over a decade in wealth management and financial planning, ultimately serving as a Director of Wealth Management. I hold the Certified Residential Specialist (CRS) designation — the highest credential awarded in residential real estate — and my work has been featured in the Wall Street Journal, MarketWatch, MSN Money, and Morningstar.

Bonus depreciation real estate 2026 is one of the most important tax strategy topics investors should understand right now. With 100% bonus depreciation restored under current law, the combination of cost segregation, Real Estate Professional status, and short-term rental strategy can create significant first-year write-offs for qualifying investors.

I have personally applied bonus depreciation strategies across my own long-term and mid-term rentals, modeling different tax scenarios and working alongside CPAs to ensure alignment with broader financial planning goals.

Bonus depreciation in real estate allows investors to deduct a large portion of a property's value in the first year by accelerating depreciation through a cost segregation study. In 2026, qualifying assets can be written off at 100% in Year 1 under current tax law.

"One of the biggest misconceptions I see is that bonus depreciation is only useful for short-term rentals. I have personally applied this strategy to my own long-term rentals — structuring acquisitions, leveraging cost segregation, and using depreciation to meaningfully reduce taxable income while still building equity, cash flow, and long-term upside."

— Eric Ravenscroft, CRSBonus depreciation is one of the most powerful tools available to real estate investors and professionals. For me, this is not just something I explain in theory. It is a strategy I actively study, model, and apply through the lens of real estate, financial planning, and tax strategy. And as of 2026, the rules have changed permanently — for the better.

Section 01What Is Bonus Depreciation?

Bonus depreciation — governed by IRC §168(k) — allows real estate investors to accelerate depreciation deductions on qualifying property, taking the full deduction in the first year the asset is placed in service, rather than spreading it across 27.5 years (residential) or 39 years (commercial).

Instead of deducting $10,000/year for 27 years on a $275,000 property improvement, you deduct the eligible portion in Year 1 — dramatically reducing your taxable income now, not over three decades.

What qualifies for bonus depreciation?

The structure of a building (walls, roof, foundation) follows the standard depreciation schedule. A cost segregation study identifies and reclassifies components into shorter-lived categories under the IRS MACRS framework:

