New Construction Investor Rates Are Closing the Gap in 2026: Builder Buydowns, Cash Flow & the 1031 Exchange Playbook

New Construction Investor Rates

Are Closing the Gap in 2026

Builder buydowns are quietly erasing the rate penalty investors usually pay — and the result is a new, low-maintenance home that renters pay a premium for. Here's the complete playbook on rates, capex, HOA rules, and 1031 exchange timing.

I write this as both a licensed agent who works new construction deals across the Greater Phoenix Metro every week and as an investor who owns rental property myself. What follows reflects rates and incentive structures I'm seeing on active deals right now, not secondhand market commentary.

In this guide

- Why this is happening right now

- The investor rate spread, explained

- What I'm seeing on deals right now

- The catch: HOA rental restrictions

- Where new construction shines

- Why low capex is more than a talking point

- The 1031 exchange playbook

- Decision framework by strategy

- Due diligence checklist

- What clients say

- Frequently asked questions

Section 01Why This Is Happening Right Now

For most of 2022 through 2025, new construction was a tough sell for investors. Builders had pricing power, rates were climbing, and the math on a rental property rarely worked when you were paying retail for a brand-new home with no equity cushion.

That has shifted. Builder confidence softened in early 2026, and the majority of builders have been offering incentives for nearly a year straight as affordability pressure and buyer hesitation have weighed on demand. The largest national builders are leaning hardest into this: roughly two-thirds of new homes sold by major builders are now using a permanent rate buydown, compared to a much smaller share among local and mid-sized builders, with the average buydown shaving over a percentage point off the borrower's rate.

This matters specifically for investors because of where investment property financing currently sits. As of mid-2026, investment property loan rates are generally running about half a point to a full point above owner-occupant rates — a gap that has always reflected the added risk lenders price into a non-owner-occupied loan. What's new is that builders are increasingly willing to fund a meaningful chunk of that gap away rather than cut their headline price. A price cut devalues every comparable home in the neighborhood and can spook buyers already under contract; a rate buydown accomplishes the same affordability goal without that side effect, which is why it has become builders' preferred tool.

Why builders are choosing buydowns over price cuts

Public statements from major builders back this up. D.R. Horton's CEO told investors earlier this year that affordability constraints and cautious buyer sentiment are pushing the company toward heavier use of rate buydowns and closing cost contributions, alongside price cuts, with elevated incentive levels likely to continue depending on demand and rate movement. PulteGroup's CEO made a similar point, crediting low fixed-rate mortgage incentives with helping offset affordability pressure even as those incentives compress builder margins.

Builders hate sitting on finished inventory. Every month a completed home goes unsold, it costs them — which is exactly why the most aggressive buydowns show up on standing, move-in-ready homes.

— Eric Ravenscroft, CRSThe net effect for investors who structure the deal well: some are landing at effective rates close to, or even below, what a primary-residence buyer pays on a comparable resale home. Investors working new construction inventory have reportedly stacked builder credits on top of rate buydowns to reach effective rates near 4%, and in a few cases into the high 3% range, on otherwise typical 2026 inventory.

Section 02The Investor Rate Spread, Explained

"Spread" here means the gap between what an owner-occupant pays for a mortgage and what an investor pays on the same loan amount for the same type of property. Lenders price investment loans higher because the risk profile is different — an owner-occupant is far less likely to walk away from their own home than an investor is from a rental that stops cash-flowing.

