The Complete Guide to Saving on Taxes Through Real Estate (2026 Edition)

The Complete Guide to Saving on Taxes Through Real Estate

35+ legal strategies — from first-year deductions to advanced depreciation stacking, capital gains deferrals, entity structuring, and lifetime estate planning. The only resource you need.

"No other asset class in the United States offers as many simultaneous, legal tax-reduction strategies as real estate. It is the single most tax-advantaged investment vehicle available to ordinary Americans — and most investors are using only a fraction of what is available to them."

I've spent 15+ years at the intersection of real estate, financial planning, and tax strategy. That vantage point reveals one consistent pattern: most real estate owners are significantly overpaying the IRS every single year — not because they're doing anything wrong, but because they simply don't know the full arsenal of strategies available to them.

This guide is designed to change that. It covers every major legal strategy — clearly explained, with real examples — so you can have an informed conversation with your CPA, financial planner, and real estate advisor about which combination is right for your situation.

Whether you own one primary residence or a portfolio of commercial properties, whether you're a W-2 employee looking for relief or a full-time investor optimizing for generational wealth — there is something in this guide for you. Read it end to end, or jump to the section that fits your situation using the parts below.

These reduce your taxable income starting in year one — available to homeowners, landlords, and investors alike.

For primary and secondary residences, homeowners can deduct interest on mortgage debt up to $750,000 (loans after December 15, 2017; $1M for older loans). In the early years when interest dominates the payment, this is often the single largest deduction available to homeowners.

- Applies to primary home and one qualifying secondary/vacation home

- Deductible on Schedule A — requires itemizing over the standard deduction (see IRS Pub. 936)

- Points paid at origination may be deductible in the year paid

- Home equity loan interest deductible if proceeds used to buy, build, or improve the property

- Rental property mortgage interest: fully deductible on Schedule E with no dollar cap

The 2024 standard deduction is $14,600 (single) / $29,200 (married filing jointly). You only benefit from itemizing — and therefore from the mortgage interest deduction — if your total itemized deductions exceed the standard deduction. Many homeowners with larger mortgages or high property taxes still benefit significantly from itemizing.

State and Local Taxes (SALT) — including property taxes — are deductible up to $10,000 per year ($5,000 MFS) on primary/secondary residences. The cap frustrates high-tax state owners, but rental property taxes are a completely different story.

Rental property taxes are NOT subject to the $10,000 SALT cap. They are deducted as an ordinary business expense on Schedule E — fully and without limitation. A $22,000 property tax bill on a commercial rental deducts in full. This is one of the most underappreciated advantages of rental ownership.

Arizona note: Arizona's effective property tax rate averages approximately 0.60% — one of the lower rates nationally — making Phoenix Metro investments especially efficient from a tax standpoint.

Rental property owners can deduct virtually every ordinary and necessary expense of managing and maintaining their property. This is broad, powerful, and surprises many first-time landlords with its scope.

- Property management fees and leasing commissions

- Repairs and maintenance (improvements must be capitalized and depreciated — not expensed immediately)

- Insurance premiums — landlord policy, umbrella policy, flood insurance

- HOA dues and condominium assessments

- Utilities paid by the landlord (water, trash, common area electric)

- Legal and professional fees — attorney, CPA, title company fees for refinancing

- Advertising, tenant screening, and background check costs

- Travel expenses to and from the property for management purposes

- Mortgage interest on rental loans — fully deductible, no cap whatsoever

- Pest control, landscaping, and snow removal

- Lock changes, security systems, and smart home upgrades (if expensed)

A repair that maintains the property's current condition (fixing a leaky faucet, patching drywall) is immediately deductible. An improvement that adds value or extends useful life (new roof, kitchen remodel, HVAC system) must be capitalized and depreciated. Getting this wrong is a common and costly audit trigger.

If you manage real estate from a space in your home used regularly and exclusively for business, you may qualify. This applies to real estate investors managing their own portfolio, agents, and those who qualify as real estate professionals.

$5 per square foot, up to 300 sq ft ($1,500 max). Much less recordkeeping. Best for smaller offices.

% of home used × actual home expenses (mortgage interest, utilities, insurance, repairs, depreciation). Usually larger deduction — requires meticulous records.

Important: the space must be used exclusively for business — a desk in a guest room typically does not qualify. A dedicated room used solely for managing properties does.

When you purchase a rental property or form a real estate business entity, you can deduct up to $5,000 in startup costs and $5,000 in organizational costs in the first year, with the remainder amortized over 180 months. Qualifying costs include attorney fees for entity formation, CPA fees for initial tax setup, market research, and travel for property scouting.

