Phoenix Metro Housing Market May 2026: What Buyers, Investors & Sellers Need to Know

Phoenix Metro Housing Market May 2026:

What Buyers, Investors & Sellers Need to Know

More inventory, stubborn rates, record luxury sales, and a short-term rental boom happening all at once. Here is the complete picture — every segment, every major city, and exactly what you should do right now.

The Greater Phoenix housing market continues sending mixed signals depending on where you look or who you ask. One headline says inventory is surging. Another says Arizona is still critically undersupplied. Mortgage rates keep bouncing. Some homes are selling immediately. Others are sitting through multiple price reductions.

I am here to give you the facts.

This is not a frozen market. It is not a collapsing market. And it is definitely no longer behaving as one unified market. What we have in May 2026 is a market that has become more selective, more localized, and much more strategy-driven than it has been in years.

01 A Market That Continues to Move

Buyer activity throughout May remained stronger than many expected despite mortgage rates pushing back toward the upper-6% range. Accepted contracts and homes under contract are running above last year's pace. Closed sales activity continues outperforming expectations heading into summer.

That is important because elevated rates would normally slow demand much more aggressively. Instead, buyers appear to be adapting rather than stepping away altogether. The focus has shifted toward long-term value and monthly affordability rather than perfectly timing the market.

The urgency from 2021 and 2022 may be gone, but demand itself has not disappeared. Today's buyers are more deliberate. They are comparing options more carefully, negotiating harder, and paying much closer attention to value, condition, location, and long-term affordability.

Homes priced correctly and presented well are still moving. Homes that miss the mark are being exposed much faster than they would have been even a year or two ago.

Many of the homes seeing the strongest activity right now are not necessarily the "perfect" homes — they are the homes where buyers feel the pricing reflects current market realities. That distinction matters enormously in today's environment.

02 The Inventory Story Requires Context

Inventory continues to dominate conversations throughout the Valley, but much of the public discussion lacks the historical perspective needed to interpret it correctly.

Yes, inventory has increased compared to the historically tight conditions of the pandemic years. Buyers today have significantly more options than during 2021 and early 2022. But current supply levels are still nowhere close to what Greater Phoenix experienced during the housing collapse between 2006 and 2008, when active listings exceeded 50,000 across the metro.

At the same time, Arizona continues dealing with a longer-term housing shortage created by years of population growth and underbuilding. Labor shortages, higher financing costs, and zoning bottlenecks mean single-family permits remain well below the pace of the early 2000s — creating a supply floor that helps explain why pricing has remained surprisingly stable despite affordability pressure.

