Short-Term Rental Tax Loophole (2026): How to Offset W-2 Income with Bonus Depreciation

Short-Term Rental Tax Loophole (2026): How to Offset W-2 Income with Bonus Depreciation

How high-income earners can use the IRS's short-term rental classification exception, material participation, and 100% bonus depreciation to accelerate capital — structured correctly and documented for audit defense.

15 years spanning real estate acquisition, wealth management, and investment portfolio structuring for high-income professionals. Eric has guided clients through multi-million-dollar STR acquisitions integrating cost segregation, bonus depreciation timing, and 1031 exchange strategy. Featured in the Wall Street Journal, MarketWatch, MSN, and Morningstar. Licensed in Arizona (SA691304000) with Elite status at Real Broker.

- Why this strategy matters right now

- The legal foundation — why STRs are different

- The 7-day rule and average period of customer use

- Material participation — the gatekeeper

- 100% bonus depreciation (current law)

- Cost segregation — the acceleration engine

- Expert perspective: CPA commentary

- Real-world case studies

- Common mistakes that create exposure

- Audit defense checklist

- Frequently asked questions

Why This Strategy Matters Right Now

High-income earners face a familiar challenge: heavy W-2 taxation, limited deductions, reduced ability to shelter income, and rising federal and state tax exposure. Most traditional tax strategies phase out as income rises.

The short-term rental (STR) tax strategy sits at the intersection of IRS passive activity rules (§469), the "average period of customer use" exception, material participation standards, cost segregation engineering, and 100% bonus depreciation under current law.

When structured correctly, a short-term rental may generate real cash flow, accelerate depreciation, potentially offset active income, improve after-tax return on capital, and increase liquidity during peak earning years.

This is not tax avoidance. It is alignment with how the IRS classifies certain short-duration rental activities — a distinction upheld in multiple Tax Court cases and explicitly addressed in IRS Publication 925.