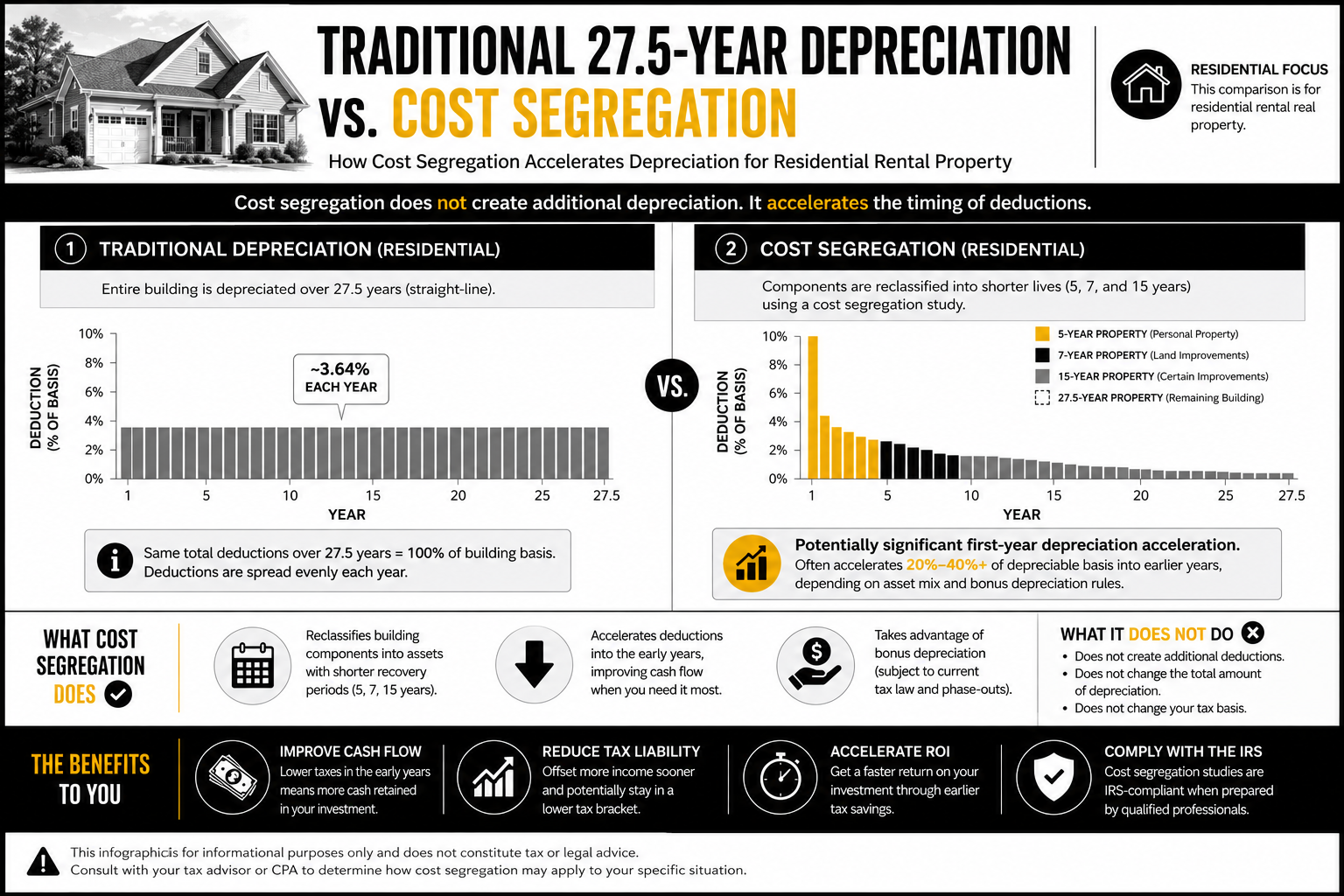

Depreciation lets you deduct the cost of a building over its useful life — generating paper losses that offset real income — even while the property appreciates in value.

"A property that earns $24,000 per year in rental income can show a $14,000 tax loss on paper — legally — through depreciation. That is the magic of real estate taxation."

Only the structure depreciates — not the land. (IRS Pub. 527 — Residential Rental Property.) On a $500,000 property with $100,000 attributed to land, the depreciable basis is $400,000, producing a consistent annual paper loss even in positive cash flow years.

| Property Type | Recovery Period | Annual Deduction on $400K Basis | 30-Year Total |

|---|---|---|---|

| Residential Rental | 27.5 years | ~$14,545/year | $436,364 |

| Commercial Real Estate | 39 years | ~$10,256/year | $307,692 |

A property appreciating at 5% per year simultaneously generates a tax loss on paper — one of the most unique advantages real estate offers over every other major asset class. Stocks, bonds, and cash produce no equivalent deduction.

When you sell a depreciated property, the IRS recaptures those deductions at a maximum 25% rate (unrecaptured Section 1250 gain) — separate from regular capital gains. The primary defenses are the 1031 exchange (defer recapture indefinitely) or the stepped-up basis at death (eliminate it entirely). Never take depreciation without a plan for the eventual recapture.

A cost segregation study is an engineering analysis that reclassifies building components into shorter depreciation categories — generating massive front-loaded deductions instead of spreading them over 27.5 or 39 years.

- 5–7 year property: appliances, carpeting, vinyl flooring, specialty lighting, decorative millwork, countertops, cabinets in common areas

- 15-year property: landscaping, parking lots, sidewalks, fencing, exterior lighting, site utilities, retaining walls

- 27.5 / 39 year: the remaining structural shell — foundation, framing, roof structure, load-bearing walls

On a $1,000,000 commercial building, a cost seg study typically identifies $250,000–$400,000 in accelerated components — compressing decades of deductions into the first few years.

Ideal candidates: (1) purchased or built property for $500,000+, (2) in the 32%+ tax bracket, (3) can absorb passive losses or qualify as a real estate professional, (4) plan to hold for at least 3–5 years. Study costs of $5,000–$15,000 are themselves deductible and typically pay for themselves 5–10x in the first year alone.

Phoenix Apartment Complex — Cost Segregation in Action

A client purchased a 12-unit apartment complex in Scottsdale, Arizona for $1.8M ($1.4M depreciable basis after land allocation). Standard depreciation would have generated ~$50,900 per year over 27.5 years. After a cost segregation study identifying $380,000 in 5–15 year components and applying bonus depreciation, the client generated $412,000 in deductions in year one — offsetting significant other income.

Bonus depreciation allows investors to deduct a large percentage of qualifying property in the very first year it's placed in service. When stacked with a cost segregation study, the 5 and 15-year components are immediately eligible for bonus depreciation.

| Tax Year | Bonus Depreciation % | Status |

|---|---|---|

| 2017–2022 | 100% | TCJA original |

| 2023 | 80% | Phase-down began |

| 2024 | 60% | Phase-down continued |

| Jan 1–19, 2025 | 40% | Final phase-down days |

| Jan 19, 2025 onward | 100% | OBBBA — permanently restored |

| 2026 and beyond | 100% | Permanent — no sunset |

The phase-down is history. Under the OBBBA, 100% bonus depreciation is permanent with no scheduled expiration — meaning every qualifying acquisition in 2026 and beyond captures the full first-year deduction. There is no longer any urgency driven by a sunset date; the certainty alone transforms long-term acquisition planning.