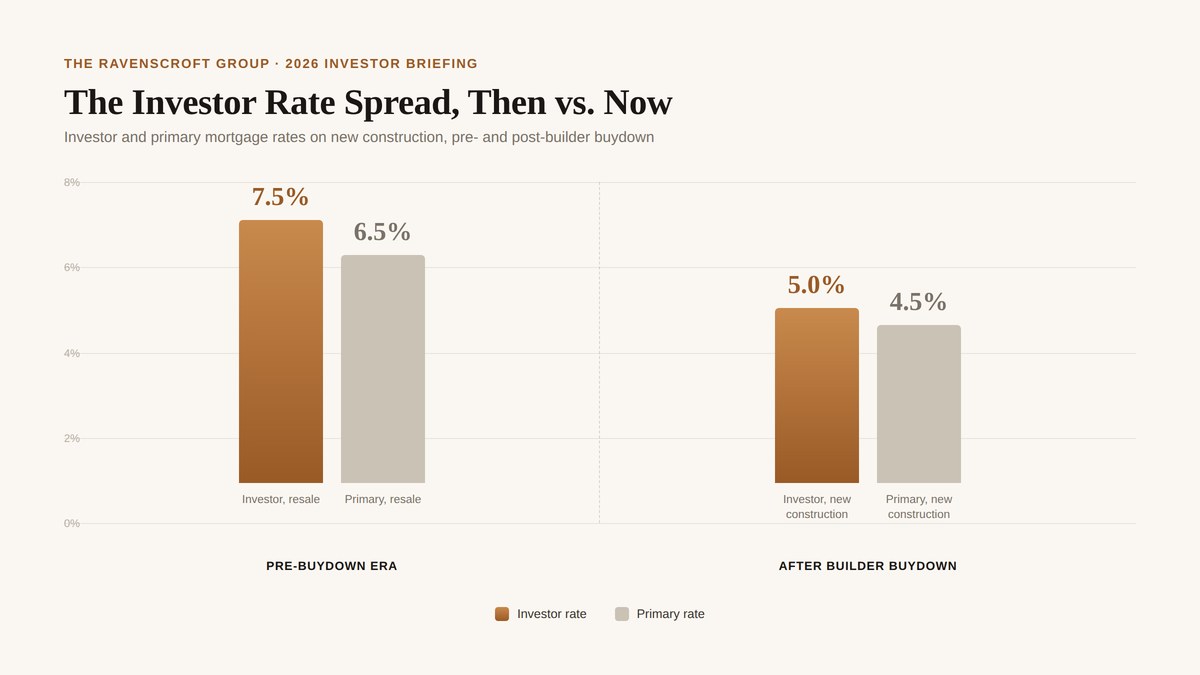

The Spread, Then vs. Now

That spread itself hasn't disappeared; it's still roughly half a point to a full point. What's changed is the base rate it gets applied to. Instead of comparing a 7%-plus investor rate to a roughly 6% owner-occupant rate, a builder-funded buydown can mean comparing a 5% investor rate to a similar primary rate. The percentage-point spread is similar, but the dollar impact on your monthly payment shrinks dramatically because both numbers moved down together.

How the buydown actually gets funded

- Permanent buydowns rely on a tool called a bulk forward commitment, where the builder pays a lender in advance to lock in a large pool of mortgage money at a reduced rate for the life of the loan. Large national builders with in-house mortgage subsidiaries are best positioned to offer these because of their scale.

- Temporary buydowns, often structured as 2-1 buydowns, reduce the rate by about 2 percentage points in year one and 1 point in year two before reverting to the full note rate. These cost builders less up front, which is why many favor them even though the long-run savings to the buyer are smaller than a permanent buydown.

- DSCR investors get an added lever. Because Debt Service Coverage Ratio loans qualify off the property's rental income rather than the borrower's personal income, redirecting a builder rate concession into a permanent buydown can also push a deal into a better DSCR pricing tier — lowering fees on top of the rate itself. One documented case moved an investor's rate from roughly 7.1% to 6.3% this way, adding more than $300 a month in cash flow per unit once the improved DSCR ratio pushed the loan into a top pricing bracket.

The Trade-Off

A buyer who takes a builder's rate buydown has typically used up their negotiating leverage in the process. They can still refinance later if rates drop further, but they no longer have the alternative of having negotiated a lower purchase price instead. It's a genuine trade-off between immediate cash flow and long-term flexibility, not a free lunch.

It's not just rate — the down payment matters too

New construction often opens financing structures that simply aren't available on resale inventory. A meaningful share of new build-to-rent product can be financed with as little as 5% down, compared with the 20–25% a conventional lender typically requires on an investment property. On a $280,000 home, that's roughly a $14,000 down payment versus $70,000 — capital an investor can redeploy into a second or third property instead of parking it all in one deal.

Builders are also layering in closing cost credits, commonly in the $6,000–$15,000 range or higher, to cover origination, title, and prepaid taxes, and in some markets a meaningful share of builders are cutting base prices by roughly 5–6% outright. Stack a closing cost credit, a permanent buydown, and a new-home warranty together, and the all-in cost of ownership in year one can look very different from the sticker price.

