Why California Investors Are Moving Millions Into Phoenix Through 1031 Exchanges

1031 Exchange · California → Arizona · 2026

Why California Investors Are Moving Millions Into Phoenix Through 1031 Exchanges

Coastal cap rates compressed, the rules tightened, and the math stopped working. Here is why so much California real-estate capital is exchanging into Phoenix instead of reinvesting at home — and the one California rule almost every article gets wrong.

Walk into any qualified intermediary's office in Los Angeles, San Diego, or the Bay Area right now and ask where the exchange money is going. A growing share of the answer is the same: Phoenix. California investors who spent decades building equity in rent-controlled, low-cap-rate coastal buildings are selling, deferring their gains under Section 1031, and redeploying that equity into Maricopa County — where the same dollars buy more units, more cash flow, and a far lighter regulatory load.

This isn't a fad. It's a rational response to a widening gap between what California real estate yields and what California now costs to own. This guide walks through the entire move: why reinvesting in California stopped pencilling, why Phoenix specifically, exactly how a 1031 exchange works, and the California "clawback" that most blog posts either ignore or get flat-out wrong. Read it before you call your CPA — then call your CPA.

Last updated July 2026. Market figures, cap rates, tax rates, and financing terms in this guide are current as of this date and can change — always verify the specifics with your CPA, qualified intermediary, and attorney before acting.

01The capital migration in plain numbers

The headline driver behind the move is one of the oldest forces in real estate: the spread between yield and cost. In primary coastal California markets, multifamily assets routinely trade at going-in cap rates in the 4% to 5% range — Los Angeles, San Francisco, and the other gateways remain among the most compressed in the country. Buyers there are paying a premium for stability and long-run appreciation, accepting thin current income in exchange.

Phoenix sits a meaningful step higher on the yield curve. Strong-growth Sun Belt metros like Phoenix have generally held multifamily cap rates around 5% to 5.5%, and value-add or older product can run higher still. On a multi-million-dollar exchange, 75 to 150 basis points of additional going-in yield is not a rounding error — it's tens of thousands of dollars of annual cash flow on the same equity, before you account for everything else that's different between the two states.

Going-in cap rate, illustrative ranges (2026)

Ranges vary widely by asset class, vintage, and submarket. Class C and value-add product trades wider; trophy Class A trades tighter. Verify against current broker comps before underwriting.

Layer on the tax and regulatory differences — covered in detail below — and you understand why a California owner sitting on a fully appreciated, rent-capped building increasingly concludes that the smartest move is to harvest that equity through a 1031 exchange rather than trade it for another low-yielding California asset.

02Why reinvesting in California stopped working

The instinctive move for a California investor selling a California property is to roll into another California property. For a long time that made sense. Three structural pressures have steadily eroded that logic.

1. Rent caps put a ceiling on your upside

Since 2020, California's Tenant Protection Act (AB 1482) has capped annual rent increases statewide at 5% plus regional CPI, never to exceed 10%, on most multifamily built before the prior 15 years. In the Los Angeles region, that ceiling resets to 8.7% effective August 1, 2026 — and in cities with their own rent-control ordinances (Los Angeles RSO, San Francisco, Oakland, Berkeley, Santa Monica), the local cap is often far lower, sometimes under 2%. Vacancy decontrol survives, so you can reset to market on turnover, but "just cause" eviction rules and relocation payments make turning a unit slow and expensive. For an investor, a legal ceiling on rent growth is a legal ceiling on net-operating-income growth — and therefore on value creation.

2. The tax burden compounds every year you hold

California's top marginal income tax rate is 13.3% — the highest in the nation — and rental income is taxed as ordinary income at the state level. Every dollar of net cash flow from a California building is taxed more heavily than the same dollar earned in a low- or no-tax state. Over a long hold, that drag is enormous.

3. The friction of operating keeps rising

Layered tenant protections, slow eviction timelines, escalating compliance obligations, and active local rent-control politics (new ballot initiatives surface regularly) all raise the cost and risk of being a California landlord. None of these are reasons to panic-sell. They are reasons that, when an owner is already at a natural decision point — a sale, an estate event, a portfolio rebalance — the replacement-property search increasingly looks beyond the state line.

03Why Phoenix — and the honest case against it

Plenty of states are cheaper and lower-tax than California. What makes Phoenix the magnet for California exchange capital specifically is the combination of scale, growth, and proximity. It's a major metro within a short flight or a one-day drive, with demographic and employment tailwinds that few markets can match.