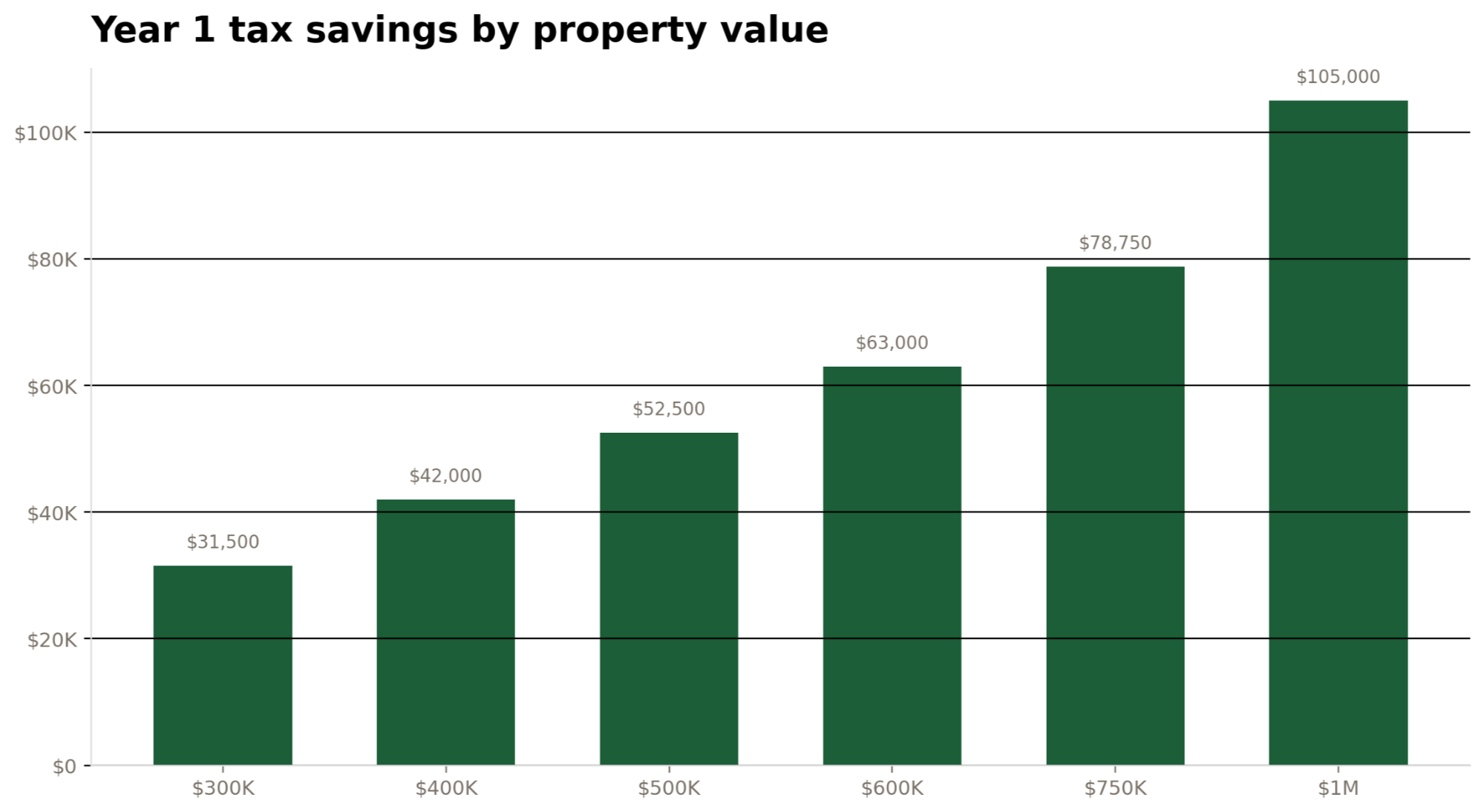

Buy a $500,000 rental → identify roughly $150,000 of bonus-eligible components through cost segregation → apply 100% bonus depreciation → at a 35% rate, that could translate to about $52,500 in potential Year 1 tax savings.

What qualifies for bonus depreciation in real estate?

| Asset Type | Eligible for Bonus Depreciation? |

|---|---|

| Appliances, flooring, fixtures | ✓ Yes (5-year property) |

| Furniture for STRs or MTRs | ✓ Yes (7-year property) |

| Landscaping, fencing, driveways, outdoor lighting | ✓ Yes (15-year improvements) |