Section 03What I'm Seeing on Deals Right Now

Numbers like "builder buydown" can feel abstract until you see what's actually on the table. These are structures I'm currently working with clients on in the Phoenix market — illustrative of live deal types, not a guaranteed rate for any specific property, and every builder, lender, and community prices differently.

The 10-year ARM is typically reserved for a builder's most motivated communities — later phases, standing inventory the builder wants off its books before the next subdivision opens — and for an investor planning to refinance, sell, or 1031 out within that 10-year window, it can function close to a fixed rate in practice. The 30-year fixed is a true permanent buydown rather than a temporary structure. Both sit meaningfully below typical investment loan pricing right now, and in some cases below what a primary-residence buyer is getting on a comparable resale home.

Section 05Where New Construction Actually Shines

Flip the strategy, though, and new construction starts to look like one of the more compelling plays in this market. For an investor running a standard long-term lease model — twelve-month tenant, stable cash flow, minimal turnover — the HOA's rental restriction is often a non-issue, because most communities that restrict short-term rentals still permit standard annual leases. That's precisely the buyer profile new construction is built for in 2026.

Here's why the combination works:

- A lower effective rate via builder buydown, narrowing or even erasing the usual investor-rate penalty.

- Lower cash-to-close via 5%-down programs versus 20–25% on conventional investment financing.

- Builder warranty coverage that keeps early capital expenditures near zero — no surprise roof, HVAC, or water heater replacement in year one or two, unlike most resale inventory.

- A brand-new asset that rents at a premium to comparable older inventory, typically with fewer maintenance calls and stronger tenant retention.

- DSCR financing availability, qualifying off the rental income itself rather than the investor's personal income or debt-to-income ratio — particularly useful for investors actively scaling a portfolio.