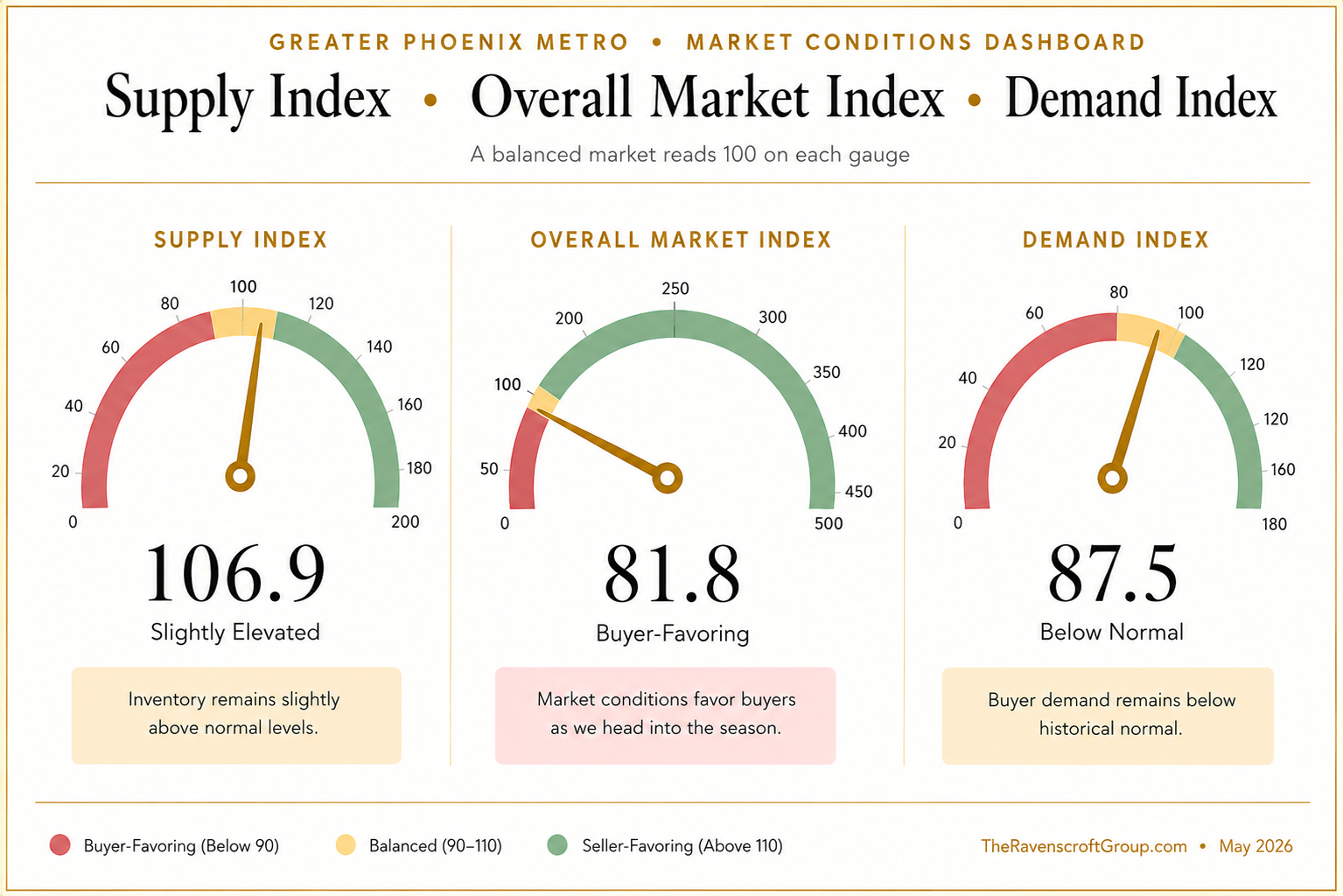

The market is absorbing inventory rather than unraveling under it. The median sales price sits near $457,250 with average price per square foot remaining relatively flat year over year. That is stability — not collapse.

This market may feel slower than the frenzy years — but slower does not automatically mean weak. In many ways, this feels more like normalization after one of the most aggressive housing runs Phoenix has ever experienced.

Overall market position — seller vs. buyer leverage

Metro-wide average leans slightly buyer-favorable. Conditions vary significantly by submarket and price point — see city breakdown below.