On a $2M apartment building, a cost segregation study identifying 30% in qualifying 5–15 year components produces $600,000 in bonus-eligible assets — fully deductible in year one at 100%. For an investor in the 35% bracket, that is $210,000 in immediate tax savings on a single acquisition. This is why 2026 is one of the most powerful acquisition years in recent history for real estate investors with the right strategy in place.

Section 179 lets business owners deduct the full purchase price of qualifying property in the year of purchase — up to the annual limit ($1,220,000 for 2024). For real estate, this primarily applies to personal property in a rental business: HVAC systems, security systems, energy-efficient equipment, and for nonresidential property, qualified improvement property including roofing, HVAC, fire protection, and alarm systems.

Key distinction from bonus depreciation: Section 179 cannot create a loss — it's limited to business taxable income. It's best when you have rental income to absorb. Also note: Section 179 is not available for property used in residential rental activities under certain conditions — confirm eligibility with your CPA.

Several costs associated with acquiring or financing rental property are not immediately deductible but are amortized over their useful life:

- Loan origination fees / points on rental loans: amortized over the life of the loan (not immediately deductible like points on a primary residence)

- Title insurance and closing costs: added to basis (not deducted), then depreciated over the property's life

- Above-market leases acquired: amortized over the remaining lease term

- Customer lists and non-compete agreements in business property acquisitions: amortized over 15 years under IRC §197

Tracking these carefully from day one ensures you capture every dollar of basis that can be depreciated or amortized over the holding period.

Selling real estate triggers capital gains taxes — but the tax code provides powerful tools to defer, reduce, or completely eliminate them.

Live in your home as your primary residence for at least 2 of the last 5 years and you can exclude capital gains from federal tax: $250,000 if filing single, or $500,000 if married filing jointly. (IRS Topic 701.) This exclusion can be used repeatedly — generally once every two years.

| Scenario | Purchase Price | Sale Price | Gain | Tax Owed |

|---|---|---|---|---|

| Single owner, qualifies | $300,000 | $620,000 | $320,000 | $17,500 (on $70K excess) |

| Married, qualifies | $300,000 | $750,000 | $450,000 | $0 (under $500K) |

| Married, does not qualify | $300,000 | $750,000 | $450,000 | ~$67,500–$107,100 |

Purchase a fixer-upper, move in, renovate while living there for 2+ years, sell and exclude up to $500,000 in gains. Done systematically every 2–3 years, this strategy can generate well over $1 million in tax-free wealth over a decade. Requires documentation of primary residence, and improvements must be tracked for basis — but no other tax strategy generates tax-free returns this reliably.

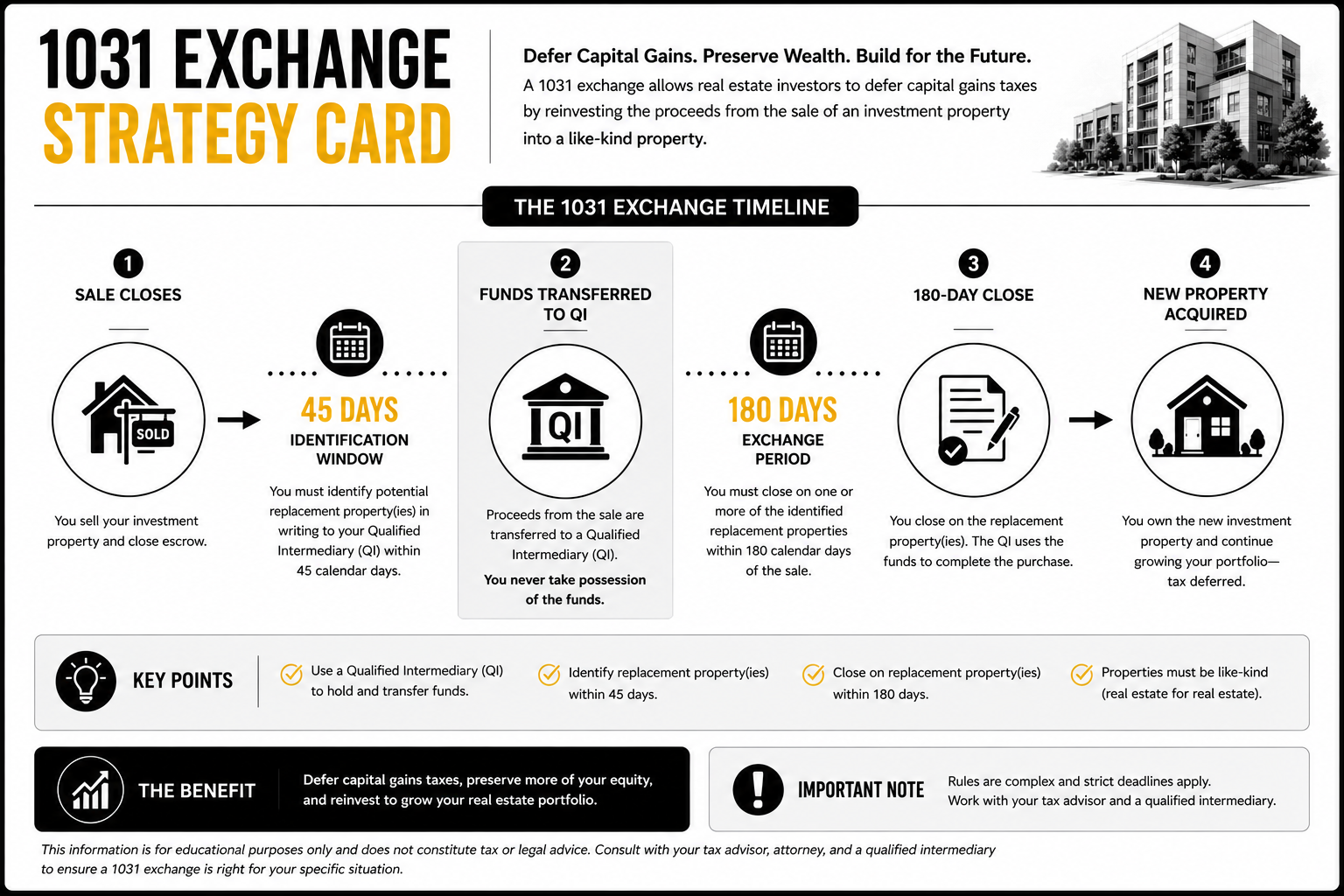

Section 1031 is the most powerful wealth-building tool in the entire real estate tax code. (IRS Like-Kind Exchange guidance.) It allows investors to defer capital gains taxes — and depreciation recapture — indefinitely by reinvesting proceeds into a like-kind replacement property.