| Building structure | ✗ No (27.5-year residential property) |

| Primary residence | ✗ No |

The 2026 Update: The One Big Beautiful Bill Made It Permanent

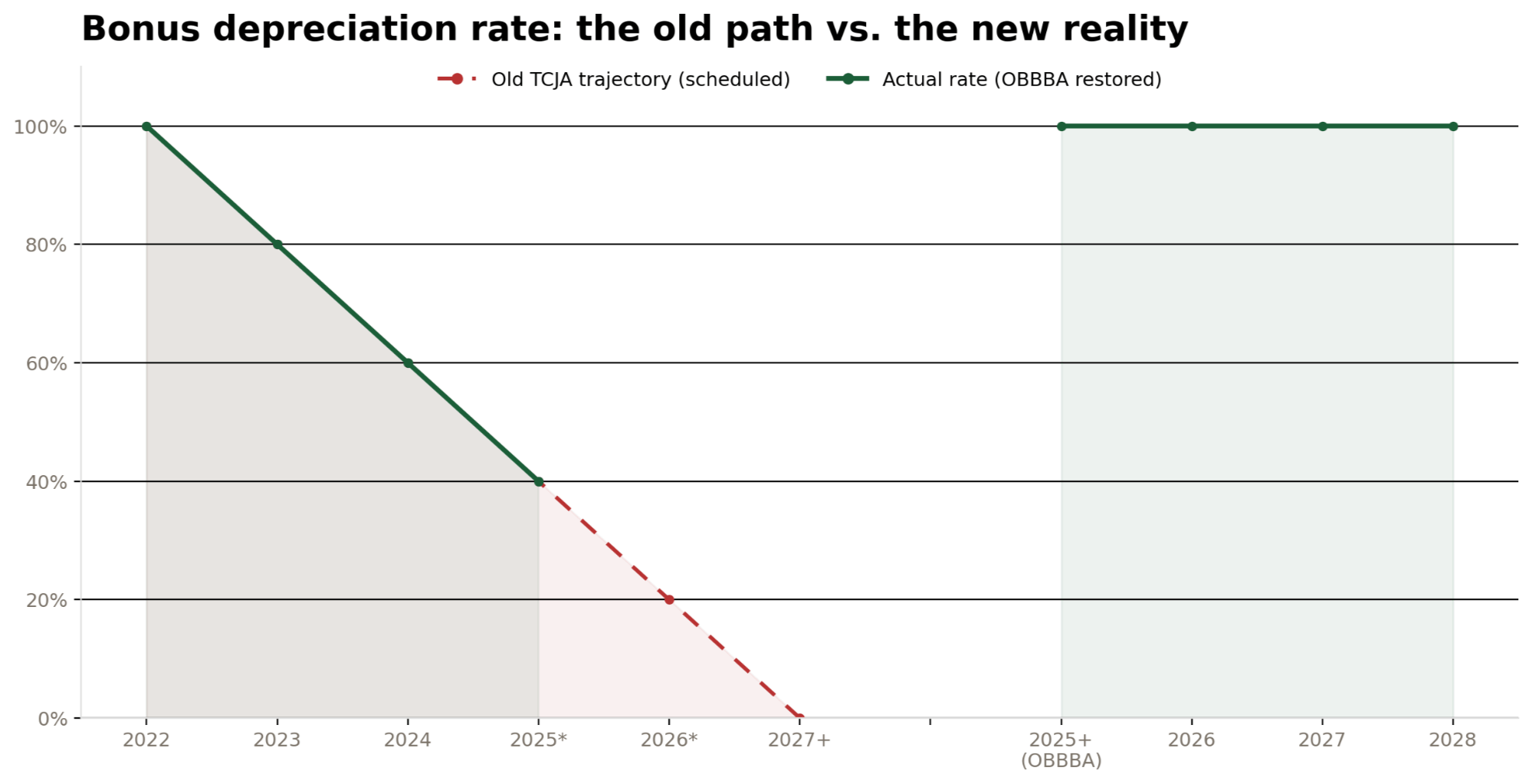

Under the Tax Cuts and Jobs Act (TCJA), bonus depreciation was always temporary — set to phase down by 20 percentage points per year until fully expiring in 2027. Investors watched the clock. Then on July 4, 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law, permanently restoring 100% bonus depreciation for qualifying property acquired after January 19, 2025.

2025

2025

What the OBBBA changed

- ✓

Eliminated the phase-down schedule entirely — 100% is now the floor, not the ceiling

- ✓

Removed placed-in-service deadlines — no more year-end scramble to close

- ✓

Maintained all existing TCJA qualification criteria unchanged

- ✓

Added qualified sound recording productions as eligible property

- →

Introduced a transition-year election to take 40% (or 60% for certain property) instead of 100% when strategically beneficial

IRS Notice 2026-11: What You Actually Need to Know

On January 14, 2026, the IRS issued Notice 2026-11, providing interim guidance on applying the OBBBA rules. Three things matter most for real estate investors:

The IRS uses the binding contract date to determine when property is "acquired." A contract signed after January 19, 2025 qualifies for 100% bonus depreciation — even if you closed months later. A contract signed before that date may only qualify for the old 40% rate. Keep your purchase agreements meticulously documented.

The Component Election

For self-constructed or renovated properties, you can elect to treat individual components as eligible for bonus depreciation as they're placed in service — even if the overall project started before January 20, 2025. This is especially valuable for phased developments, renovation projects, and multi-unit properties with staggered improvements.

When to elect a lower rate

Taking 100% bonus depreciation isn't always optimal. If you have significant net operating losses (NOLs), or if your state doesn't conform to federal bonus depreciation rules (see Section 10 for Arizona specifics), electing 40% may produce a better combined federal + state outcome. Model both scenarios before filing.

Section 04How Cost Segregation Unlocks Bonus Depreciation

A cost segregation study is an engineering and tax analysis that breaks down your investment property into its component parts and assigns each the correct IRS asset class. Without one, everything defaults to the 27.5-year residential bucket. With one, you reclassify 30–40% of your property value into categories eligible for 100% bonus depreciation.

Studies typically run $3,000–$8,000 depending on property size and complexity. On a $500K property generating $50,000+ in Year 1 federal savings, the study pays for itself many times over — often within a single quarterly estimated tax payment.

Who Qualifies — The Full Breakdown

There are two primary investor profiles that determine how bonus depreciation can be used. The type of rental you own and your IRS classification together determine whether losses can offset active income.

| Requirement | All Investors |

|---|---|

| Binding contract signed after Jan. 19, 2025 | Required |

| Property placed in service (available for rent) | Required |

| Cost segregation study performed | Required to identify bonus-eligible components |

| Property used in trade/business or for income production | Required — primary residences do not qualify |

| Form 4562 filed with tax return | Required |

The Real Estate Professional Advantage: LTR, MTR, and STR

This is the section that separates sophisticated investors from everyone else. Under IRC §469(c)(7), a Real Estate Professional (REP) must meet two tests in a given tax year:

- ✓

750+ hours spent in real property trades or businesses in which they materially participate

- ✓

More than 50% of total personal services during the year performed in real property trades or businesses

Why REP status is a game-changer: passive vs. non-passive

For non-REPs, rental losses are passive under IRC §469 — they can only offset passive income. Excess losses are suspended and carried forward.