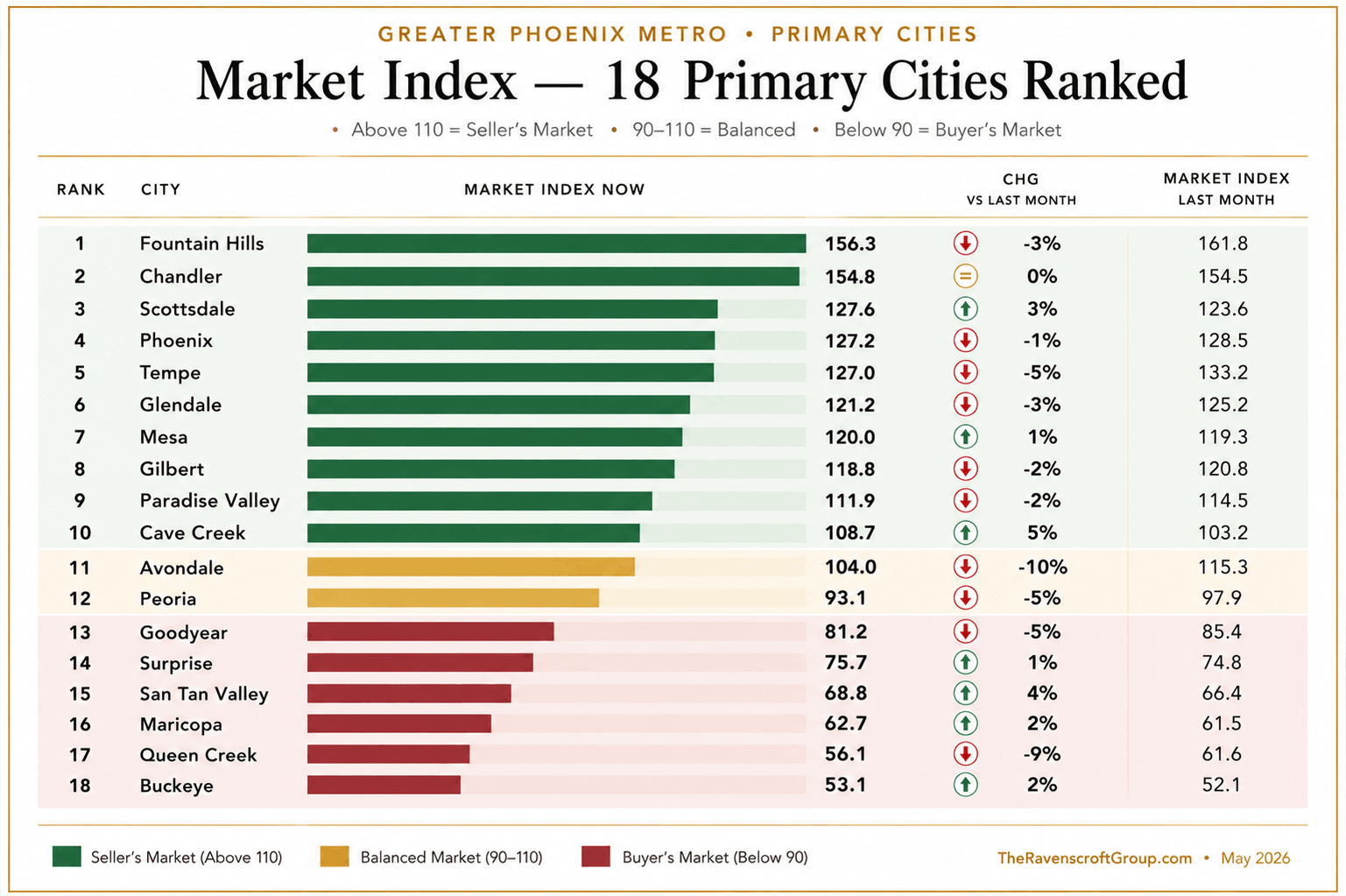

03 The Market Has Become Extremely Localized

Different parts of the Valley are behaving very differently right now — and that separation has only become more noticeable over the past several months. Broad statements about "the Phoenix market" are increasingly misleading. Two homes at similar price points, only a few miles apart, can experience completely different levels of activity depending on the neighborhood, product type, and nearby competition.

| City / Area | Conditions | What's Happening |

|---|---|---|

| Scottsdale | Seller | North Scottsdale especially strong. Luxury demand keeps inventory constrained. Multiple-offer scenarios still occurring in guard-gated communities. |

| Paradise Valley | Seller | Ultra-luxury activity near record levels. Cash and equity buyers dominate. Watch for summer supply tightening — it happened here last year and shifted leverage back to sellers. |

| Chandler | Seller | Tech corridor employment anchors demand. Inventory relatively controlled at mid-to-upper price points. Southeast Valley continues to outperform. |

| Gilbert | Seller | Family demand remains strong. Higher-end single-family resale performing well. HOA-heavy condo inventory showing more softness. |

| Tempe / Mesa | Balanced | Competitive near light rail and ASU corridor. Mid-priced single-family holding fairly steady. Some pockets softening below $350K. |

| Phoenix Core / Arcadia | Balanced | Infill pockets remain structurally tight — no new inventory being built here. Arcadia-Biltmore holding premium. Supply floor is structural, not cyclical. |

| Avondale / Cave Creek | Balanced | Constrained resale inventory keeps conditions balanced. Good entry-level opportunity. Watch for builder competition from nearby outer markets. |

| Buckeye / Goodyear | Buyer | Best negotiating leverage in the metro. Builder competition creating strong concession packages — price reductions plus rate buydowns available. Most sq footage per dollar in the Valley. |

| Queen Creek / San Tan | Buyer | Outer markets giving buyers meaningful flexibility. New construction incentives still aggressive. Run the full monthly cost including HOA before committing. |

| Maricopa | Buyer | Extended days on market. Motivated sellers. Best combination of price, square footage, and land for budget-conscious buyers or investors in the greater metro. |

04 Mortgage Rates: The Controlling Variable

Mortgage rates continue shaping much of the psychology surrounding today's market. As of May 27, 2026, the 30-year fixed in Arizona sits at approximately 6.50%, with some lenders quoting higher depending on credit profile and loan type. The 15-year fixed has improved to around 6.0%, and ARM products are available in the 6.3–6.6% range.

Rates briefly moved closer to 6% earlier this year before climbing back, creating renewed hesitation among some buyers. What feels different now is that buyers no longer appear shocked by rates. Instead, many are simply waiting for a better window. That creates pent-up demand that could release quickly if rates improve even modestly.