Why "low capex" is more than a talking point

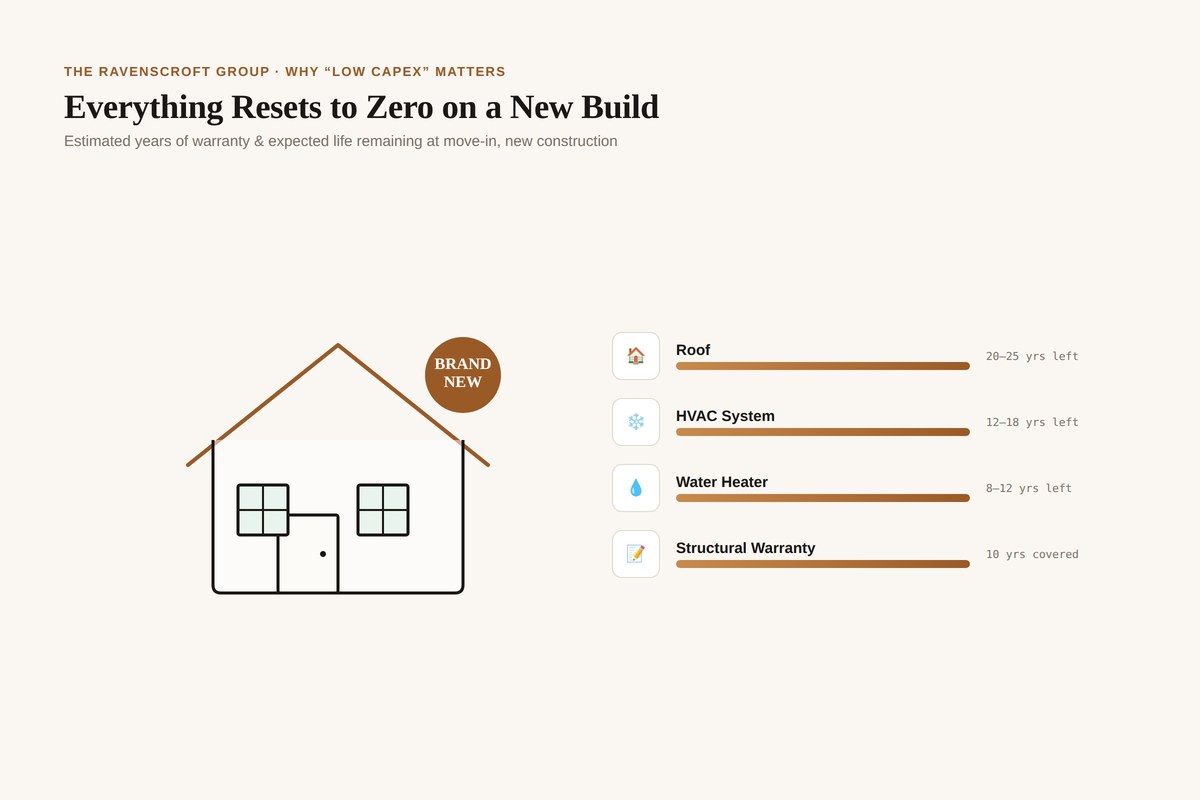

It's worth breaking down what "low maintenance" actually means in dollars, because this is one of the more underrated parts of the new construction case. A resale home, even a well-kept one, carries an inherited maintenance clock you can't see at the inspection — you don't know exactly how many years are left on the roof, the HVAC system, or the water heater, only that the clock has already been running since the home was built. A new construction purchase resets that clock to zero, and a builder's structural and systems warranty covers the years where major failures are statistically most front-loaded for a resale property.

What resets to zero on a new build

Typical replacement timeline, resale vs. new construction

| System | Typical Lifespan | Resale, Unknown Age | New Construction |

|---|---|---|---|

| Roof | 20–25 years | Could need replacement any year — $9K–$15K+ | Full lifespan ahead, typically no cost for 20+ years |

| HVAC system | 12–18 years | Often mid-life or older — $6K–$12K+ to replace | Builder-warrantied, full life expectancy ahead |

| Water heater | 8–12 years | Frequently original — $1.5K–$3K to replace | New, typically not a year-1–8 expense |

| Appliances | 10–15 years | Mixed ages, no warranty — replaced piecemeal | New, under manufacturer warranty |

| Structural & systems | 1–10 year coverage windows | No builder warranty remaining | Builder warranty typically covers 1-year workmanship, 2-year systems, 10-year structural |

Figures are general industry ranges for illustration, not a quote for any specific property — actual costs vary by market, finish level, and contractor. The point isn't that resale homes are bad investments; it's that their capex timing is unknown, while a new build's is largely deferred for years by design.

For a buy-and-hold investor, that timing matters more than it first appears. A surprise $10,000 roof or $8,000 HVAC replacement in year two doesn't just cost the repair — it erases a year or more of cash flow and can force an investor to dip into reserves earmarked for the next acquisition. A new build doesn't eliminate maintenance forever, but it pushes the highest-cost, least-predictable items years down the road, during which the investor is simply collecting rent on an asset that's behaving exactly as a brand-new home should.

Run the numbers, and the home that looks more expensive on the sticker price frequently produces a stronger cash-on-cash return than the cheaper resale alternative, once financing structure and near-term capital expenditures are factored in. The resale isn't actually cheaper to own — it just defers its costs instead of avoiding them.

This is also exactly the buyer profile builders are most motivated to work with. Every month a finished, unsold home sits on a builder's books adds carrying cost, which is the underlying reason builders are willing to negotiate aggressively with investors purchasing standing inventory or small multi-unit packages right now.

Rent Premium

Tenants consistently pay a premium to live in a brand-new home over an older one with comparable square footage — newer finishes, newer systems, and being the first occupant all factor in. Pair that rent premium with a low, builder-paid rate and a low-maintenance asset, and the cash flow math tends to be cleaner than investors expect going in.

The low effective rate also creates optionality that a 7%-plus resale purchase doesn't. With a meaningfully lower payment, you have more room to hold the property through a soft rental month, more flexibility to refinance opportunistically if rates move further, and more headroom if you decide to convert the property's use down the road, subject to the HOA's rules discussed above. A tight cash flow margin on a resale purchase doesn't leave you that same room to maneuver.

Want to See What These Rates Look Like on a Real Property?

Book a free strategy call and I'll walk you through current builder incentives in your target market.

Section 06The 1031 Exchange Playbook

A 1031 exchange lets an investor sell an investment property and defer capital gains tax by rolling the proceeds into a "like-kind" replacement property. The tool remains fully available and unchanged heading into 2026, and industry advisors continue to report strong investor demand for it as financing conditions improve.

New construction fits the 1031 buyer for a specific reason that's easy to overlook: a 1031 exchange comes with a strict 45-day identification window and a 180-day close window. Builders with standing, already-completed inventory can close fast — often faster than a custom build, and comparably fast to resale — while still offering the financing incentives described above. That combination of speed, incentive stacking, and a fresh asset with no deferred maintenance is hard to find anywhere else in the market right now.