The structural tailwinds

- In-migration. Metro Phoenix added roughly 80,000 new residents in 2024, ranking among the top large metros for net domestic in-migration. A large share arrive from higher-cost California and coastal markets.

- Employment diversification. The TSMC semiconductor build-out in north Phoenix, the expansion of Mayo Clinic and Banner Health, and growing financial-services back-office operations have broadened the economy well beyond its old construction-and-tourism base.

- A landlord-friendly framework. Arizona has banned municipal rent control, allows market-rate rents, and has one of the fastest eviction processes in the country for nonpayment. Investors price that flexibility into value.

- Lower carrying costs. Arizona's flat 2.5% state income tax and an effective property tax burden around 0.5% sit far below California's, and Proposition 117 caps annual growth in a property's taxable (limited) value at 5%.

The part most "Phoenix is booming" articles leave out

Here's the honesty that separates real underwriting from cheerleading: Phoenix is soft right now. (We track the numbers monthly in our Phoenix housing market updates.) After absorbing one of the largest apartment-supply waves in decades, the metro entered 2026 with elevated vacancy (roughly 11%–12% in some multifamily surveys), asking rents down on the order of 3%–4% year over year, and concessions widespread. Average per-unit pricing has fallen meaningfully from the 2022 peak — by double digits in some data sets.

For a disciplined buyer, that softness is the opportunity, not the warning sign. Per-unit pricing below the 2022 peak — and, in many cases, below today's replacement cost (construction costs are up nearly 40% since 2020) — means you can acquire stabilized assets for less than it would cost to build them. Meanwhile the new-supply pipeline has contracted sharply (units under construction down roughly 30% year over year), and absorption has been strengthening. That is the textbook setup for a supply correction: pain now, firmer occupancy and rent growth as deliveries fade. National research houses broadly expect Sun Belt markets like Phoenix to move back toward equilibrium and outperform over the longer term, even as they caution that 2026 will stay choppy.

California vs. Arizona, side by side

| Factor | California | Arizona |

|---|---|---|

| Top state income tax | Up to 13.3% | 2.5% flat |

| Effective property tax | ~0.71% (Prop 13 caps growth at 2%/yr) | ~0.5% (Prop 117 caps growth at 5%/yr) |

| Rent control | AB 1482 caps increases at 5% + CPI (max 10%); stricter local ordinances | No rent cap; municipal rent control preempted by A.R.S. § 33-1329 |

| Eviction for nonpayment | Slow; "just cause" + relocation rules | Among the fastest in the U.S. |

| Typical multifamily cap rate | ~4.0–5.0% (gateway) | ~5.0–5.5%+ |

| Property insurance | Carrier exits & FAIR Plan; rising cost, limited availability (wildfire) | Below national average; ~100+ competing carriers; low catastrophe risk |

| Sale withholding | 3.33% of price (exempt via Form 593 in a 1031) | No state withholding equivalent |

04The demand engine: companies are betting hundreds of billions on Phoenix

The single best reason to underwrite Phoenix through a soft patch is the demand side of the equation. The Valley isn't growing on sunshine and retirees — it's in the middle of one of the largest concentrations of corporate capital investment anywhere in the country, and every one of those jobs is a future renter or buyer. This is the engine that turns near-term softness into long-term rent growth, and it's why seasoned investors treat 2026 as an entry window rather than a red flag.

Semiconductors: the $165 billion anchor

TSMC is building the largest foreign direct investment in a greenfield project in U.S. history. Its commitment to north Phoenix has grown from $12 billion in 2020 to roughly $165 billion, and the build-out is planned to include up to six chip-fabrication plants, two advanced-packaging facilities, and an R&D center — a "gigafab" cluster. The first fab is already online producing 4-nanometer chips (Apple, its largest customer, is reported to be sourcing more than 100 million Arizona-made chips in 2026, with NVIDIA among other clients); the second fab's structure is complete with 3nm production targeted for late 2027; and a third fab for 2nm-class chips broke ground in 2025. TSMC has said the project supports roughly 40,000 construction jobs over four years plus tens of thousands of permanent high-wage positions, and is expected to drive more than $200 billion in indirect economic output over the decade.

Intel adds a second pillar: the company has invested on the order of $20 billion-plus expanding its Ocotillo campus in Chandler, where it already employs more than 12,000 people across operating fabs. Two of the world's most important chipmakers competing for the same talent in the same metro is, for a housing investor, an almost ideal backdrop.

