Depreciation, 1031 Exchanges & Step-Up in Basis: The Real Estate Tax Strategy Most Investors Miss

The Real Estate Tax Strategy Most Investors Never Learn — Until It's Too Late

Depreciation, 1031 exchanges, and step-up in basis — three tools that work together across the full lifecycle of a real estate investment. Most investors discover them too late.

|

Written by Owner, The Ravenscroft Group · Real Broker | Greater Phoenix Metro G 150+ Five-Star Google Reviews ★★★★★ Eric brings 15 years of combined experience in real estate, financial planning, and wealth management — including a background as a Director of Wealth Management. He is a Top 1% REALTOR® across North America, has closed over $100M in residential sales, and has helped clients build more than $133 million in long-term wealth. He publishes the Financial Planning Digest to share the tax and investment strategies most advisors never discuss. |

Two investors. Similar returns. Dramatically different tax bills.

This scenario plays out constantly in real estate, and it's almost never about luck. It's about whether an investor understands how the tax code treats their asset — not just in the year of acquisition, but across the full lifecycle of ownership, sale, and inheritance.

The most common misconception I encounter is that real estate investors are primarily focused on appreciation or cash flow. While both are important, many experienced investors spend just as much time evaluating the tax implications of a potential acquisition. In fact, some of the most powerful benefits associated with real estate have little to do with rental income and everything to do with how the asset is treated under current tax law.

This piece walks through all four phases — and the tax mechanics that operate at each stage.

The examples below use real-world income and property values to illustrate how these strategies work in practice. They are illustrative, not prescriptive. Tax outcomes depend on income level, filing status, state of residence, active participation qualifications, and the guidance of a qualified CPA. Nothing in this article constitutes tax, legal, or investment advice.

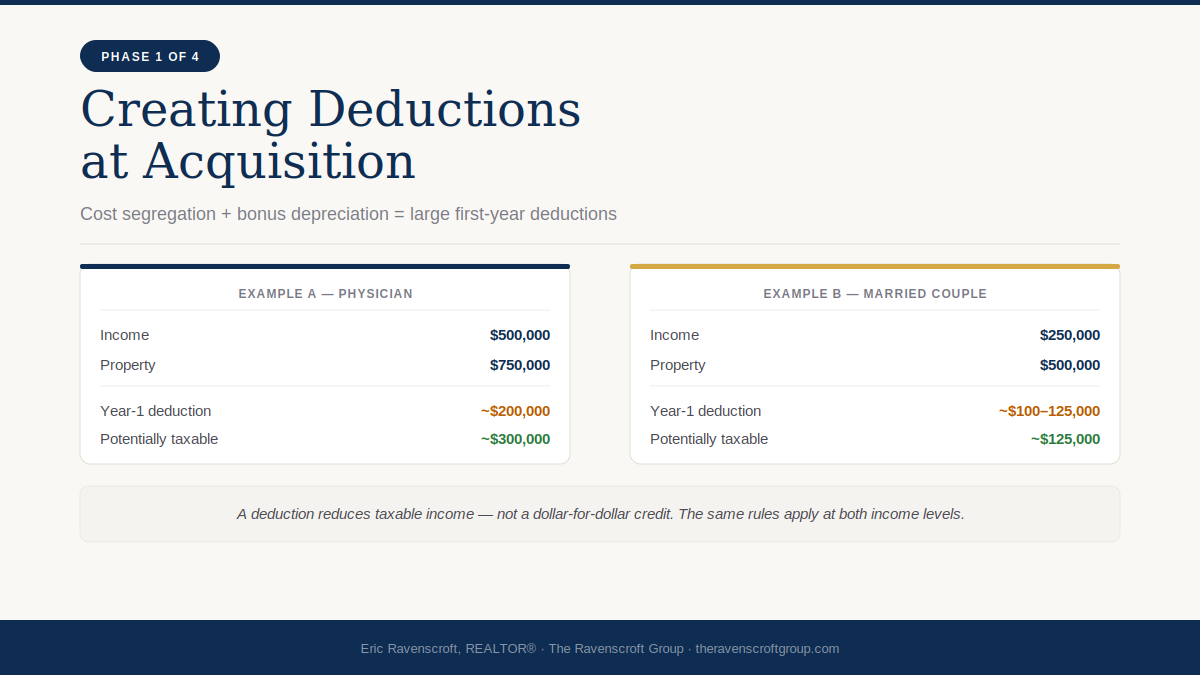

Phase 1: Creating Deductions at Acquisition

The first misconception most investors carry into real estate is that depreciation is a minor bookkeeping entry — a small annual deduction that gently reduces taxable income over three decades. The reality, particularly when combined with cost segregation and bonus depreciation, is often far more dramatic.