In many conversations lately, buyers are not asking whether they should buy. More often, they are asking whether now is the right time for their specific situation — a very different mindset than the emotional urgency of several years ago.

| Loan Type | Rate (May 27, 2026) | Est. Monthly Payment* | Trend |

|---|---|---|---|

| 30-yr Fixed | 6.50% | ~$2,340 | Elevated |

| 15-yr Fixed | 6.00% | ~$3,060 | Improving |

| 5/1 ARM | 6.29% | ~$2,270 | Stable |

| 2-1 Buydown (yr 1) | ~4.5% | ~$1,950 yr 1 | Seller-paid |

*Based on $457,250 purchase, 20% down (~$366K loan). Sources: Zillow, Rocket Mortgage, Curinos/Experian, May 27, 2026.

05 New Construction vs. Resale

The separation between new construction performance and resale continues widening throughout 2026. Builders are still heavily relying on incentives across many parts of the Valley — rate buydowns, closing cost assistance, upgrade packages, and flexible financing continue playing a major role in driving buyer activity.

At the same time, resale homes are beginning to compete much more effectively again. Buyers are weighing the advantages of completed landscaping, mature communities, lower carrying costs, and avoiding the delays, uncertainty, and upgrade expenses that can come with building new.

Many buyers initially assume new construction automatically provides the better deal. After comparing total monthly costs, lot premiums, upgrades, landscaping, and timelines, resale homes are often far more competitive than expected — especially in established core submarkets. Run the side-by-side numbers on every scenario before deciding.

Some builders have become extremely competitive while others have scaled incentives back significantly. In some outer-market areas, I've recently had clients secure combinations of significant price reductions, financing incentives, and additional concessions that created substantial savings. In others, the resale clearly wins on total monthly cost.

06 Luxury & Ultra-Luxury Market

The luxury segment is operating in a fundamentally different market than the rest of Greater Phoenix — and it is one of the few tiers where conditions are genuinely seller-favorable at scale.

Sales above $1 million remain among the strongest-performing segments across the Valley. The ultra-luxury market ($3M+) continues seeing some of its best activity in years. Cash-heavy buyers and stock-market wealth continue playing a major role, making that segment far less sensitive to mortgage rate fluctuations than the broader market.

Many luxury buyers still view Phoenix as relatively undervalued compared to California and Colorado — particularly for waterfront, golf course, and guard-gated product in North Scottsdale and Paradise Valley.

Last summer, Paradise Valley saw supply tighten faster than expected as listing cancellations picked up with the heat — temporarily shifting leverage back to sellers. It would not be surprising to see that pattern emerge again in June and July 2026. Buyers in this segment should be prepared to act quickly if that window opens.

Condos and townhomes, by contrast, remain more challenging. HOA fees that have risen substantially over the past several years are beginning to impact buyer demand almost as much as mortgage rates themselves in some communities — particularly in the $300K–$450K range.

07 The Return of the Short-Term Rental Buyer

The increase in buyers searching for short-term rental eligible properties has become very noticeable in 2026. Honestly, this has been one of the strongest starts to the year for STR-focused acquisitions that I can remember in quite some time.

The accelerant is bonus depreciation. High-income earners who qualify as real estate professionals or meet material participation requirements can use cost segregation and accelerated depreciation to generate substantial first-year write-offs. The tax efficiency has attracted physicians, business owners, tech executives, and high-income W-2 earners in growing numbers. Here are two real-world illustrations:

~$500,000 purchase

$35,000–$55,000 in projected tax savings

Based on projected cost segregation and accelerated depreciation. Assumes 32–37% bracket and material participation. Consult your CPA — results vary significantly.

~$1,000,000 purchase

$80,000–$100,000+ in projected tax savings

Includes structure, furnishings, and improvements. Assumes 35–37% bracket. Individual CPA guidance is essential — this is illustrative only.

The strongest STR acquisition activity is concentrating in Scottsdale (Old Town, resort corridors, STR-zoned neighborhoods), select Tempe and downtown Phoenix neighborhoods with strong conference demand, and Sedona-adjacent properties for weekend leisure traffic. Supply of quality STR-eligible locations is competitive enough that early positioning still matters.

08 Guidance: Buyers · Sellers · Investors

The market looks different depending on what you are trying to accomplish. Here is the practical breakdown for each situation.

The conflicting inventory narrative has created unnecessary confusion. The truth: you have more choices today than at any point since 2019, prices have held relatively stable for two-plus years, and more than half of sellers are actively offering concessions. That combination is genuinely favorable — but only if you know how to use it.

Rate buydowns are your first ask on every offer. A seller-paid 2-1 buydown — often costing them $8,000–$12,000 — can lower your effective rate by two full points in year one. Far more impactful than a small price reduction, and many sellers will say yes because it keeps their headline number intact.