The part that compounds is the ecosystem. Where fabs go, the supply chain follows. Advanced-packaging and materials specialists — Amkor in Peoria, NXP and Microchip Technology in Chandler, ON Semiconductor, plus a steady stream of suppliers such as KoMiCo, Fujifilm Electronic Materials, TOCALO, and Pure Wafer — have expanded or planted operations across the East Valley's Price Corridor, now one of the densest semiconductor clusters in the Western Hemisphere. The Greater Phoenix Economic Council counts more than 140,000 semiconductor-relevant jobs in the metro and 75-plus semiconductor companies, with Arizona State University's large engineering pipeline feeding the workforce.

Healthcare, aerospace, and a diversifying base

Phoenix's growth story is far broader than chips. Mayo Clinic is undertaking a $1.9 billion expansion of its north Phoenix campus, adding roughly 1.2 million square feet and thousands of jobs, while Banner Health anchors one of the metro's largest and most recession-resilient employment sectors. A long-established aerospace and defense base adds further ballast. Newer entrants are broadening the mix: Axon Enterprise (the Scottsdale-based maker of public-safety technology) is in a major headquarters expansion adding thousands of roles, advanced-manufacturing startup Hadrian is investing around $200 million in an AI-driven facility in Mesa, and clean-energy and battery investment continues to land across the region. Companies including GoDaddy and Microchip are headquartered here, and others — Dutch Bros among them — have shifted corporate operations into the Valley. Venture-capital investment in the metro topped $3.6 billion in a single recent year.

Data centers and logistics

Phoenix has quietly become one of the nation's largest data-center markets, with hyperscalers expanding capacity as AI demand pours capital into power, land, and construction. On the logistics side, the metro absorbed close to 10 million square feet of industrial space in a single recent quarter — among the most in the western U.S. — much of it tied to semiconductor supply chains and to companies relocating operations out of California and the Midwest. New international air service, including nonstop flights to Asia, underscores how the Valley's connectivity is scaling alongside its industrial base.

Why this matters to a 1031 buyer

Jobs are the demand side of your rent roll. High-wage semiconductor, healthcare, and technology employment pulls in precisely the renter profile that fills well-located apartments and single-family rentals — and a meaningful share of those workers are relocating from California's Silicon Valley, where the state-income-tax gap alone (Arizona's 2.5% flat rate versus up to 13.3% in California) often exceeds their entire moving cost. That is the structural demand that underwrites the long-term thesis. The current supply wave is finite and already correcting; the employment build-out runs for the rest of the decade. When you buy into the soft patch, you're buying ahead of the jobs that are still being created. See how we approach Arizona investment property for out-of-state buyers.

05The new-construction edge: financing, rents & insurance

A large share of the California exchange capital landing in Phoenix isn't chasing tired 1980s garden apartments — it's buying brand-new construction. For an out-of-state 1031 buyer trading out of a fully appreciated, low-yield California asset, new product stacks three advantages that older buildings can't match: builder-subsidized financing, a rent premium renters happily pay, and dramatically lower, more available insurance than California.

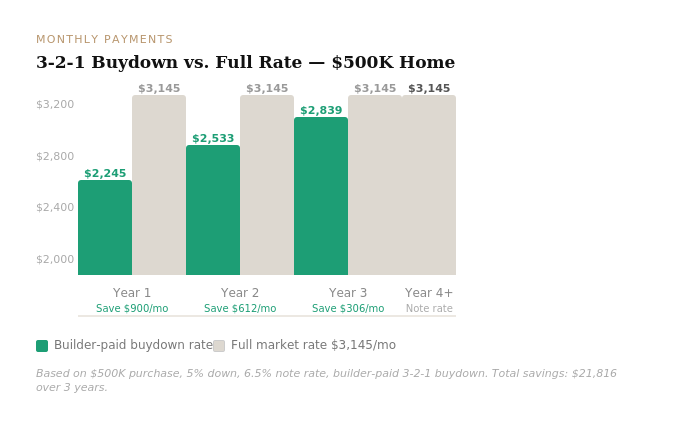

Builder financing can beat the open market by more than a point

While Phoenix clears its supply overhang, builders have leaned hard on incentive financing — and that's the buyer's gain. Through permanent rate buydowns and bulk forward commitments, a builder's preferred lender pre-purchases a block of money at a below-market rate and originates loans on select homes from it. In this market, that has put qualified buyers into 30-year fixed financing in the high-3s to low-4s — rates as low as roughly 3.75% on certain new-construction inventory — at a time when the open market sits meaningfully higher. Documented Phoenix builder programs have advertised buydown rates near 3.99% (and lower before that), so the high-3s are not a gimmick; they're a structural feature of today's new-build market.