The IRS allows investment property owners to deduct the cost of the property's structure over time — 27.5 years for residential, 39 years for commercial. This creates annual deductions even while the property itself may be appreciating in value. Land is not depreciable; only improvements qualify.

Here is where cost segregation changes the equation. Rather than treating a building as a single asset depreciated over 27.5 years, a cost segregation study — conducted by engineers and tax professionals — identifies specific components that qualify for much faster depreciation: 5, 7, or 15 years. Components that might qualify include personal property (appliances, carpet, specialty lighting), land improvements (paving, landscaping), and certain structural elements.

When those shorter-life assets are identified and combined with 100% bonus depreciation — currently in effect as of 2026 — investors can potentially deduct a large portion of those costs in the first year. To illustrate:

The Physician Investor

The Married Couple

Important distinction: A depreciation deduction is not a dollar-for-dollar tax credit. It reduces the amount of income potentially subject to taxation. A $200,000 deduction at a 37% marginal rate could reduce federal tax liability by approximately $74,000 — but actual outcomes vary based on individual circumstances and CPA guidance.

One critical qualifier: for these deductions to offset active income — wages, business income — rather than being limited to passive losses, investors must meet specific IRS material participation requirements. Short-term rental properties have a different set of rules than long-term rentals — learn more about STR investment strategy in Arizona. This is a nuanced area that requires professional guidance specific to your situation.

Why deductions matter most at acquisition

The deduction is most powerful in the year of acquisition, when bonus depreciation is available and the asset is new on your books. In subsequent years, depreciation continues at a more modest pace. This is why timing — both of acquisition and of the cost segregation study — matters significantly to investors coordinating real estate with other income events such as a business sale or large bonus year.

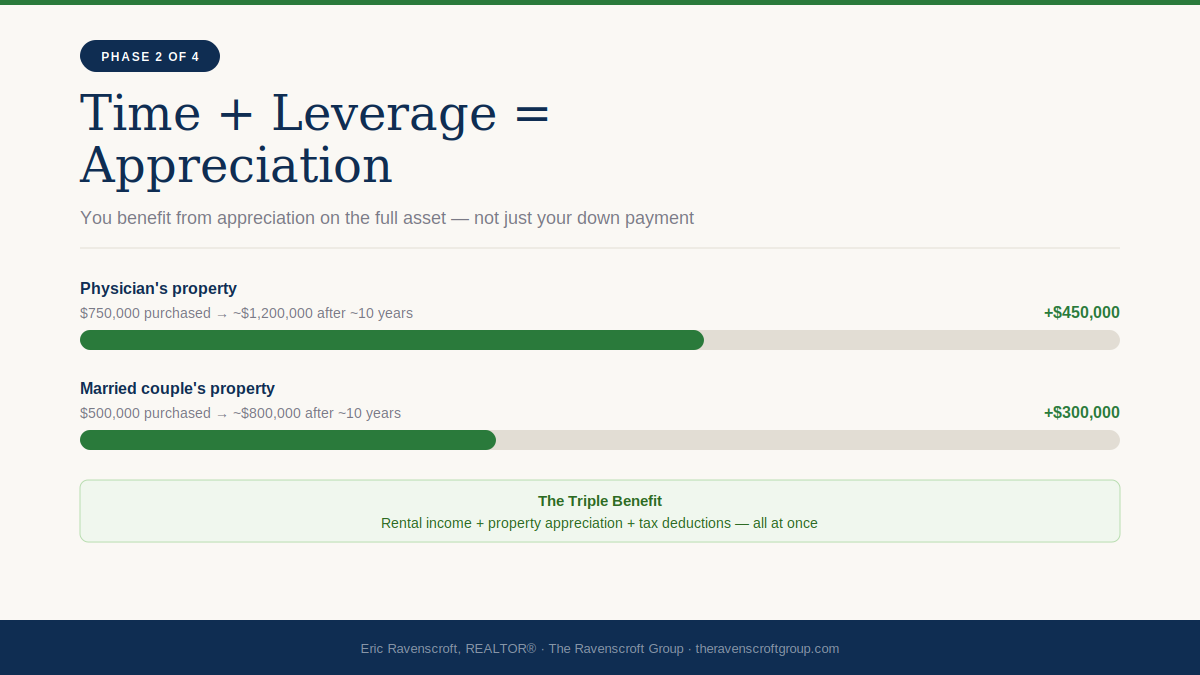

Phase 2: Allowing Time and Appreciation to Work

While depreciation dominates the early-acquisition conversation, appreciation drives most long-term wealth creation in real estate. And real estate has a feature most other investments do not: leverage amplifies appreciation returns.