Your leverage is highest in the outer markets. Buckeye, Goodyear, Queen Creek, Maricopa, and San Tan Valley are giving buyers the most negotiating room right now. If location flexibility exists, these markets offer the best combination of price, square footage, and concession potential in the Valley.

Waiting for 5% rates is increasingly costly. Buyers who held out through 2023–2025 watched prices hold. Long-term value and monthly affordability — not market timing — should drive the decision.

Strong moves for buyers right now

- Ask for seller-paid rate buydown on every offer — over half will say yes

- Compare builder incentives vs. resale on total monthly cost, not just list price

- Run full HOA cost analysis on any condo or townhome before writing an offer

- Check price reduction history on anything with extended days on market

- Use Coming Soon listings to preview before the DOM clock starts running

The peak spring season is beginning to wind down, but overall sales activity is still running ahead of last year — particularly in the luxury segment. The sellers winning right now priced correctly from day one, invested in presentation, and used strategic concessions intentionally.

Days on market is the most expensive metric you can ignore. Every week a home sits without going under contract, it loses negotiating leverage and accumulates buyer skepticism. Overpricing gets exposed almost immediately in today's market.

Use Arizona's Coming Soon advantage. Arizona allows homes to be marketed and shown for up to 30 days without accruing days on market. When used correctly, this lets you build demand, gather real buyer feedback, and launch with momentum — not desperation.

Concessions are strategy, not weakness. Offering a rate buydown or closing cost credit keeps your headline price intact, attracts a wider buyer pool, and keeps deals together at the inspection stage.

What's working

- Priced within 2–3% of comparable sold data from the past 90 days

- Professional staging and photography — non-negotiable in today's market

- Pre-marketing in Coming Soon status to build early momentum

- Proactive concession offer: a rate buydown beats a price reduction every time

Phoenix's economic diversification is the investment thesis that most national headlines miss. Semiconductor manufacturing, aerospace, healthcare, financial services, logistics, and higher education all anchor employment — creating a recession-resilient mix that supports long-term housing demand.

The lock-in effect creates a structural supply floor. With most existing homeowners carrying sub-4% mortgages, listings will remain constrained even as buyer demand fluctuates. That puts a floor under price pressure that benefits long-hold investors across cycles.

STR is the highest-ROI opportunity for qualified investors. When structured with cost segregation and bonus depreciation, the tax efficiency can rival or exceed cash-on-cash returns — particularly for high-income earners looking to reduce federal tax burden while building appreciating assets.

Long-term rental remains solid in the Chandler–Gilbert–Tempe–Mesa corridor where tech and healthcare worker demand has stayed elevated. Cap rates remain more attractive than comparable West Coast markets on a risk-adjusted basis.

Best plays in 2026

- STR-eligible properties in Scottsdale Old Town and resort corridors

- SFR long-term rentals in the Chandler / Gilbert tech employment corridor

- Outer-market acquisitions using builder concessions to lower your cost basis

- Monitor HOA and municipal STR regulation changes — they move fast in AZ

09 Looking Ahead to Summer

As temperatures continue climbing across the Valley, seasonality will begin playing a larger role in overall market activity. Summer tends to slow parts of the market as many sellers pull back, cancel listings, or wait until fall. That reduction in active listings can sometimes tighten supply enough to improve conditions in certain segments — particularly luxury markets.

Last summer, several areas tightened much more quickly than many expected once listing activity slowed. It would not be surprising to see parts of that pattern emerge again this year.

The Greater Phoenix market is still moving, still creating opportunities, and still attracting demand. But the easy market is gone. This has become a market that rewards preparation, positioning, and strategy — not just timing.

Written by

Eric Ravenscroft

Real Estate Advisor · Owner, The Ravenscroft Group · Elite Agent, Real Broker · License SA691304000

Eric Ravenscroft is a Top 1% real estate advisor across North America and the owner of The Ravenscroft Group at Real Broker. A former Director of Wealth Management, Eric brings a rare financial planning lens to every transaction — specializing in new construction, short-term rental investment, 1031 exchanges, and California-to-Arizona relocation strategy. He has closed more than $100 million in residential sales, helped clients build over $133 million in long-term wealth, and earned 150+ five-star reviews. Eric has been featured in the Wall Street Journal and is a preferred partner for USAA, Chase, SoFi, PennyMac, Citibank, and RBC.

Market statistics represent metro-wide averages as of May 27, 2026; individual submarket conditions vary. Mortgage rates are approximate and vary by lender, credit profile, and loan type. STR tax projections are illustrative estimates only — not tax, legal, or financial advice. Consult a qualified CPA before acting. Sources: ARMLS, Zillow, Rocket Mortgage, Curinos/Experian, Lofty. AZ License SA691304000.

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.