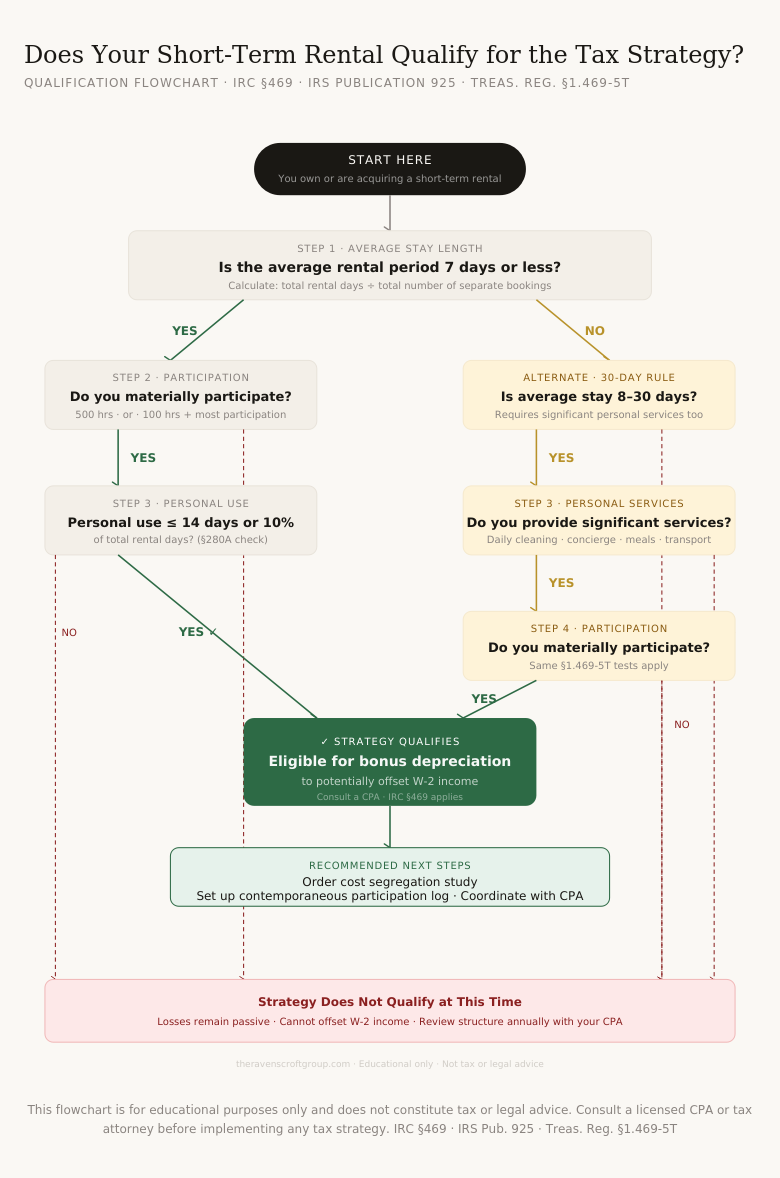

The Legal Foundation — Why STRs Are Different

Under Internal Revenue Code §469, rental activities are generally treated as passive. Passive losses cannot offset W-2 wages or active business income.

However, IRS Publication 925 (Passive Activity and At-Risk Rules) states that an activity is not treated as a rental activity if:

- The average period of customer use is 7 days or less, OR

- The average period is 30 days or less and significant personal services are provided

If the activity is not treated as a rental activity, it is evaluated under standard material participation rules. That shift — from "rental activity" to "trade or business activity" — is the foundation of the STR tax strategy.

IRC §469(c)(2) and Treas. Reg. §1.469-1T(e)(3) govern when a rental activity is recharacterized. IRS Pub. 925 translates these rules for practitioners. The IRS has litigated this classification in cases including Eger v. Commissioner and Langille v. Commissioner, both of which turned on average rental period documentation.

The 7-Day Rule — Average Period of Customer Use

The IRS uses the term average period of customer use, which equals:

This must be calculated annually. If your average exceeds 7 days in any given year, classification may change and losses may revert to passive. Precision matters.

The 30-Day Exception and Significant Personal Services

If the average rental period is 30 days or less, qualification requires significant personal services. Routine services do not qualify — cleaning between guests, trash removal, landscaping, maintenance, and providing linens at check-in are all excluded. Services that may qualify include daily cleaning, concierge services, meals, transportation, and hospitality-level services. Most investors structure under the 7-day rule rather than rely on this exception.