The low-capex profile matters even more in a 1031 specifically because of how exchange capital works. You're deploying a large, often fully-tax-deferred sum into a single replacement property, frequently at or near 100% of the relinquished property's equity to avoid taking boot. That doesn't leave much room for a surprise $12,000 HVAC replacement in year two eating into the return you exchanged to protect. A new build's warranty-covered systems and multi-year runway before any major capital item comes due means the exchange proceeds go to work generating rental income from day one, rather than competing with an inherited repair bill in year one or two of ownership.

There's also a more advanced structure worth knowing: a reverse 1031 exchange, where an Exchange Accommodation Titleholder helps the investor acquire the replacement property before selling the relinquished one. This structure is specifically common in build-to-suit and new construction scenarios, where timing the purchase of a not-yet-finished home against the sale of an existing property is logistically difficult.

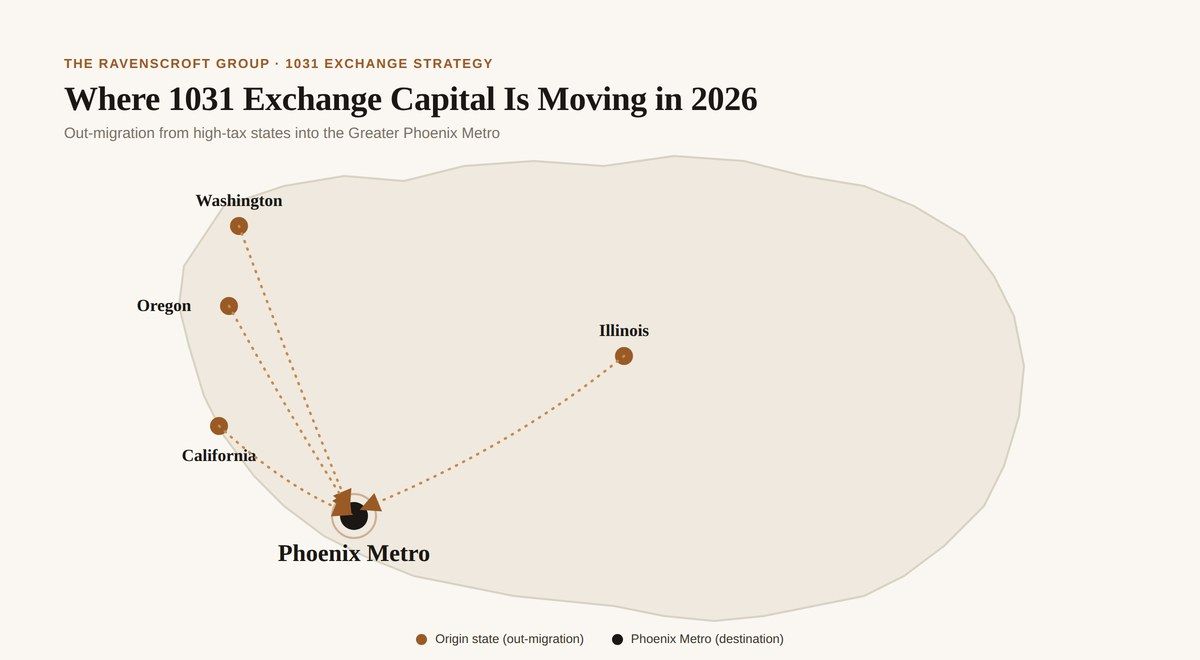

Why high-tax states are driving so much of this demand

The math behind exchanging out of certain states is straightforward and large. High-tax states — California, New York, and Oregon among them — make 1031 exchanges especially valuable because of the size of the state tax bill being deferred. As a rough illustration, a $500,000 capital gain in California can trigger upwards of $65,000 in state tax alone, on top of federal capital gains tax. Deferring that bill through a 1031 exchange preserves capital that would otherwise go straight to the state, freeing it up for redeployment into new construction with builder-funded financing incentives layered on top.