When you qualify as a REP and materially participate in your rentals, those rentals become non-passive. Bonus depreciation losses flow directly against your active income — commissions, W-2, business revenue, or a spouse's income.

(30+ day avg. stay)

(8–29 day avg. stay)

(≤7 day avg. stay)

Non-passive — offsets all income

Non-passive — offsets all income

Non-passive — offsets all income

Passive — suspended losses only

Passive — suspended losses only

Non-passive if avg. stay ≤7 days

A physician buying a mid-term rental generates passive losses — usable against passive income only. A real estate agent buying the same property, with REP status, generates non-passive losses that directly reduce their commission income. Same property, $28,000+ difference in Year 1 taxes.

Material participation tests (any one qualifies)

Even as a REP, you must materially participate in each rental property. Under IRS Temp. Reg. §1.469-5T, you satisfy material participation if you meet any one of seven tests — the most common for landlords is logging 100+ hours per year with no single other person spending more hours than you. Keep a contemporaneous log.

Section 07Non-Real Estate Professionals: The STR Path

If you're a high-income W-2 earner — physician, attorney, software engineer, executive — and you don't qualify as a REP, you still have a direct path to bonus depreciation through short-term rentals (STRs) with material participation.

Under IRS Publication 925, a rental where the average period of customer use is 7 days or fewer is not classified as a rental activity under the passive activity rules. It's treated as an active business — meaning losses flow against active income if you materially participate (typically, the 100-hour test).

If your AGI is under $100,000, you may qualify for the $25,000 special rental loss allowance even without REP status. This phases out completely at $150,000 AGI. Most high-income earners reading this guide are above that threshold — making the STR + material participation strategy the primary vehicle.

Can Bonus Depreciation Offset W-2 Income?

This is one of the most common questions I get — and one of the most misunderstood parts of the strategy.

The answer depends on how your rental is classified. The tax outcome is not driven solely by the property. It is driven by the combination of property type, average stay length, material participation, and whether you qualify for Real Estate Professional status.

- ✓

Real Estate Professional (REP): qualifying long-term, mid-term, and short-term rental losses can potentially offset active income, including commissions or W-2 income

- ✓

Short-Term Rental (7 days or fewer average stay): can potentially offset W-2 income if you materially participate, even without REP status

- →

Long-term or mid-term rental without REP status: typically remains passive, meaning losses are generally suspended and carried forward

This is the difference between saving little or nothing in Year 1 and potentially saving $25,000 to $50,000+ in taxes. Same market. Similar property. Completely different outcome depending on classification and participation.