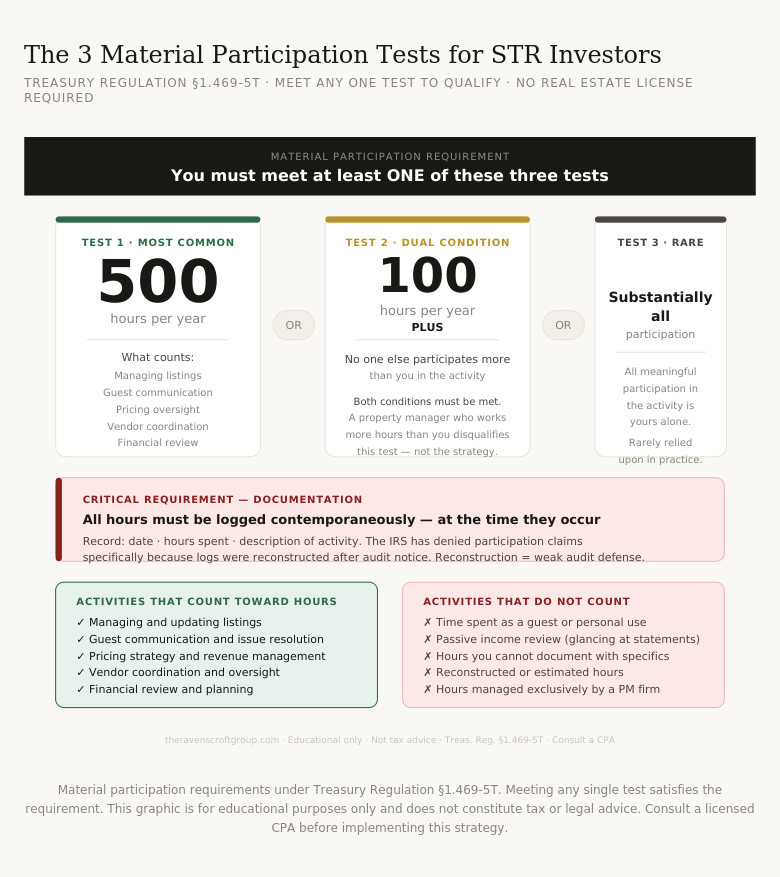

Material Participation — The Gatekeeper

You do not need to qualify as a Real Estate Professional. Instead, you must meet one of the material participation tests under Treasury Regulation §1.469-5T.

- 500 hours of participation in the activity

- 100 hours AND no one else participates more than you

- Substantially all participation in the activity is yours

Qualifying participation may include managing listings, guest communication, pricing oversight, financial review, vendor coordination, and strategic decisions.

Maintain contemporaneous logs — recorded at the time, not reconstructed later — including the date, hours spent, and description of each activity. The IRS has denied material participation claims specifically because logs were reconstructed after audit notice. Documentation determines defensibility.

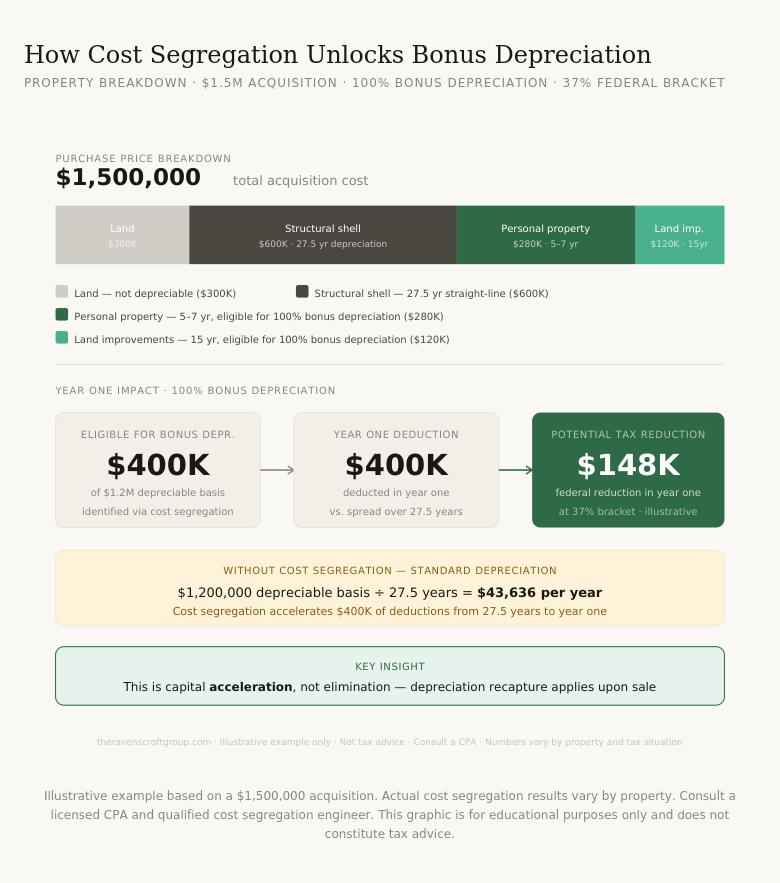

100% Bonus Depreciation — Current Law

Under current IRS guidance, the One Big Beautiful Bill Act restored a permanent 100% additional first-year depreciation deduction for qualified property acquired after January 19, 2025. This applies to property with a recovery period of 20 years or less and certain qualified improvement property.