The 1031 exchange timeline: 45 days to identify, 180 days to close — both run from the sale date of the relinquished property.

Identify replacement property(ies) within 45 days of the sale closing. Can identify up to 3 properties without restriction (3-property rule) or more under specific rules.

Exchange must close within 180 days of the relinquished property sale. No extensions, no exceptions.

Must use a QI to hold proceeds — you cannot touch the money at any point. Contact with funds disqualifies the entire exchange.

Replacement must be of equal or greater value. Any cash received ("boot") is taxable in the year of exchange.

Investor A sells a $500,000 property with $200,000 in gains, pays tax ($40,000+), reinvests $460,000. Investor B executes a 1031 exchange and reinvests the full $500,000. Over 20 years and multiple exchanges, Investor B's tax-deferred compounding creates a wealth gap of hundreds of thousands of dollars — all legal, all deferred. At death, heirs inherit at stepped-up basis and the deferred taxes vanish entirely.

Chandler Duplex → Mesa Commercial Strip Center

A client sold a Chandler duplex purchased for $185,000 in 2014 for $520,000 in 2024. Gain: $335,000 (including $42,000 in prior depreciation subject to recapture). Instead of paying approximately $85,000 in combined capital gains and recapture tax, the client executed a 1031 exchange into a small commercial strip center in Mesa. The $85,000 that would have gone to the IRS stayed in the investment — continuing to generate rental income and appreciation.

When you leave appreciated real estate to heirs, the cost basis is automatically "stepped up" to the fair market value at the date of death — eliminating all capital gains accrued during your lifetime, including decades of deferred 1031 gains and accumulated depreciation recapture.

This is not a loophole — it is the law as designed, and it is the ultimate endpoint of a lifetime 1031 exchange strategy. For investors who have held properties for decades, this single provision can eliminate millions in deferred tax liability.

Gifting appreciated property during life does NOT trigger a step-up. The recipient takes your original cost basis. Only transfers at death receive the stepped-up basis. This distinction drives many estate planning decisions around when and how to transfer real estate to heirs.

QOZs offer three tiers of capital gains benefits for investors who reinvest gains into designated low-income communities within 180 days. The gains don't have to come from real estate — they can come from stock sales, business sales, or any capital asset.

- Tier 1 — Deferral: Original gains deferred until the QOZ investment is sold (or Dec. 31, 2026 under current law — confirm with CPA)

- Tier 2 — Step-up: Basis step-up on the QOZ fund investment after holding periods

- Tier 3 — Permanent Exclusion: 100% of appreciation on the QOZ investment excluded from tax if held 10+ years

Best for investors with large, recent capital gains events who believe in the underlying investment location and can commit to a 10+ year hold.

Rather than receiving all proceeds at closing — and paying tax on the entire gain in one year — an installment sale spreads payments and tax recognition over multiple years. This can keep annual recognized gains below key rate thresholds (0%, 15%, 20%) and defer meaningful tax dollars.

- Each payment received consists of a principal return, interest, and gain recognition in proportion to the gross profit percentage

- Interest charged must meet the IRS applicable federal rate (AFR) to avoid imputed interest issues

- Does not defer depreciation recapture — recapture is recognized in full in year one regardless

- Works well for seller-financed commercial real estate, vacant land, and business property sales

Long-term capital gains rates (property held 12+ months) are 0%, 15%, or 20% depending on taxable income. Strategic timing of a property sale can drop your recognized gain into a lower bracket — or even the 0% bracket for qualifying lower-income years.

| 2024 Taxable Income (MFJ) | Long-Term Capital Gains Rate |

|---|---|

| Up to $94,050 | 0% |

| $94,051 – $583,750 | 15% |

| Over $583,750 | 20% |

Additionally, high-income earners may owe the 3.8% Net Investment Income Tax (NIIT — IRS Topic 409) on gains if MAGI exceeds $250,000 (MFJ). Real estate professionals may avoid NIIT on rental income; consult a CPA for specifics.

The strategy that separates serious investors from casual landlords — and can unlock six-figure annual tax savings for high-income households.

Real Estate Professional Status allows qualifying taxpayers to deduct unlimited passive real estate losses against any income (IRS Pub. 925) — W-2 wages, business income, investment income — with no dollar limitation whatsoever. Both IRS tests must be met:

- Test 1: More than 750 hours per year in real property trades or businesses in which you materially participate

- Test 2: More than half of ALL personal services during the year must be in real property activities

For a married couple filing jointly where one spouse qualifies as REPS, all rental losses from materially participated activities become fully deductible against the household's total income — including the other spouse's high W-2 earnings.

The IRS actively scrutinizes REPS claims, particularly from households with high W-2 income. You must maintain contemporaneous time logs documenting every hour spent on qualifying real property activities — date, hours, specific activity. Retroactively reconstructed logs do not hold up in audit. Keep your logs current, weekly.

Phoenix Physician Household — REPS + Cost Segregation

A physician couple in Scottsdale — one spouse earning $480,000 W-2, the other managing their 4-property rental portfolio full time. The managing spouse qualified as a REPS (820+ hours annually, well-documented). They acquired a fifth property — a $950,000 duplex — and commissioned a cost segregation study identifying $215,000 in accelerated components. Combined with prior depreciation, they generated $287,000 in deductible losses in a single tax year, fully offsetting a large portion of the physician's W-2 income.