When you purchase a $750,000 property with $200,000 down, you benefit from appreciation on the full $750,000 — not just the $200,000 deployed. A 10% increase in value creates $75,000 in equity — a 37.5% return on the actual capital invested. This is why well-selected real estate, held over time, has historically been one of the most powerful wealth-building tools available to ordinary investors.

Illustrative Appreciation — Held Approximately 10 Years

Illustrative only. Actual appreciation varies by market, property type, and economic conditions. Past performance does not guarantee future results. Want to estimate what a specific property could generate? Use Eric's property income calculator.

At this point both investors have accomplished something worth pausing on: they own assets that have simultaneously produced income, generated tax deductions, and increased in value. The question now becomes what to do with all that accumulated equity.

Phase 3: Sell and Pay the Tax Bill, or Defer and Keep Growing?

This is where real estate tax planning separates thoughtful investors from reactive ones. When a property has appreciated substantially, selling triggers two distinct tax events that many investors underestimate:

Capital Gains Tax

Depreciation Recapture

When you sell a property, the IRS recaptures a portion of the depreciation deductions claimed during ownership. Unrecaptured Section 1250 gain is taxed at a maximum federal rate of 25% — often higher than long-term capital gains rates. For investors who claimed large first-year deductions, this recapture can represent a substantial portion of the total tax bill. This is why exit strategy planning begins at acquisition, not at the point of sale.

The 1031 Exchange: defer instead of pay

Under Section 1031 of the Internal Revenue Code, an investor who sells a qualifying investment property can defer both capital gains taxes and depreciation recapture by reinvesting the proceeds into another qualifying investment property — subject to strict timing and identification rules.

A 1031 exchange requires a qualified intermediary — you cannot receive the sale proceeds directly. You have 45 days from closing to identify potential replacement properties, and 180 days to close. Trading into a less valuable property triggers partial gain recognition. These rules require professional coordination; errors can disqualify the entire exchange.

Returning to the physician example: after a decade, the $750,000 property has appreciated to approximately $1.2 million. Rather than selling and paying taxes on $450,000 of appreciation plus accumulated depreciation recapture, the investor exchanges into a $1.5 million property. The full equity base keeps compounding. No tax bill triggered. The married couple follows the same path — exchanging their $800,000 property into a $1 million asset.

"The taxes are not eliminated — they are deferred. But a dollar of tax deferred for twenty years is a dollar that has compounded for twenty years."

Over decades, disciplined use of the 1031 exchange allows investors to build portfolios substantially larger than would otherwise be possible. Every property sale that triggers a tax bill is a reset — capital removed from the compounding process. Every exchange is a continuation.

Phase 4: The Strategy Most Investors Never Hear About

Here is where many people's mental model of real estate taxation breaks down entirely. The assumption is this: eventually, someone pays the deferred taxes. All those years of depreciation. All the appreciated value. All the deferred recapture. At some point, there's a reckoning.

Under current U.S. tax law, in many situations, that reckoning never comes.

The mechanism is called step-up in basis, and it is one of the most significant — and least understood — provisions in the entire tax code.

When investment property is inherited, the heir's tax basis is generally reset to the property's fair market value at the date of the original owner's death — not the original purchase price.

If the heir sells at $3,000,000, there is no capital gain and generally no depreciation recapture — because both are measured against the new, stepped-up basis. Under current law, decades of deferred gains may simply disappear at the step-up. Tax law is subject to change; consult a qualified estate planning attorney.

Think about what this means viewed across the full lifecycle. The investor may have received large depreciation deductions for decades. The assets may have appreciated substantially. Taxes may have been deferred through multiple exchanges. Yet the heirs may inherit the assets with a new basis — and potentially sell them without paying taxes on gains that accumulated during the original owner's lifetime.

The same principle applies to the married couple earning $250,000 annually. Their portfolio may be smaller, but the rules operate identically. This is why many experienced investors don't view real estate simply as an investment. They view it as a long-term wealth transfer strategy.