Full Math Examples: Three Scenarios

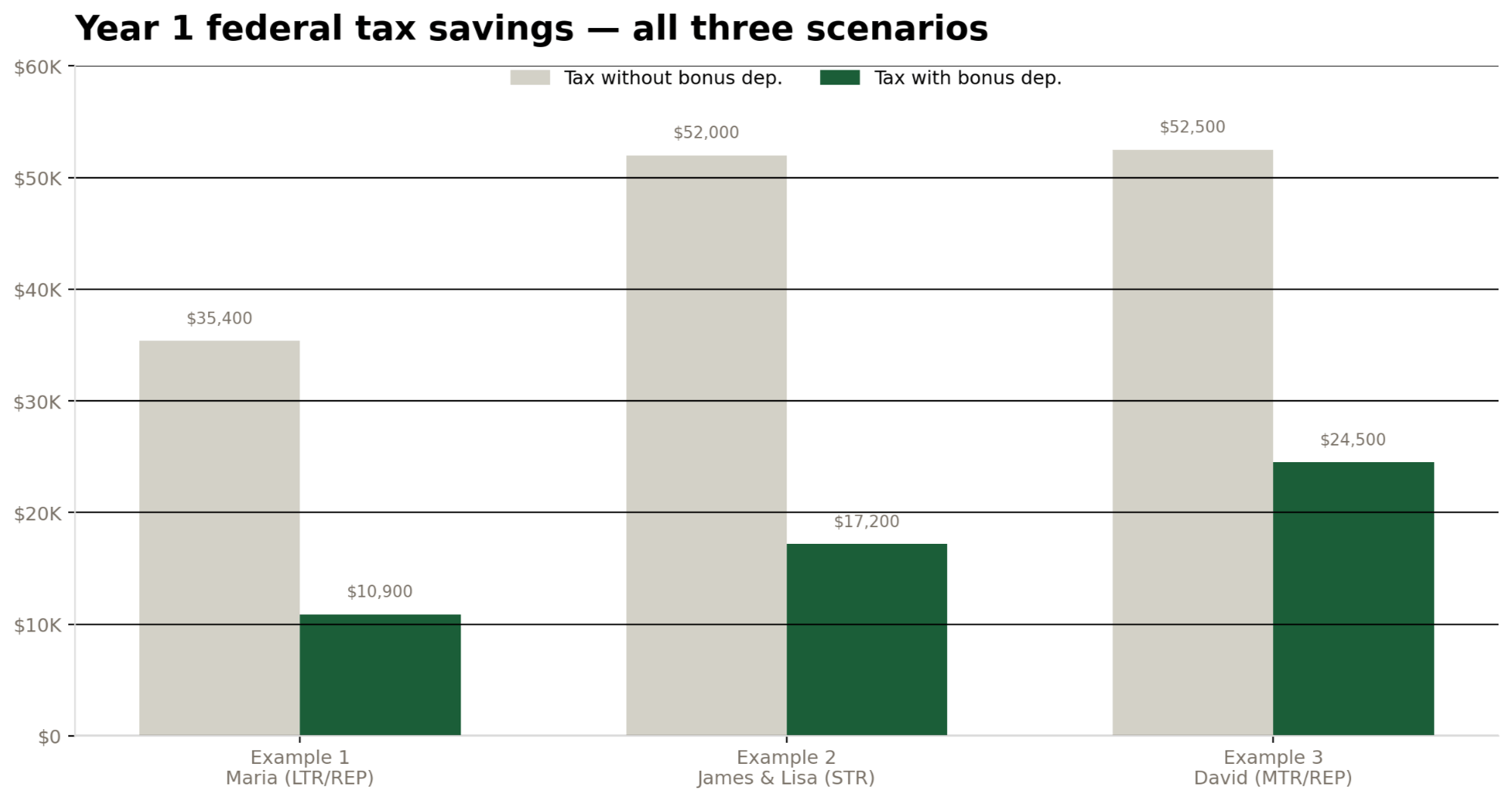

Example 1: The Real Estate Agent — Long-Term Rental

Maria · Licensed AZ Agent · $180K commission income · REP status

| Cost Segregation Results | Value | Method |

|---|---|---|

| 5-yr personal property (appliances, carpet, fixtures) | $72,000 | 100% Bonus |

| 15-yr land improvements (landscaping, driveway) | $18,000 | 100% Bonus |

| 27.5-yr building structure | $310,000 | Straight-line |

| Total bonus-eligible components | $90,000 | Year 1 deduction |

| Year 1 Deductions | Amount |

|---|---|

| Bonus depreciation (5-yr + 15-yr) | $90,000 |

| Standard depreciation ($310K ÷ 27.5) | $11,273 |

| Operating expenses (taxes, insurance, maintenance, interest) | $24,000 |

| Gross rental income | ($26,400) |

| Net rental loss (non-passive for REP) | $98,873 |

Example 2: The W-2 High Earner — Short-Term Rental

James & Lisa · Software Engineer + Part-Time · $250K combined · No REP status

| Cost Segregation Results | Value | Method |

|---|---|---|

| 5-yr personal property | $105,000 | 100% Bonus |

| 7-yr furniture & fixtures | $35,000 | 100% Bonus |

| 15-yr land improvements | $28,000 | 100% Bonus |

| 27.5-yr building structure | $392,000 | Straight-line |

| Total bonus-eligible components | $168,000 | Year 1 deduction |

| Year 1 Deductions | Amount |

|---|---|

| Bonus depreciation (5-yr + 7-yr + 15-yr) | $168,000 |

| Standard depreciation ($392K ÷ 27.5) | $14,255 |

| Operating expenses (platform fees, cleaning, utilities, mortgage interest) | $38,000 |

| Gross STR rental income | ($82,000) |

| Net STR loss (non-passive — avg. stay ≤7 days + material participation) | $138,255 |

Example 3: The Real Estate Agent — Mid-Term Rental

David · Phoenix Top Producer · $240K commissions · REP status · Corporate tenants