Without REPS, passive real estate losses can only offset passive income under general passive activity rules (IRC §469). However, there are meaningful exceptions that still benefit many investors:

- $25,000 active participation allowance: If your MAGI is under $100,000 and you actively participate (make management decisions), you can deduct up to $25,000 of rental losses against ordinary income. Phases out ratably between $100,000–$150,000 MAGI.

- Passive loss carry-forward: All unused passive losses are suspended and carried forward. They are fully released in the year you dispose of the property in a fully taxable transaction — or when you generate sufficient passive income.

- Grouping election: Multiple properties or activities can be grouped as a single activity under Reg. §1.469-4, making it easier to meet material participation tests across a portfolio.

- Self-rental rule: If you rent property to a business you own, the rental income may be treated as non-passive — consult a CPA on this nuanced area.

Every dollar of suspended passive losses accumulated over years of ownership is released in the year you sell the property. This is why many long-term rental property owners have a significant built-up passive loss "bank" that dramatically reduces or eliminates their tax on the eventual sale. Track these carefully — they are a valuable asset.

STRs occupy a uniquely powerful position in the tax code — with the right structure, they can generate active losses that offset W-2 income for high earners who cannot meet REPS requirements.

Properties rented with an average stay of 7 days or fewer are not classified as rental activities under the passive activity rules — they are treated as active businesses under IRC §469(c)(7). If you materially participate, losses are non-passive and directly offset W-2 or other active income.

This classification happens by statute — it applies automatically to any rental with an average period of customer use of 7 days or less, regardless of services provided. Combined with cost segregation and bonus depreciation, a single STR property can generate six figures in first-year deductions.

You must: (1) have an average rental period of 7 days or fewer (this is the average across all rentals — not any individual stay), AND (2) materially participate in the activity — generally 500+ hours per year of personal services, or meeting one of the other 7 IRS material participation tests. Hiring a full-service property manager may jeopardize material participation. Structure this before you buy.

The IRS has significantly increased audits of high-income earners claiming STR losses against W-2 income in recent years. Common vulnerabilities: insufficient activity logs, relying on a property manager for most tasks, short activity periods (a property bought in October claiming a full year's participation). Documentation standards here are as rigorous as REPS claims.

For properties used both personally and as a rental, the tax treatment hinges entirely on personal use days vs. rental days:

| Scenario | Classification | Tax Treatment |

|---|---|---|

| Rented fewer than 15 days/year | Personal residence | Rental income completely tax-free. No reporting required. No deductions either. |

| Personal use > 14 days AND > 10% of rental days | Personal/vacation home | Rental income taxable; deductions limited proportionally and cannot create a loss |

| Personal use ≤ 14 days AND ≤ 10% of rental days | Rental property | All expenses deductible proportionally; losses subject to passive activity rules |

If you rent your primary or vacation home for fewer than 15 days in a tax year — for example, during a major local event like a Super Bowl or spring training — the rental income is completely tax-free and doesn't even need to be reported. The Augusta Rule, as it's informally known, is one of the few legal ways to receive tax-free rental income. Business owners can also rent their home to their own business for meetings, further expanding the strategy.

The tax classification of a rental property depends not just on average stay length (7-day STR test) but also on the services provided. Understanding these classifications allows investors to strategically position their property for the most favorable tax treatment:

- Average stay ≤ 7 days: Treated like a hotel — active business, not passive rental. Losses can offset active income if you materially participate.

- Average stay 8–30 days with significant personal services: Also treated as active business (like a B&B). Similar treatment to the 7-day rule.

- Average stay 8–30 days, no significant services: Passive rental activity — subject to standard passive activity loss rules.

- Average stay > 30 days: Standard long-term rental — passive activity, Schedule E treatment.

- Medium-term rentals (30–90 days, furnished): Can qualify under the 30-day rule — useful for travel nurses, corporate housing, and executive rentals in markets like Phoenix, Scottsdale, and Tempe.

How you hold real estate significantly impacts your tax outcome, liability protection, and estate planning flexibility. Structure matters as much as strategy.

| Entity | Tax Treatment | Liability Protection | Best For |

|---|---|---|---|

| Sole Proprietorship / Direct Ownership | Schedule E or C | None | Single property, minimal risk, simplicity |

| LLC (single-member) | Disregarded entity; Schedule E or C | Strong | Solo investors — most common structure |

| LLC (multi-member) | Partnership; K-1 pass-through | Strong | Partners, spouses, joint ventures |

| S-Corporation | Pass-through; split salary/distribution | Strong | Reducing self-employment tax on active income |

| C-Corporation | Double taxation; 21% corporate rate | Strong | Rarely optimal for rental real estate |

| Land Trust | Privacy vehicle; pass-through to beneficiary | Moderate (privacy) | Privacy-focused investors, estate planning |

| Series LLC | Each series taxed separately | Strong (series isolation) | Multi-property portfolios — available in AZ and many states |

Arizona adopted Series LLC legislation, making it an excellent vehicle for Phoenix Metro investors with multiple properties. Each series can own a separate property with liability insulated from other series — providing asset protection similar to multiple LLCs at a fraction of the cost. Tax treatment flows through to the owner's return. Confirm current Arizona law with your attorney.

The QBI deduction allows eligible pass-through business owners to deduct up to 20% of qualified business income from federal taxable income. Real estate investors may qualify if their rental activity rises to the level of a trade or business — a facts-and-circumstances determination.

- Safe harbor: 250+ hours of rental services per year with contemporaneous records qualifies the activity as a trade or business for QBI purposes

- Applies to income from LLCs, S-corps, partnerships, and sole proprietorships

- Subject to W-2 wage and capital limitations for higher earners (generally above ~$383,900 MFJ for 2024)

- STR owners who qualify under the active business classification may automatically satisfy the trade or business test

Example: Investor netting $120,000 in qualified rental income could deduct $24,000 — saving $7,200–$10,800 in federal taxes depending on bracket. This deduction is frequently overlooked by rental property owners who are not aware they qualify.