It does not apply to land or the structural building shell (27.5-year residential rental property). This is where cost segregation becomes essential.

Depreciation begins when the property is ready and available for rent — not when you close escrow. If a property closes in December but is not listed until January, depreciation begins in January. This timing directly affects year-one tax modeling.

Cost Segregation — The Acceleration Engine

A cost segregation study is an engineering analysis that reallocates components of a property into shorter depreciation lives — typically 5-year, 7-year, and 15-year land improvements — making them eligible for 100% bonus depreciation in year one.

Personal Use and Vacation Home Rules

If personal use exceeds the greater of 14 days or 10% of total rental days, vacation home rules under IRC §280A may limit deductible losses and reduce the depreciation benefit. Clear separation of personal and rental use is critical to preserving the strategy.

Schedule E vs. Schedule C

Most STRs report on Schedule E. If substantial services are provided primarily for the guest's convenience, income may shift to Schedule C and trigger self-employment tax — an unintended consequence that careful structuring avoids. See IRS Topic 414 for full treatment.

Net Investment Income Tax (NIIT)

Passive rental income is generally subject to the 3.8% NIIT. If the STR qualifies as non-passive through material participation, NIIT exposure may be reduced — but this is fact-specific and requires CPA coordination.

State Conformity

Not all states conform to federal bonus depreciation rules. Several states decouple, require add-back adjustments, or phase deductions differently. Always model state-level impact before projecting after-tax return.

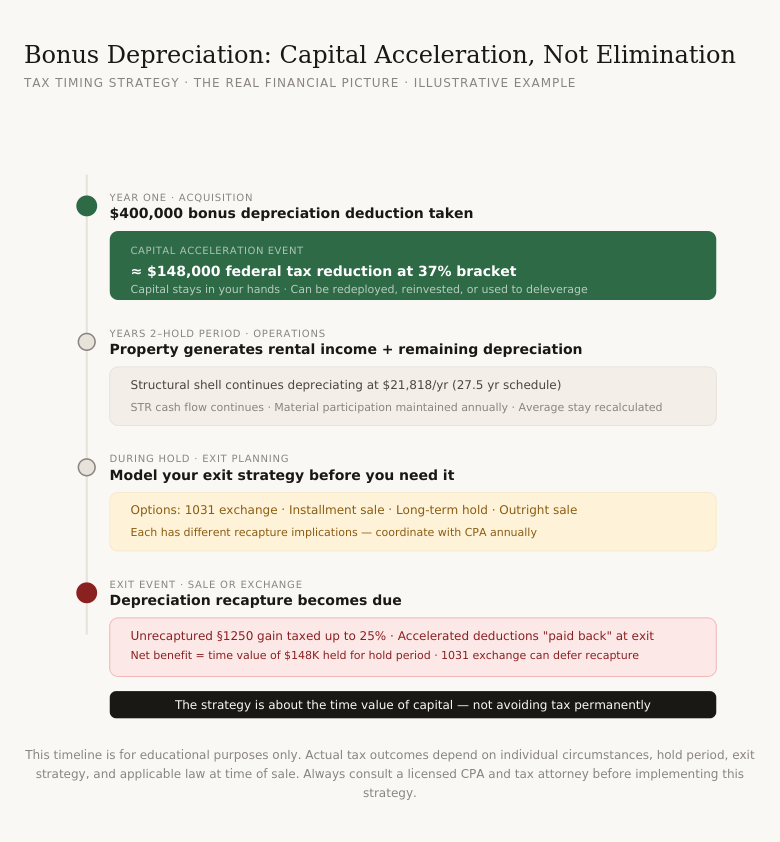

Depreciation Recapture and Exit Planning

Upon sale, depreciation is recaptured — unrecaptured Section 1250 gain may be taxed at up to 25%. Common planning tools include a 1031 exchange, long-term hold strategy, or installment sale planning. This is timing optimization, not permanent tax elimination.