Mid-term rentals are passive for non-REPs — usable only against passive income. For real estate agents with REP status, they're a tax weapon with less operational complexity than STRs. Almost no guide explains this distinction.

| Cost Segregation Results | Value | Method |

|---|---|---|

| 5-yr personal property | $62,000 | 100% Bonus |

| 7-yr furniture & equipment | $28,000 | 100% Bonus |

| 15-yr land improvements | $12,000 | 100% Bonus |

| 27.5-yr building structure | $228,000 | Straight-line |

| Total bonus-eligible components | $102,000 | Year 1 deduction |

How to Use Bonus Depreciation in Real Estate (Step-by-Step)

- Acquire an investment property that fits your broader investment and tax strategy.

- Complete a cost segregation study to identify 5-year, 7-year, and 15-year assets eligible for accelerated write-offs.

- Place the property in service so it is actually available for rent and eligible for the deduction.

- Determine whether you qualify as a REP or whether a short-term rental tax strategy is the better path for offsetting active income.

- Work with your CPA to file Form 4562 correctly and coordinate the deduction with your broader tax plan, including Roth conversions, estimated payments, and long-term exit strategy.

The investors who benefit most from bonus depreciation in real estate are not just buying property. They are intentionally structuring the acquisition, the tax classification, and the timing of the deduction from day one.

Real Case Studies: Bonus Depreciation in Action

Understanding bonus depreciation is one thing. Seeing how it actually plays out in real transactions is where the strategy becomes clear. Below are three real-world examples from my own content library showing how different acquisition strategies can dramatically impact both income and tax outcomes.

For a deeper breakdown of these strategies, explore: Scottsdale STR Case Study, $100K Airbnb Case Study, and Casita Strategy Case Study.

Scottsdale 85254 Turn-Key STR | Bonus Depreciation Strategy

Turn-key short-term rental | fully furnished | immediate income

This acquisition was built around execution from day one: a fully operational short-term rental, already producing income, purchased at the right time to align with year-end tax planning.

- ✓

$170,000 below list price

- ✓

Fully furnished and ready for immediate operation

- ✓

Roughly 87% occupancy with a 4.98 rating at the time of the case study

- ✓

Seller covered closing costs and significant improvements

The ability to place the property in service immediately is critical for bonus depreciation. Turn-key STRs eliminate delays like renovations, furnishing, and setup—allowing investors to execute the tax strategy within the same year.

Palm Valley Goodyear STR | $100K+ Airbnb Revenue Strategy

High-performing STR | West Valley opportunity

This property highlights a different angle—identifying strong-performing short-term rental opportunities outside of Scottsdale, where acquisition price is lower but revenue potential remains strong.

Markets like Goodyear offer a unique combination of lower entry price and strong rental demand driven by sports, seasonal travel, and event-based demand. When paired with bonus depreciation, this creates both cash flow and tax efficiency.

Palm Valley Casita Strategy | Hybrid STR + Bonus Depreciation

Primary + income-producing casita setup

This strategy blends lifestyle and investment—using a property with a separate casita to generate rental income while maintaining flexibility for personal use.

- ✓

Separate income-producing unit

- ✓

Flexibility between STR income and personal use

- ✓

Potential for bonus depreciation on the qualifying portion of the property

Hybrid properties open the door to tax strategies while maintaining lifestyle flexibility—something many investors overlook when evaluating real estate purely as an asset.