If you buy and sell properties frequently, the IRS may classify you as a dealer rather than an investor. The tax difference is dramatic:

| Classification | Tax Rate on Profits | 1031 Exchange | Cap Gains Rates | Self-Employment Tax |

|---|---|---|---|---|

| Investor | 0%–20% long-term cap gains | Eligible | Yes | No |

| Dealer | Up to 37% ordinary income | Not eligible | No | Up to 15.3% |

Factors the IRS considers: frequency of sales, intent at purchase, holding period, improvements made, and whether this is your primary occupation. If you both flip and hold properties, separate entities for each activity is critical — flipping operations in one LLC, long-term investments in another — to protect investor status on held properties.

Real estate agents, brokers, and other self-employed professionals in real estate pay up to 15.3% in self-employment (SE) tax on net earnings — on top of income tax. Several strategies reduce this burden:

- S-Corporation election: Split income between reasonable salary (subject to FICA) and S-corp distributions (not subject to SE tax). A real estate agent earning $200,000 might pay themselves a $90,000 salary and take $110,000 as distributions — saving ~$16,830 in SE tax annually.

- SEP-IRA contributions: Contribute up to 25% of net self-employment earnings (max $69,000 for 2024) — fully deductible, reducing SE income and income tax simultaneously.

- Solo 401(k): Up to $69,000 in contributions for 2024 ($76,500 age 50+) — the most powerful retirement savings vehicle available to self-employed individuals.

- Health insurance premiums: Fully deductible above-the-line for self-employed individuals who are not eligible for employer coverage.

- Business deductions: Vehicle (actual expenses or standard mileage), tech/software, continuing education, professional memberships, marketing, home office.

The 3.8% Net Investment Income Tax (IRC §1411) applies to the lesser of net investment income or the amount by which MAGI exceeds $250,000 (MFJ) / $200,000 (single). For real estate investors, this can significantly increase the tax cost of rental income and capital gains.

- Subject to NIIT: Passive rental income, capital gains on investment property sales (including 1031 boot), interest, dividends

- Exempt from NIIT: Active trade or business income — including rental income from activities qualifying as a trade or business under REPS or the STR active classification

Qualifying as a real estate professional not only eliminates passive activity loss limitations — it may also exempt your rental income from the 3.8% NIIT surcharge, creating a dual benefit for high-income investors.

The most powerful real estate tax strategies work across generations — combining deferral during life with elimination at death.

"The most sophisticated investors don't just avoid tax today — they architect a lifetime strategy where the deferred taxes never come due. Real estate makes this possible in ways no other asset class does."

This is the crown jewel combination in real estate tax planning. Execute 1031 exchanges throughout your lifetime — continuously deferring capital gains and depreciation recapture as you trade up into larger properties. At death, your heirs inherit at fair market value. All deferred gains and accumulated recapture disappear. Permanently.

| Sell and Pay Tax | 1031 Exchange Strategy | |

|---|---|---|

| Gain recognized over lifetime | $800,000 | $0 (deferred) |

| Estimated federal tax paid | $160,000–$184,000 | $0 |

| Capital at work | $616,000–$640,000 | $800,000 |

| Gains taxable to heirs | N/A | $0 (stepped-up basis) |

Arizona has no separate state estate tax, meaning Arizona investors do not face a dual federal/state estate tax burden that many other states impose. Combined with the federal stepped-up basis rule and no Arizona capital gains preference rate (gains taxed at the same flat 2.5% as ordinary income), the 1031 + step-up strategy is particularly powerful for Arizona investors compared to residents of California, New York, or Oregon.

A DST allows investors to complete a 1031 exchange into fractional ownership of institutional-quality real estate — multifamily communities, industrial parks, net-lease commercial properties, medical office buildings. DSTs qualify as like-kind property for 1031 purposes under Revenue Ruling 2004-86.

- Exit active management while deferring all capital gains taxes and recapture

- Diversify across property types and geographies through a single exchange

- Satisfy strict 1031 timelines when a direct replacement isn't closing in time

- Receive passive income without landlord responsibilities

- Transition to retirement-friendly passive income structure

DST investments are typically $100,000 minimum and are restricted to accredited investors. Due diligence on the sponsor, property quality, and financing structure is essential — not all DSTs are equal.

A CRT allows you to donate appreciated real estate to a trust, which sells the property without paying immediate capital gains tax, then pays you income for life (or a term of years), with the remainder passing to charity at the end.

- Avoid immediate capital gains tax on sale of highly appreciated property

- Receive a lifetime income stream (typically 5–8% of initial trust value annually)

- Receive a partial charitable income tax deduction in the year of transfer

- Remove the asset from your taxable estate — reducing estate tax exposure

- Support a charitable cause or establish a named fund at a community foundation

Best for investors aged 60+ with highly appreciated property, charitable intent, and income needs in retirement. The income received from the trust is taxable — the CRT does not eliminate tax, it defers and converts it to a more manageable income stream.

FLPs and family LLCs allow investors to transfer real estate to family members at a valuation discount (due to lack of marketability and minority interest discounts of 15–40%) while retaining operational control as general partner or managing member.

- Estate tax reduction: Transfer interests at a discount, moving more value out of the taxable estate per annual exclusion gift ($18,000/recipient/year for 2024) or lifetime exemption dollar

- Asset protection: Outside creditors generally cannot seize a charging order interest — they receive distributions if and when made, providing significant protection

- Income splitting: Shift income to family members in lower tax brackets (subject to kiddie tax rules for minors)

- Centralized management: Keep family properties together under unified management while gradually transferring economic interests to heirs

The IRS aggressively challenges FLPs that lack economic substance — where the primary purpose is tax avoidance without meaningful business activity. The FLP must have a legitimate non-tax business purpose, maintain proper formalities, and the general partner must not retain too much control over distributions. Work with a qualified estate planning attorney.