Why builders do it: a buydown lets them protect the headline price while advertising a lower monthly payment — and, in a detail most buyers miss, forward-commitment buydown costs fall outside the normal seller-concession caps, so a builder can subsidize far more than an ordinary seller could (national builders routinely spend well into the single and double digits as a percentage of price on these packages). Lock a sub-4% cost of capital onto a new, low-maintenance asset and your cash-on-cash math is transformed — exactly the lever a 1031 buyer wants when redeploying coastal equity.

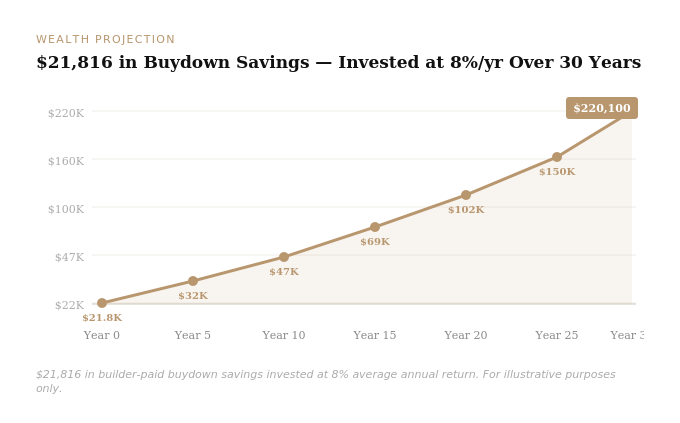

The payment relief is the visible part. What investors tend to miss is what that saved capital becomes once it's redeployed rather than spent — a buydown isn't a discount you consume, it's cash flow you can compound.

Renters pay a premium for brand-new — and stay longer

New construction commands a rent premium and leases up faster — and the size of that premium depends on which rental strategy you run (long-term, mid-term, or short-term). Tenants pay more for current finishes, in-unit laundry, energy-efficient systems, smart-home features, and the simple confidence that everything is under warranty. That matters twice over for an investor: the higher rent lifts gross income, and the near-zero deferred maintenance and capex in the early years means more of every rent dollar survives all the way down to net operating income. New product also pairs well with a bonus depreciation and cost-segregation strategy, and tends to attract higher-credit, longer-tenured renters — and with lease renewals running at historically high levels nationally, retention on a desirable new asset quietly cuts turnover cost and vacancy risk. For a remote, out-of-state owner, "new and low-maintenance" isn't a luxury; it's an operating strategy.

Arizona insurance is a fraction of California's volatility

This is the line item most pro formas underweight. California's property-insurance market is in genuine distress: major carriers have pulled back or stopped writing new policies over wildfire exposure, owners are increasingly pushed onto the state's FAIR Plan of last resort at higher cost and thinner coverage, and non-renewals have become routine. The risk isn't only price — it's whether you can get covered at all.

Arizona is the mirror image. No hurricanes, no coastal flooding, and minimal seismic risk mean lower catastrophe exposure, and roughly 100-plus admitted carriers compete for Arizona business — which keeps premiums below the national average and, just as importantly, keeps coverage available and predictable. New construction compounds the edge: a brand-new roof, wiring, and plumbing insure cheaper than aging California building stock. Lower, stable insurance flows straight into NOI — and therefore straight into your cap rate and your value.

…and the rules still favor the owner

Now stack those three advantages on top of what we already covered — no municipal rent control in Arizona, market-rate rents with no statewide cap, and one of the fastest eviction processes in the country. Cheaper capital, a rent premium, lower insurance, and a landlord-friendly legal framework don't just add up — they compound. The operating economics of a new Phoenix rental simply outrun a rent-capped, high-friction California building holding the same equity.