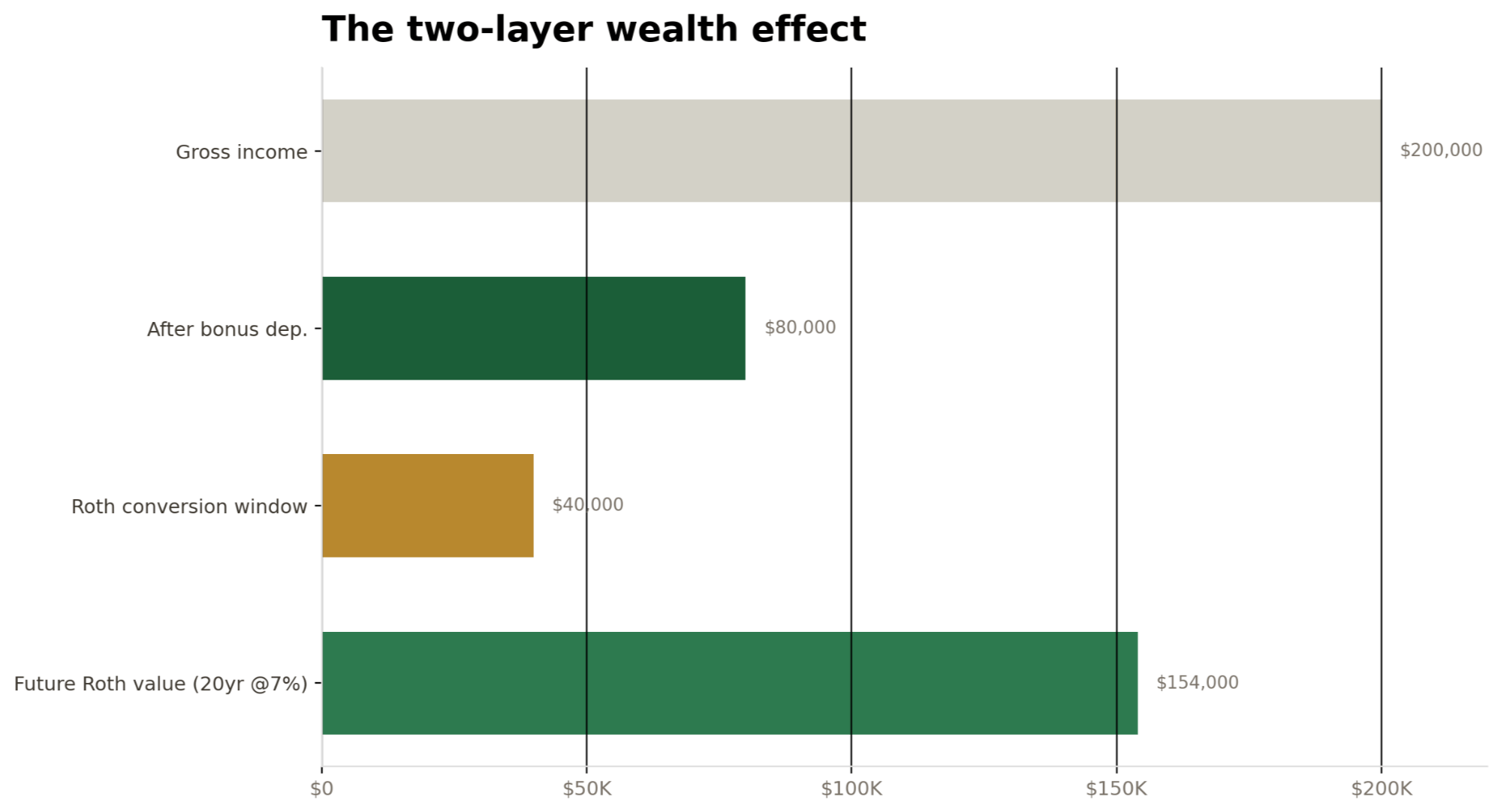

Bonus Depreciation + Roth Conversions: The Advanced Play

This is a strategy I've used with clients who think in 10 and 20-year time horizons.

Bonus depreciation lowers your taxable income dramatically in Year 1. If your income was $200,000 and a cost seg study drops it to $80,000, you've created a low-income window. In that window, you can convert pre-tax retirement funds (Traditional IRA, 401(k), SEP-IRA) to a Roth IRA at a much lower effective rate than you'd normally face.

Converted funds grow tax-free forever, and qualified Roth distributions in retirement are completely tax-free. The combination creates a two-layered wealth effect: reduce taxes now through bonus depreciation, and reduce taxes permanently in retirement through Roth conversion. This is the kind of integrated planning — merging wealth management with real estate strategy — that I bring to every client conversation.

Section 10Arizona Investors: State Conformity and What It Means for You

Arizona has historically decoupled from federal bonus depreciation in certain years. Even when you take a full federal deduction, you may owe Arizona state tax on the income that deduction offsets federally. This doesn't eliminate the strategy — federal savings typically far exceed state tax owed — but you must model both.

Simplified example: $100K bonus depreciation

| Return | Taxable Income After Dep. | Effective Rate | Tax Owed |

|---|---|---|---|

| Federal (with full deduction) | $50,000 | ~22% | ~$11,000 |

| Arizona (if non-conforming) | $150,000 | ~4.5% | ~$6,750 |

| Net federal benefit | ~$20,500+ saved | ||

The strategy still wins — but the Arizona tax bill is real and must be planned for.

- Confirm current-year Arizona conformity status with a CPA — Arizona's conformity can change year to year based on state legislation. Don't assume it matches federal rules.