Sophisticated estate planning for real estate investors often involves irrevocable trusts that remove property from the taxable estate while preserving various benefits:

- Intentionally Defective Grantor Trust (IDGT): Sell property to the trust in exchange for an installment note — removes appreciation from estate while grantor continues paying income tax on trust income (tax-free gift to beneficiaries). Ideal for properties expected to appreciate significantly.

- Qualified Personal Residence Trust (QPRT): Transfer your home to the trust and retain the right to live in it for a term of years, at a reduced gift tax value. At end of term, property passes to heirs with estate tax savings.

- Spousal Lifetime Access Trust (SLAT): Irrevocable trust for spouse's benefit that removes assets from estate. Particularly relevant with the current elevated federal estate tax exemption ($13.61M per person for 2024) scheduled to sunset after 2025.

The 2025 sunset of the doubled estate tax exemption makes 2026 planning critical — consult an estate planning attorney immediately if your combined estate exceeds $7M.

Beyond the immediate tax benefits, QOZ investments can serve as estate planning vehicles. If held for 10+ years, the entire appreciation in the QOZ fund is excluded from capital gains tax — making the investment highly efficient for heirs. Additionally, QOZ fund interests can be gifted using standard techniques, potentially transferring the 10-year appreciation exclusion to family members.

Combine the tax advantages of retirement accounts with real estate investing for compounding benefits on two fronts simultaneously.

A self-directed IRA allows you to invest retirement funds directly in real estate — rental properties, mortgage notes, tax liens, commercial property, and more. Income grows tax-deferred (traditional) or tax-free (Roth). The rules are strict and must be followed precisely to avoid disqualifying the account.

- Cannot personally use or benefit from the property — no living in it, managing it directly, or performing repair work yourself

- Prohibited transactions with disqualified persons (yourself, spouse, lineal family members, your fiduciaries) can trigger immediate taxation of the entire IRA

- All property expenses must be paid from the IRA; all income must flow back to the IRA

- Unrelated Business Taxable Income (UBTI) may apply when the IRA uses leverage (debt-financed property) — triggering tax inside the IRA

A Roth SDIRA grows completely tax-free — including all rental income and capital gains. A $100,000 property purchase in a Roth SDIRA that appreciates to $400,000 over 15 years generates $300,000 in completely tax-free profit, with no capital gains, no depreciation recapture, and no required minimum distributions. The Roth SDIRA is the most powerful long-term real estate investment vehicle for investors who can fund it.

The Solo 401(k) (also called Individual 401(k) or Self-Employed 401(k)) is available to self-employed individuals with no full-time employees other than a spouse. It offers the highest contribution limits of any retirement account and greater flexibility for real estate investing than a traditional IRA.

| Contribution Type | 2024 Limit |

|---|---|

| Employee elective deferral | $23,000 ($30,500 age 50+) |

| Employer profit-sharing contribution | Up to 25% of compensation |

| Combined maximum | $69,000 ($76,500 age 50+) |

- Checkbook control: With a Solo 401(k) that includes checkbook control, you can invest directly in real estate quickly — no custodian approval required for each transaction

- Leverage without UBTI: Unlike SDIRAs, Solo 401(k)s can generally use leverage (mortgage) to purchase real estate without triggering UBTI — a major advantage for leveraged investments

- Loan provision: Borrow up to $50,000 or 50% of account balance (whichever is less) from your Solo 401(k) — can be used for investment down payments

For high-income self-employed real estate professionals, defined benefit and cash balance plans can allow contributions far exceeding the Solo 401(k) limit — in some cases $200,000+ per year — fully tax-deductible.

A cash balance plan combined with a Solo 401(k) can dramatically reduce a high earner's taxable income. Real estate professionals earning $400,000–$800,000 annually are prime candidates. These plans require actuarial design and have higher administration costs, but the tax savings typically dwarf those costs many times over.

Knowing what not to do is as important as knowing the strategies themselves. These are the errors that cost investors the most — often without realizing it until it's too late.

Your adjusted cost basis — purchase price plus improvements minus depreciation taken — determines your taxable gain when you sell. Investors who fail to track improvements, capitalized costs, and depreciation accurately often overpay capital gains tax because they can't prove their basis. Start a dedicated records file the day you close on every property.

A kitchen remodel is not a "repair" — it must be capitalized and depreciated. Improperly expensing capital improvements is a common audit trigger. The flip side: failing to capitalize improvements means missing the depreciation deduction on those costs over the property's life. Both errors cost money.

The 1031 exchange deadlines are absolute. Missing the 45-day identification window or the 180-day closing window makes the entire transaction taxable — with no exceptions for illness, natural disasters (unless a federal disaster declaration), or paperwork delays. Start identifying replacement properties before you sell, not after.

The IRS does not accept reconstructed time records created after the fact. REPS and STR active loss claims require contemporaneous records — maintained throughout the year. Many investors who legitimately qualify for these strategies lose their deductions in audit because they cannot document the hours. Keep a real-time log.

Every dollar of depreciation you've taken — even depreciation you didn't know you were taking — will be recaptured at 25% when you sell. Investors who sell without a 1031 exchange plan are often shocked by their tax bill. Run the numbers before you list the property, not after you accept an offer.

One lawsuit against one property can expose every other property in the same LLC. Separate high-risk properties into separate entities. The cost of maintaining multiple LLCs — typically $50–$200/year each in Arizona — is trivial compared to the asset protection benefit.

The Section 199A QBI deduction can reduce taxable income on rental profits by 20% — but only if your rental activity qualifies as a trade or business. Many real estate investors who qualify never claim it because they or their CPA aren't aware the rental safe harbor applies. Review your eligibility annually.

A general-practice CPA who files simple returns will not proactively identify cost segregation opportunities, recommend grouping elections, or know the STR classification rules. Real estate tax strategy is a specialized discipline. Working with a CPA who focuses on real estate investors typically pays for itself in tax savings within the first engagement.

Investors in the Greater Phoenix Metro and across Arizona benefit from several state-level advantages that make the federal strategies above even more powerful.