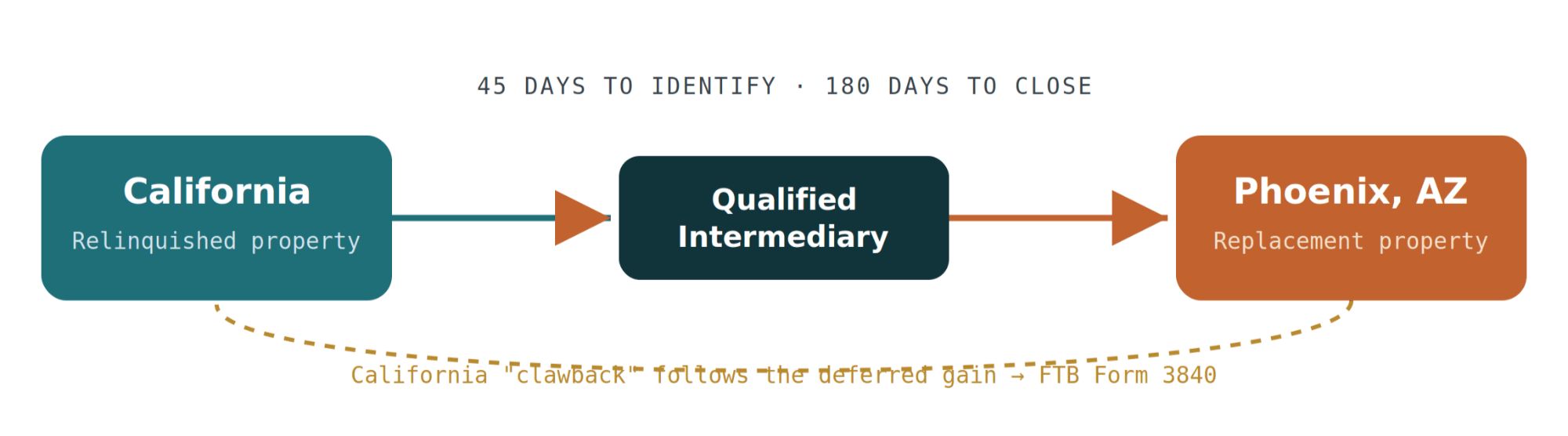

06How a 1031 exchange actually works

A 1031 exchange — named for Section 1031 of the Internal Revenue Code — lets you sell investment real estate and defer the federal capital-gains tax and depreciation recapture you'd otherwise owe, provided you reinvest the proceeds into like-kind replacement property and follow the rules precisely. "Like-kind" for real estate is broad: virtually any U.S. investment or business real property qualifies as like-kind to any other. You can swap an apartment building for retail, raw land for a warehouse, or one property for several.

Good news on the legislative front: the One Big Beautiful Bill Act (OBBBA) left Section 1031 intact, without the previously floated cap on deferral. As of 2026 the strategy stands on solid ground, though proposals to limit it resurface in Congress periodically, so stay informed.

The rules you cannot break

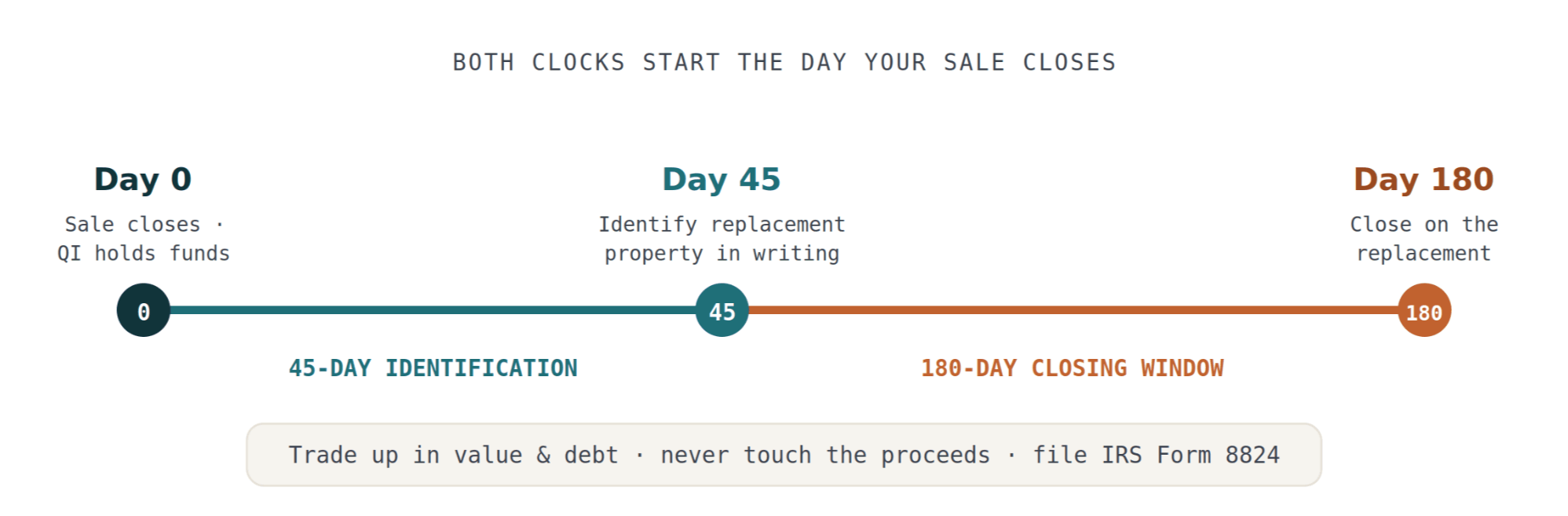

- Two deadlines, both firm. From the day your sale closes, you have 45 calendar days to identify replacement property in writing and 180 calendar days to close on it. Both clocks start at the same closing and run concurrently. There are no extensions for weekends or holidays, and missing either deadline by a single day voids the exchange.