A few state-specific notes worth knowing for the markets named in this strategy:

Origin state

California

The state aggressively tracks exchanged gains even after an investor relocates. California's Franchise Tax Board takes the position that gains accumulated while an investor was a California resident remain taxable by California, even after a later move to a no-tax state. California also withholds roughly 3.33% of the sale price at closing on certain transactions, even with a properly structured exchange, requiring advance, state-specific paperwork filed before closing rather than handled at year-end. The state's Form 3840 tracks these deferred gains across tax years. A 1031 exchange can also be completed entirely within California — many Bay Area investors exchange into higher-yield Central Valley or Inland Empire new construction rather than leaving the state at all.

Origin states

Illinois, Washington & Oregon

These states are frequently named alongside California as among the primary out-migration states fueling new construction demand in faster-growing Sunbelt and Mountain West markets. Phoenix has been cited repeatedly as a landing spot, driven in large part by a wave of semiconductor-related job growth tied to major manufacturing investment in the region, which has pulled in dozens of supplier companies and tens of thousands of associated jobs.

Case in point

A documented exchange in practice

One California investor held a rental for roughly 17 years and sold at $550,000 against an original purchase price near $175,000. Without a 1031 exchange, the estimated combined tax was approximately $139,272. By exchanging the full proceeds into an Arizona replacement property with no boot taken, the tax due at the time of the exchange was $0 — and because the property is intended to pass to heirs, the deferred gain may be eliminated entirely under the stepped-up basis rules at death.

Strategy note

Diversification, not just deferral

Diversification is a stated goal, not just a tax play, for many of today's exchangers. Moving out of a single concentrated market into growing Sunbelt markets is commonly cited by industry advisors as both a risk-reduction and income-growth strategy.

If a longer-term relocation strategy is part of the plan — establishing residency in a no-income-tax state before an eventual final sale — that typically requires a year or two of documented, bona fide residency with clear ties to the new state, and should be planned with a CPA well in advance rather than assumed at the time of sale.

Exchanging Out of California, Illinois, Washington, or Oregon?

I work with out-of-state investors on Arizona replacement property every week, from identification through closing.

Section 07Decision Framework by Strategy

| Your Strategy | Fit | Why |

|---|---|---|

| Long-term buy-and-hold, 12-month leases | Strong | Builder buydowns offset the investor rate spread; HOA rules rarely restrict standard leasing |

| 1031 exchange replacement property | Strong | Fast closing on standing inventory fits the 45/180-day windows; no deferred maintenance; incentives stack with tax deferral |

| DSCR portfolio scaling | Strong | Rate buydowns can push deals into better DSCR pricing tiers, compounding the savings |

| Short-term rental (Airbnb/Vrbo) | Weak — verify | Most HOA communities restrict or ban stays under 30 days; the restriction usually overrides looser city rules |

| Mid-term / furnished rental (30–90 day) | Mixed — verify | Many of the same minimum-stay clauses that block STRs also block mid-term strategies |

| House flip / fast resale | Weak | Builders are already discounting; you're competing directly with the builder's own incentive stack on resale |