Expert Perspective: CPA Commentary

"The STR classification exception is one of the most misunderstood provisions in passive activity law. When properly documented, the strategy is technically sound — but the IRS scrutinizes it heavily. The two failure points we see consistently are average stay calculations that are off by even a fraction of a day, and participation logs that were clearly written after the fact. Investors who maintain airtight contemporaneous records and work with a qualified cost segregation firm generally hold up very well in examination."

Eric works alongside clients' existing CPAs and tax counsel during acquisition structuring. The real estate analysis — property selection, revenue modeling, participation planning — integrates directly with the tax professional's depreciation and cost segregation projections.

Real-World Case Studies

Understanding how this strategy works in theory is important. Seeing how it plays out in real transactions is more valuable. The following examples reflect actual client engagements structured with STR classification and bonus depreciation as part of the acquisition plan.

When This Strategy Did Not Make Sense

Not every property qualifies — and sometimes the right guidance is to walk away. In one engagement, a high-income buyer considered a $2.3M luxury STR in a competitive vacation market. While cost segregation projected substantial accelerated depreciation, revenue modeling showed inconsistent occupancy assumptions, elevated operating expenses, and a narrow margin after debt service. The numbers worked only if depreciation was the primary driver. After modeling recapture exposure and long-term exit sensitivity, the acquisition was not recommended. Disciplined capital allocation sometimes means walking away.

Common Mistakes That Create Exposure

The strategy itself is legitimate. Execution errors are where investors create audit exposure and real financial risk.

If the average period of customer use exceeds 7 days, classification may shift and losses remain passive. The platform doesn't matter — the IRS looks at average stay length, calculated annually from booking records.

Hours must be logged as they occur. Reconstructed logs are weak audit defense and have been rejected by the Tax Court. Use a dedicated time-tracking method from day one.

Exceeding 14 days or 10% of rental days may trigger vacation home rules under §280A, limiting losses and reducing the depreciation benefit. Maintain clear separation between personal and rental use.

If the property only "works" because of the depreciation, risk is elevated significantly. The investment must stand on its own merit — cash flow, appreciation potential, exit flexibility — before the tax layer is added.

Accelerated depreciation improves early liquidity, but recapture must be modeled at exit before acquisition. Unrecaptured §1250 gain taxed at up to 25% can significantly alter after-tax returns on sale.

Some states decouple from federal bonus depreciation and require add-back adjustments that can materially reduce projected benefit. Model state impact before finalizing acquisition economics.

Audit Defense Checklist

The strategy is legitimate. Documentation is what makes it defensible. Maintain all of the following:

- ✓Annual average period of customer use calculations (from booking export data)

- ✓Booking platform export reports showing all rental periods

- ✓Contemporaneous material participation logs (date, hours, description of activity)

- ✓Personal use log showing dates used by owner/family

- ✓Cost segregation engineering report from a qualified firm

- ✓Vendor invoices and receipts supporting participation claims

- ✓Schedule E filing consistent with non-passive treatment

- ✓CPA sign-off on classification and bonus depreciation election

Frequently Asked Questions

Schedule a Strategy Session

If you're evaluating whether a short-term rental tax strategy fits your income profile, we review your participation feasibility, conservative revenue modeling, cost segregation potential, and exit planning — before you make any acquisition decision.

Book a Session

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona's most trusted real estate strategists. With 15 years of experience spanning real estate acquisition, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions — from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric's expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. He holds the Certified Residential Specialist (CRS) designation and is licensed in Arizona (SA691304000).

Last updated: March 2026. Tax law is dynamic. Bonus depreciation provisions, passive activity rules, and state conformity requirements are subject to change. Verify all tax information with a licensed CPA and/or tax attorney before taking action.

© 2026 The Ravenscroft Group · Eric Ravenscroft, CRS · AZ License SA691304000 · Privacy & Terms

Related: Palm Valley Case Study · Scottsdale 85254 Case Study · STR vs MTR Comparison · 1031 Exchange Guide

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.