- Use a Qualified Intermediary (QI). You may never take possession of the sale proceeds. A neutral QI must hold the funds between transactions. Touch the money — even briefly — and the IRS treats it as a taxable sale.

- Trade up in value and debt. To defer 100% of the gain, your replacement property must be of equal or greater value, and you must carry equal or greater debt (or replace any debt paydown with fresh cash). Any shortfall — cash received or debt reduction — is "boot," and boot is taxable.

- Same taxpayer rule. The entity that sold the relinquished property must be the entity that buys the replacement. Names must match.

- Report it. File IRS Form 8824 with the tax return for the year of the exchange.

One more planning note for year-end sellers: if you sell late in the year, your 180-day window can be cut short by your tax-filing deadline. To preserve the full 180 days, you generally must file an extension on your return. Coordinate this with your CPA the moment you go under contract.

07The California catch: the clawback & Form 3840

This is the section most articles skip — and the one that matters most when you exchange out of California. This is where real estate tax strategy earns its keep. There's a persistent myth in investor circles that goes: "If I 1031 my California building into Arizona, I'm done with California taxes forever." That is wrong, and believing it can cost you six figures.

California is a "sticky" tax state. Under Revenue & Taxation Code Sections 18032 and 24953, the Franchise Tax Board (FTB) takes the position that gain which accrued while a property sat on California soil remains California-source income — even after you exchange into an out-of-state property, and even if you later move to Nevada, Texas, or Arizona yourself. You haven't escaped the California tax. You've deferred it, federally and at the state level, and California intends to collect when the chain finally ends.

How the FTB keeps score: Form 3840

To track that deferred California gain, the FTB requires you to file an annual information return — FTB Form 3840, California Like-Kind Exchanges — for the year of the exchange and every subsequent year until the deferred California-source gain is finally recognized. This is not a one-time filing. Skip it, and the FTB can issue a Notice of Proposed Assessment, estimate your income, and bill you for the entire deferred gain plus penalties and interest — leaving you with the burden of proving you didn't actually cash out.

The enforcement teeth are real. The FTB has invested heavily in data-matching systems that cross-reference your federal Form 8824 filings against your California return. If the federal data shows a California 1031 exchange but no Form 3840 appears on the state side, the mismatch can trigger an automatic notice. Treat annual 3840 compliance as non-negotiable.

The legitimate way to make the clawback disappear

There is a clean, legal endgame: "swap till you drop." If you keep exchanging — never selling for cash — and hold the final replacement property until death, your heirs receive a stepped-up basis to current market value. That step-up eliminates the deferred gain entirely, wiping out both the federal and the California liability. It's the reason 1031 exchanges are as much an estate-planning instrument as a tax-deferral one. Confirm the current rules with your estate-planning attorney, since tax law evolves.

08A worked example: LA fourplex → Phoenix

Numbers make it concrete. This is illustrative only — your real figures depend on basis, debt, depreciation, and current pricing — but it shows the shape of the decision. To model your own, use our real estate calculators or walk through more 2026 tax-strategy scenarios.

Suppose you own a Los Angeles fourplex bought years ago, now worth $1,500,000, with a large embedded gain and an AB 1482 rent cap keeping your in-place rents well below where the market would otherwise be. Sold outright, you'd face federal capital-gains tax, depreciation recapture, and California tax at rates up to 13.3% — a combined bill that could easily exceed $300,000, vaporizing a fifth of your equity in a single transaction.

Instead, you 1031 the full proceeds into Phoenix. At a roughly 5.3% going-in cap rate versus the ~4.3% your LA building yields, the same equity produces materially more annual NOI — and you redeploy into a market with no rent-control ceiling, a 2.5% flat income tax on the cash flow, and lower property taxes. You defer the entire tax bill, keep your full equity working, and file FTB Form 3840 each year to stay compliant on the deferred California gain. If you ultimately hold to a step-up at death, that deferred California tax is never paid at all.

09Real California-to-Arizona exchanges we've closed

The framework above isn't theoretical. These are real California-to-Arizona exchanges we've guided — verifiable case studies with the numbers as closed.