Section 08Due Diligence Checklist

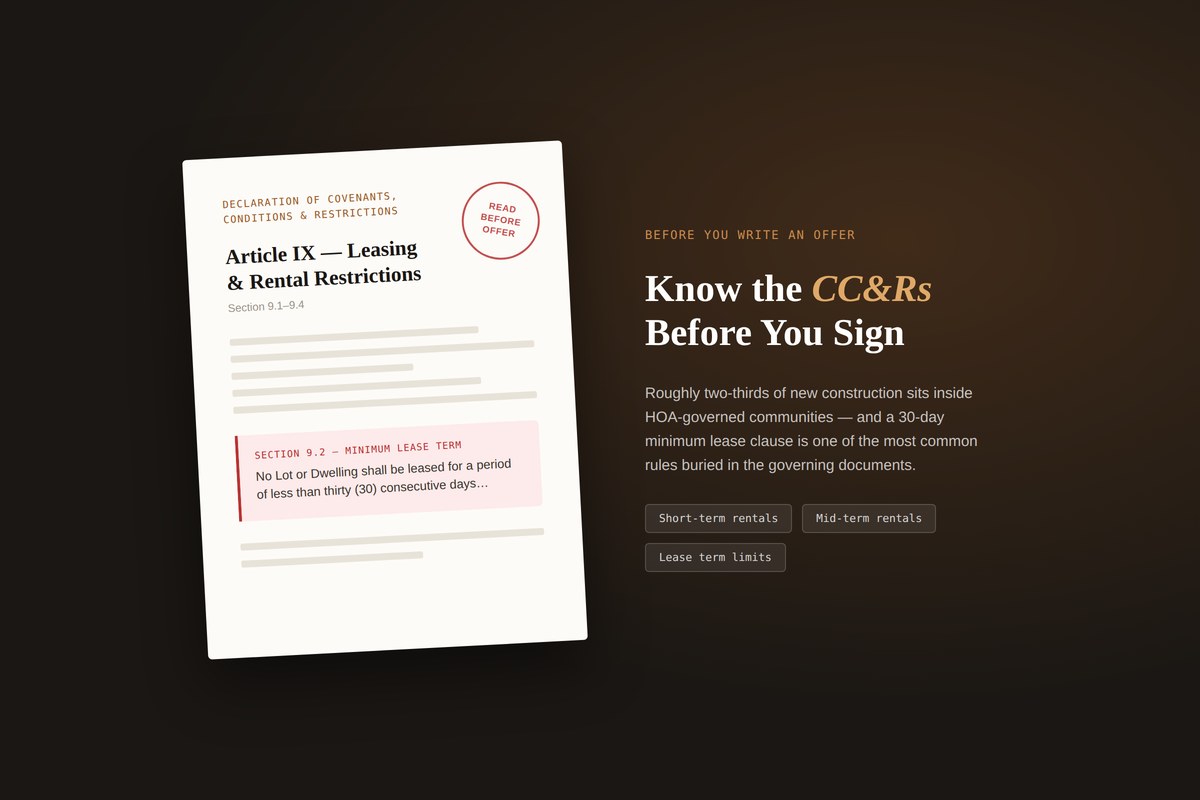

- ✓Pull the CC&Rs before you write an offer. Confirm minimum lease terms in writing, not verbally from a sales agent.

- ✓Ask whether the buydown is permanent or temporary. A 2-1 buydown's savings disappear after year two — model your cash flow at the full note rate, not just the year-one rate.

- ✓Get the DSCR math run before closing, not after, if you're financing on rental income.

- ✓Confirm the builder's incentive funding source. Some "discounts" are baked into a higher design-center markup elsewhere in the contract.

- ✓If running a 1031, line up your Qualified Intermediary and identify replacement property early — well before the relinquished property closes, given the tight 45-day window.

- ✓If residency relocation is part of a broader tax strategy, talk to a CPA in both the originating and destination state before you sell anything.

Section 09What Clients Say

★★★★★

“Last December, Eric helped us with the purchase of a new build in Buckeye. New construction is clearly his area of expertise. As an investor himself, Eric also shared valuable resources, tips, and insights that were incredibly helpful as we begin our own investment journey.”

Elda Rodriguez · New Construction, Investor Guidance

★★★★★

“As out-of-state buyers, we relied heavily on his market expertise, and his insights were consistently thoughtful, data-driven, and candid. It was clear he viewed his role not just as facilitating a purchase, but as representing us strategically and responsibly.”

Wander Inn Style · Out-of-State Investor

★★★★★

“I referred dear friends for a 1031-exchange contingent purchase from Los Angeles. Eric handled it flawlessly — negotiated carefully, maintained transparent communication with all parties, and always presented clear options, even worst-case scenarios.”

Cyndi Lesinski · Broker Associate, 1031 Referral

Section 10Frequently Asked Questions

Can investors get the same mortgage rate as primary home buyers on new construction in 2026?

Not exactly the same, but very close. Investment property loans are still priced roughly half a point to a full point above owner-occupant rates, but builder-funded permanent and temporary rate buydowns are being applied to the base rate before that spread is calculated, which can bring effective investor rates down into the 3.75–4.75% range on certain new construction inventory.

Do new construction homes allow short-term or Airbnb rentals?

Often not. Roughly two-thirds of new construction homes are built inside HOA-governed communities, and rental restrictions, frequently a 30-day minimum lease term, are among the most common rules in those governing documents. This typically blocks both short-term and many mid-term rental strategies. Always review the CC&Rs before purchasing if a short-term or mid-term rental strategy is part of the plan.

Why is new construction a good fit for 1031 exchange investors?

A 1031 exchange requires identifying a replacement property within 45 days and closing within 180 days. Builders with completed, standing inventory can close quickly, often comparably fast to resale, while also offering rate buydowns, closing cost credits, and a new-home warranty that limits near-term capital expenditures. That combination of speed and incentive is difficult to find in resale inventory.