Save and share each phase image individually — right-click to save.

Acquisition: the deduction phase

Large first-year depreciation deductions via cost segregation and bonus depreciation potentially reduce taxable income by $100,000–$200,000+ depending on property value.

Ownership: the income and appreciation phase

The property generates rental income, appreciates in value, and builds equity — often using leverage that amplifies returns on invested capital.

Exchange: the deferral phase

Rather than selling and paying taxes, the investor exchanges into a larger property via 1031. Capital gains and depreciation recapture are deferred while the full equity base continues compounding.

Estate: the potential elimination phase

Assets pass to heirs with a step-up in basis. Under current law, deferred capital gains and accumulated depreciation recapture may be substantially reduced or eliminated at inheritance.

These Strategies Are Not Reserved for the Wealthy

As soon as the physician example appears, a percentage of readers disengage. They assume these strategies require a $500,000 income or a $750,000 investment property. They do not.

The married couple earning a combined $250,000 follows the identical strategy on a different scale. Their deductions are smaller. Their appreciation is measured in hundreds of thousands, not millions. But every rule, every mechanism, every phase operates the same way for them as it does for the physician.

The rules governing depreciation, 1031 exchanges, and step-up in basis have no income floors that exclude middle-class investors. What they have are qualification requirements, participation tests, and procedural rules that require competent professional guidance — regardless of whether you're a physician or a dual-income family anywhere in the country.

The numbers may be different. The principles are identical. Many people assume these strategies are reserved for the ultra-wealthy. If you're wondering where to start, explore Eric's personal financial planning approach. In reality, they are available to ordinary investors who take the time to understand how the rules work and who build the right team of advisors around them.

What This Article Cannot Tell You

Tax law is not one-size-fits-all. Several variables determine whether and how these strategies apply to any specific investor.

Passive activity rules. Depreciation deductions from rental properties are generally classified as passive losses, which can typically only offset passive income. Exceptions exist — the short-term rental exception, real estate professional status — but these require meeting specific IRS tests that depend heavily on individual circumstances and documentation.

The future of step-up in basis. Current law provides for step-up in basis, but this provision has been discussed as a potential target for future legislation. Estate plans built around it should be reviewed periodically with an estate planning attorney.

State taxes. Federal rules are just one layer. Several states — California notably — do not conform to federal bonus depreciation rules. State tax implications must be analyzed separately from federal strategy.

Depreciation recapture follows the chain. Even within a 1031 exchange strategy, recapture is deferred, not eliminated. An investor who eventually sells without exchanging will face recapture on all accumulated depreciation from all prior properties in the exchange chain.

Questions About Your Specific Situation?

Every investor's tax picture is different. Income level, filing status, current holdings, state of residence, and long-term goals all shape which of these strategies makes sense — and in what sequence. Whether you're considering your first investment property, evaluating a 1031 exchange, or thinking about how real estate fits into your estate plan, I'm happy to be a starting resource for that conversation.

Schedule a Conversation →Frequently Asked Questions

What is a cost segregation study and do I need one?−

What is the difference between a tax deduction and a tax credit?−

What qualifies as a short-term rental for tax purposes?−

What is material participation and how do I qualify?−

Can I do a 1031 exchange into a different property type?−

What happens to depreciation recapture in a 1031 exchange?−

Is 100% bonus depreciation still available in 2026?−

What is depreciation recapture and at what rate is it taxed?−

Can step-up in basis be eliminated by future legislation?−

Are these real estate tax strategies only for high-income earners?−

Do I need a team of advisors, or can I do this on my own?−

How does leverage amplify real estate returns compared to other investments?−

Key Terms Glossary

|

Related Resources from The Ravenscroft Group |

||

|

||

|

||

|

||

|

||

|

|

|

About the Author Owner, The Ravenscroft Group · Real Broker | Greater Phoenix Metro Eric Ravenscroft is a Top 1% REALTOR® across North America and the founder of The Ravenscroft Group with Real Broker in Arizona. With 15 years of combined experience in real estate, financial planning, and wealth management — including roles as an advisor, branch manager, and Director of Wealth Management overseeing $8.5 billion in assets — Eric brings a uniquely analytical and strategy-driven perspective to real estate investing. He has closed more than $100 million in residential sales and has helped clients create over $133 million in long-term wealth. Eric publishes the Financial Planning Digest monthly to share the strategies most advisors never bring to the table. |

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.