1031 Exchange · California → Arizona

$139,272 deferred — structured to be eliminated for the heirs

Glendale, AZ · single-family rental

A Southern California investor had held a rental for 17 years on a large embedded gain. We engaged the qualified intermediary before the property was listed, sold, and exchanged into a Glendale single-family rental secured roughly $20,000 under list with a cash offer — proceeds held in a segregated, FDIC-insured account, with the 45- and 180-day deadlines met. Then, coordinating with the client's CPA and estate attorney, we built the hold around the stepped-up basis at death (IRC § 1014), so the gain California tracked for 17 years is set to be eliminated entirely for the next generation.

Read the full case study →

1031 Exchange · California → Arizona

$2M California asset repositioned into two Arizona rentals

Peoria, AZ · Vistancia

This client exchanged a $2M California multifamily asset into two single-family rentals in Vistancia. The California property produced solid rent, but high taxes, insurance, and tenant-friendly laws capped its efficiency. The Arizona strategy delivered stronger cash flow and lower operating costs — roughly $1,000 a month more in net cash flow and about $15,000 a year in property-tax savings. Same capital, smarter deployment.

Read the full case study →

1031 Exchange · TSMC growth corridor

$110K below list in the path of Phoenix's biggest employer

North Phoenix · Union Park at Norterra

An investor redeploying capital into a high-growth rental market near the TSMC expansion corridor secured a Union Park at Norterra property $110,000 below list, with projected rents of $3,100–$3,500 a month inside a master-planned, amenity-rich community 15 minutes from the fabs. Owning exactly where the jobs are landing.

Read the full case study →And it's not only the buy side — we handle the exit too. One North Scottsdale seller achieved a neighborhood-record price with 20-plus offers, then rolled the proceeds into a 1031 exchange replacement in Tucson.

Past results don't guarantee future outcomes. Every exchange depends on your specific basis, debt, timeline, and goals — these examples illustrate strategy, not a promised result.

10The step-by-step playbook

- Build the team before you list. You'll want a Qualified Intermediary, a CPA fluent in California exchange rules (especially Form 3840), and a Phoenix-side broker who underwrites investment product, not just resale homes. This is not the place for generalists.

- Engage the QI before closing. The QI must be in place before your sale closes. Set this up while you're in escrow, not after.

- Handle the Form 593 withholding exemption at the California closing. Certify the 1031 exemption so you're not over-withheld.

- Identify within 45 days. Submit your written identification to the QI — most use the three-property rule (identify up to three regardless of value) or the 200% rule. Identify with days to spare, never on day 45.

- Underwrite Phoenix conservatively. Verify trailing rents and comps, build in realistic concessions and vacancy, confirm the supply pipeline in your target submarket, and walk the units for deferred maintenance.

- Close within 180 days — and watch the year-end trap. If your sale was late in the calendar year, file a tax extension to preserve the full window.

- File Form 8824 federally and FTB 3840 with California — then 3840 every year after. Calendar the annual 3840 obligation so it never lapses.

11Risks and honest caveats

A guide that only sells the upside isn't worth trusting. The real risks here:

- Near-term softness is real. Phoenix rents and pricing are under pressure in 2026. If you over-leverage or assume aggressive rent growth, the trough can hurt before the recovery helps.

- The clawback is a tail, not an escape. Exchanging out of California defers — it doesn't erase — the California gain unless you hold to a step-up. Plan for the long-term obligation and the annual filing.

- Climate and water diligence matter. Extreme summer heat and long-run water security have moved from background concerns to active underwriting questions for long-hold Phoenix investors. Weight them explicitly.

- The deadlines are unforgiving. A failed identification or a blown 180-day close turns the whole thing into a fully taxable sale. Build in margin.

- Legislative risk. Section 1031 has survived recent proposals intact, but it remains a periodic target. Don't assume the rules are permanent.

Thinking about exchanging out of California?

Run your specific numbers — basis, debt, target cap rate, and the clawback math — before you list. A short consultation can save a six-figure mistake.

Talk through your exchangeOr start browsing Arizona investment listings.

12Frequently asked questions

Can I do a 1031 exchange from California to Arizona?

Yes. Section 1031 is federal and works across state lines. You sell your California investment property and reinvest into a like-kind Arizona property within the 45-day identification and 180-day closing windows to defer your federal gain. California, however, applies its clawback to the original California-source gain, tracked annually on FTB Form 3840 until that gain is recognized.

What is the California clawback and FTB Form 3840?