How much can a new construction investor save on maintenance and capital expenses?

Potentially a great deal in the early years, since the timing of major repairs is the real variable. A new build resets the maintenance clock to zero: a builder's structural and systems warranty typically covers the first one to ten years, and major items like a roof (20–25 year lifespan) or HVAC system (12–18 years) are unlikely to need replacement for a decade or more. That can mean avoiding five-figure surprise repairs — commonly $9,000–$15,000 for a roof or $6,000–$12,000 for HVAC — in the exact years an investor is trying to stabilize cash flow.

Is new construction better than resale in Phoenix?

It depends on supply, incentives, lifecycle cost expectations, and long-term community trajectory. New construction often wins on financing terms and near-term maintenance; resale can win on location and lot premium. The right answer depends on your specific strategy, timeline, and the community in question.

Are builder incentives always beneficial?

Not always. Incentives must be evaluated relative to the base pricing structure and long-term resale positioning — some "discounts" are offset by a higher design-center markup elsewhere in the contract. Compare the all-in price against outside financing before assuming the builder's preferred lender is the best deal.

Related reading

Bottom Line

The builder incentive environment in 2026 has created a genuine, measurable window where new construction investment financing can rival, or even beat, what a primary residence buyer pays — something that hasn't reliably been true in years. That window is real, but it's not for every investor. If your business model depends on short-term or mid-term rental income, verify the governing documents before assuming new construction works for you; in many HOA communities, it simply won't. If you're a long-term buy-and-hold investor, and especially if you're running a 1031 exchange out of a high-tax state like California, Illinois, Washington, or Oregon, this is one of the more favorable setups the new-home market has offered investors in recent memory: fast closings, fresh assets, minimal near-term capital expenditures, and financing incentives doing real work to close the investor rate gap.

Every market, every builder, and every HOA is different. The figures and examples in this article illustrate broader 2026 market trends and are not a quote, projection, or guarantee for any specific property. Work with a licensed mortgage professional, a CPA, and a Qualified Intermediary before making investment or exchange decisions.

Let's Build a Strategy Around Your Numbers

Whether you're weighing a long-term hold, planning a 1031 exchange, or just want a current read on builder incentives in your target market, book time and we'll walk through it together.

This article was researched and compiled using current 2026 housing market reporting, builder earnings calls, HOA legal guidance, and 1031 exchange industry sources, alongside live deal terms current as of June 2026. Builder incentive structures, HOA rules, and tax law change frequently and vary by location and by builder — confirm current details with the specific builder, HOA, and your own licensed professionals before acting.

Sources

- Annie Mac — Builder Rate Relief & DSCR: Winning the 2026 Real Estate Game

- LRG Realty — Builder Incentives for New Builds in Texas (2026)

- American Enterprise Institute — Three Years Later, Permanent Rate Buydowns Continue to Prop Up New Home Prices

- Norada Real Estate — How Builders Are Lowering Mortgage Rates to Sell Move-In Ready Homes

- New Home Approval — Majority of Home Builders Are Offering Buyer Incentives in 2026

- BiggerPockets — Stop Waiting for Rates to Drop: New Construction Investors Already Bought at 4%

- The MortgagePoint — Incentives, Price Cuts Squeeze the Margins for Major Homebuilders

- AmeriSave — Restrictive Covenants in Real Estate: Your Complete 2026 Guide

- RealManage — How HOAs Can Manage Short-Term Rentals

- Tuscana Properties — California Airbnb Rules: What Homeowners and Investors Need to Know

- FirstService Residential — HOA Rental Restrictions: Everything You Need to Know

- Manning & Meyers — Legal Implications of Short-Term Rentals in HOA Communities

- Sea Crown Estates — 1031 Exchanges: For Real Estate Investors in 2026

- Madras Accountancy — State-Specific 1031 Exchange Rules: Cross-State Guide 2026

- IPX1031 — 1031 Exchange Trends and Market Update 2026

- The Ravenscroft Group — 1031 Exchange: The Complete 2026 Investor Guide

- Realized 1031 — 1031 Exchange and Out-of-State Moves

- LA Metro Home Finder — 1031 Exchange: Bay Area to Sacramento, OC & IE (2026 Guide)

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.