- Model both federal and state outcomes before electing 100% bonus depreciation. In some cases, 40% federal produces a better combined outcome.

- Consider entity-level implications if your rental is held in an LLC or S-corp — Arizona filing rules may differ.

Verify current-year status at azdor.gov or with a licensed Arizona CPA.

Bonus Depreciation vs. Section 179: Key Differences

| Feature | Bonus Depreciation (IRC §168(k)) | Section 179 (IRC §179) |

|---|---|---|

| Annual dollar cap | None | ~$1.22M (2026, inflation-adjusted) |

| Can create a net operating loss? | ✓ Yes — carries forward indefinitely | ✗ No — limited to business income |

| Phase-out threshold | None | Phases out above ~$3.05M in purchases |

| New vs. used property | Both (new to taxpayer) | Both |

| State conformity issues | Common (CA, AZ, others) | Generally more conformity |

| Best for | Large deductions, NOL creation, real estate investors | Smaller businesses managing income levels |

| Can they be combined? | Yes — use §179 first up to income limit, then apply bonus depreciation to the remainder | |

Common Mistakes and How to Avoid Them

Frequently Asked Questions

Real Estate vs. Stocks: Why Bonus Depreciation Changes the Equation

Traditional equities can offer growth and liquidity, but they do not give investors the same combination of cash flow, leverage, depreciation, and tax control that real estate can provide. That is one reason I often frame property decisions as capital allocation decisions rather than just transactions.

When bonus depreciation in real estate is paired with the right asset, the equation changes meaningfully. Instead of simply hoping for appreciation, investors may generate income, capture principal paydown, participate in upside, and create an immediate tax benefit in Year 1. That combination is difficult to replicate elsewhere.

Stocks can appreciate. Real estate can appreciate and potentially reduce taxable income at the same time. When structured correctly, bonus depreciation gives investors a powerful reason to think about after-tax returns rather than headline returns alone.

Is This Strategy Right for You?

Bonus depreciation in real estate is not just a tax strategy — it is a capital allocation decision. In 2026, with 100% bonus depreciation permanently restored, investors who understand cost segregation, REP status, short-term rental rules, and long-term planning have an opportunity to reduce taxable income while accelerating wealth building. The question is no longer whether the strategy exists. The question is whether you are positioned to use it correctly.

Who this strategy is best for

- ✓

Real estate agents, brokers, and full-time real estate professionals earning strong active income

- ✓

High-income W-2 earners exploring short-term rentals and willing to materially participate

- ✓

Investors acquiring property after January 19, 2025 and open to using a cost segregation study

- →

Anyone looking to reduce taxable income through real estate while still focusing on asset quality and long-term wealth building

- ✓ Real estate agent, broker, or full-time investor earning $100K+

- ✓ W-2 earner in 24%+ bracket open to an STR with active management

- ✓ Acquired (or acquiring) property after January 19, 2025

- ✓ Willing to commission a cost segregation study

- ✓ Thinking in multi-year wealth terms, not one-time deductions

- → Unsure whether you qualify as a REP

- → Significant passive losses already carried forward

- → Taxed in Arizona or other non-conforming states

- → Rental income close to or exceeds your deductions

Helpful Resources

| Resource | Why it helps |

|---|---|

| IRS Newsroom: Notice 2026-11 overview | Best official summary of the 2026 guidance and OBBBA changes. |

| IRS Publication 946 | Core IRS resource on depreciation, MACRS, and the special depreciation allowance. |

| IRS Publication 925 | Important for passive activity rules, including the 7-day exception tied to STR strategy. |

| Arizona Department of Revenue: IRC conformity | Helpful for Arizona investors evaluating how state conformity affects bonus depreciation planning. |

| IRS Topic No. 415 | Useful IRS summary on renting residential and vacation property. |

Bonus depreciation in real estate is not just a tax strategy—it is a long-term wealth strategy. When applied correctly, it can significantly accelerate how quickly you build and retain wealth through real estate.

The information in this guide is for educational purposes only and does not constitute legal, tax, or financial advice. Tax laws are complex, change frequently, and vary by individual circumstance. Always consult a qualified CPA or tax advisor before implementing any strategy. The examples in this article use approximate tax rates for illustration purposes — actual savings will vary based on your full financial picture, filing status, state of residence, and other factors.

Categories

- All Blogs (303)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (19)

- Buyers (196)

- Financial Planning (54)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (23)

- New Construction (26)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (84)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.