Under California Revenue & Taxation Code Sections 18032 and 24953, California keeps the right to tax gain that accrued while your property was in California — even after you exchange into an out-of-state replacement and even if you move away. To preserve that right, the FTB requires you to file information return Form 3840 in the year of the exchange and every year afterward until the deferred California gain is recognized.

What are the deadlines for a 1031 exchange?

From your sale's closing date: 45 calendar days to identify replacement property in writing, and 180 calendar days to close on it. Both run concurrently from the same date, with no extensions for weekends or holidays. Sell late in the year and the 180-day window can be shortened by your tax-filing deadline unless you file an extension.

Why buy in Phoenix instead of reinvesting in California?

Phoenix generally offers higher going-in cap rates than coastal California, a 2.5% flat income tax versus California's 13.3% top rate, lower effective property taxes, no municipal rent control, and faster evictions. With strong in-migration and major employers like TSMC and Mayo Clinic, the same equity tends to generate more cash flow and a clearer path to rent growth.

Is 2026 a good time to buy multifamily in Phoenix?

Phoenix is working through a supply correction, so 2026 rents are soft and per-unit pricing has fallen below the 2022 peak — often below replacement cost. For patient, conservatively financed buyers, that softness is the entry opportunity, because the construction pipeline has contracted sharply while long-term demand drivers remain intact. Disciplined submarket selection and conservative underwriting are essential.

Can investors really get a ~3.75% rate on Phoenix new construction?

On select new-construction inventory, yes — but it's builder-funded, not a market mortgage rate. Builders use permanent rate buydowns and bulk forward commitments through their preferred lender to originate loans at below-market rates, which has put qualified buyers into the high-3s to low-4s while the open market sits higher. These programs are time-limited and vary by loan program and occupancy type, so always compare the permanent note rate and total cost with your own broker and confirm investor eligibility before relying on the headline figure.

Is property insurance really cheaper in Arizona than California?

Generally yes, and the bigger story is availability. California's market has seen major carriers retreat over wildfire risk, pushing many owners onto the state FAIR Plan at higher cost with thinner coverage. Arizona avoids hurricanes, coastal flooding, and significant seismic risk and has roughly 100-plus admitted carriers competing, which keeps premiums below the national average and coverage predictable. Brand-new construction insures cheaper still thanks to new roofs and systems.

What major companies are investing in or moving to Phoenix?

Greater Phoenix is anchored by an enormous semiconductor build-out: TSMC has committed roughly $165 billion to a multi-fab campus in north Phoenix — the largest greenfield foreign investment in U.S. history — and Intel has invested $20 billion-plus expanding its Chandler operations, with a deep supplier ecosystem (Amkor, NXP, Microchip, ON Semiconductor and others) clustered in the East Valley. Beyond chips, Mayo Clinic is investing $1.9 billion in a north Phoenix expansion, Axon is expanding its Scottsdale headquarters, hyperscale data centers and AI-driven manufacturing continue to land, and the metro counts 140,000-plus semiconductor-relevant jobs. That high-wage job growth is the demand engine behind long-term rental demand.

Does Arizona have rent control like California?

No. Arizona has no statewide rent cap, and Arizona Revised Statutes § 33-1329 preempts cities and towns from creating their own rent control, with a narrow exception only for government-owned or subsidized housing. That means landlords set rents at market and there is no percentage cap on increases (proper notice and anti-retaliation rules still apply). California, by contrast, caps most rent increases under AB 1482 at 5% plus CPI, up to 10%, with stricter local ordinances in many cities.

Do I still owe California tax if I move to Arizona too?

For the deferred gain that originated from your California property, generally yes — California's clawback applies regardless of where you later live, and continues until the gain is recognized or eliminated through a step-up in basis at death. Your future Arizona-source income is a separate matter. This is a question for a cross-state tax professional.

About Eric Ravenscroft

As Featured In

Published June 24, 2026 · Last reviewed July 15, 2026 · Written and reviewed by Eric Ravenscroft (CRS · GRI · ABR · Top 100 Phoenix Metro · Top 1% Nationwide).

Disclaimer: This article is for general educational purposes only and is not tax, legal, accounting, or investment advice. The author is not your CPA, attorney, or financial advisor, and no advisory relationship is created by reading this page. Section 1031, the California clawback, FTB filing requirements, cap rates, tax rates, and market conditions change and vary by situation; figures cited are general 2026 reference points and illustrative examples, not guarantees. Before executing any exchange, consult a qualified intermediary, a licensed CPA familiar with California requirements, and a real estate attorney about your specific facts.

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.