- No separate state capital gains tax rate: Arizona taxes capital gains as ordinary income at the flat state rate — currently 2.5% (reduced from 4.5% in recent years). No preferential federal rate differential at the state level, making federal 1031 deferral and exclusion strategies even more valuable.

- No state estate tax: Arizona repealed its estate tax. Arizona residents face only the federal estate tax — and only on estates exceeding the federal exemption ($13.61M per person for 2024, though scheduled to change after 2025).

- Low effective property tax rate: Arizona's effective property tax rate averages approximately 0.60% — well below the national average of 1.07%. Lower carrying costs improve cash-on-cash returns and make depreciation deductions go further relative to cash outlay.

- Favorable LLC laws: Arizona Series LLC is available, and Arizona LLC charging order protection is strong, making the state attractive for holding real estate in business entities.

- No city income tax in Phoenix Metro: Unlike some states where cities impose additional income taxes, Arizona has no local city income tax — keeping the overall tax burden lower for investors and tenants.

- Arizona's rental tax (TPT): Arizona imposes a Transaction Privilege Tax (TPT) on residential rental income — currently 2.0% at the state level plus city rates. This is a tax on the activity of renting, not income. Ensure proper registration and filing. Short-term rentals have additional registration requirements in most Arizona cities.

The Phoenix Metro area — including Scottsdale, Chandler, Tempe, Gilbert, Mesa, Glendale, Peoria, and Surprise — is one of the fastest-appreciating real estate markets in the country over the past decade. The combination of strong appreciation, low property taxes, and no state estate tax makes the 1031 exchange + stepped-up basis lifetime strategy particularly impactful for Phoenix Metro investors. Properties purchased in 2010–2015 have in many cases tripled in value — making capital gains planning urgent for any investor considering a sale.

A quick reference for the technical terms used throughout this guide.

Quick Reference by Investor Profile

Find your situation — these are the strategies to prioritize first.

Homeowner

- Mortgage interest deduction (Sec. 163)

- SALT property tax (up to $10K)

- Section 121 exclusion (up to $500K)

- Home office deduction

- Live-in flip strategy

First Rental Property

- Schedule E operating expense deductions

- Straight-line depreciation (27.5 yrs)

- $25K passive loss allowance

- Entity structure review (LLC)

- QBI deduction (Sec. 199A)

High-Income W-2 Earner

- Real estate professional status (REPS)

- Short-term rental active loss strategy

- Cost segregation + bonus depreciation

- Material participation planning

- NIIT avoidance through REPS

Growing Portfolio

- 1031 like-kind exchanges

- Cost segregation on each acquisition

- Multi-entity structuring (Series LLC)

- QBI deduction optimization

- Passive loss grouping election

Preparing to Sell

- 1031 exchange — plan before listing

- Installment sale structuring

- Opportunity zone reinvestment

- 1031 into DST (passive transition)

- Capital gains bracket timing

Estate Planning Focus

- 1031 + stepped-up basis lifetime strategy

- Delaware Statutory Trust (DST)

- Charitable remainder trust (CRT)

- Family limited partnership / LLC

- IDGT / QPRT / SLAT structures

Fix-and-Flip Investor

- Separate entity for flip vs. hold

- Dealer vs. investor status planning

- S-corp for SE tax reduction

- Solo 401(k) contributions

- Business expense deductions

STR / Airbnb Owner

- 7-day average stay active loss test

- Material participation documentation

- Cost segregation + bonus depreciation

- Augusta Rule (under-15-day rental)

- Arizona TPT registration

Self-Employed Agent / Broker

- S-corp election for SE tax reduction

- Solo 401(k) or defined benefit plan

- Home office deduction

- Vehicle and business expense deductions

- Health insurance premium deduction

Frequently Asked Questions

Eric Ravenscroft has spent over 15 years at the rare intersection of real estate, financial planning, and tax strategy — giving his clients a genuinely integrated perspective that the vast majority of real estate professionals simply cannot offer.

Unlike advisors who specialize in a single discipline, Eric understands how every investment decision ripples through a client's complete financial picture: tax liability today, retirement plan tomorrow, and estate strategy for the generation that follows. He doesn't just help people buy and sell properties — he helps them build portfolios that work intelligently within their broader financial lives.

Eric's work has been featured in the Wall Street Journal, MarketWatch, MSN, and Morningstar. He serves clients throughout the Greater Phoenix Metro area — Scottsdale, Chandler, Tempe, Gilbert, Mesa, Glendale, Peoria, and Surprise — and across North America.

The tax strategies in this guide are implemented in close collaboration with Eric's network of CPAs and tax attorneys who specialise in real estate investors.

Ready to build a tax strategy that actually changes your numbers? Schedule a consultation with Eric — no obligation, no generic advice. Just a focused conversation about your specific situation.

Ready to Build a Strategy That Actually Reduces Your Taxes?

35+ strategies. One conversation. Eric will identify which combination applies to your situation — and exactly how to implement it with your CPA.

Schedule Your Free ConsultationGreater Phoenix Metro · Serving Investors Across North America · Last reviewed May 19, 2026

Categories

- All Blogs (306)

- Active Adult & 55 Plus Communities (14)

- Arizona Relocation Guides (21)

- Buyers (198)

- Financial Planning (55)

- General Real Estate (129)

- Income From Real Estate (54)

- Market Update (24)

- New Construction (27)

- News, Updates and Coming Soon (56)

- Real Estate Agent Financial Planning (21)

- Real Estate Investing (85)

- Sellers (103)

- Vacation and Short Term Rentals (41)

Recent Posts

About the Author

Eric Ravenscroft is a Top 1% REALTOR® across North America and one of Arizona’s most trusted real estate strategists. With 15 years of experience spanning real estate, wealth management, and investment planning, he helps clients make smarter, financially grounded decisions, from new construction and relocations to STR investments, 1031 exchanges, and long-term portfolio strategy.

Eric’s expertise has earned him industry recognition, Elite status with Real Broker, and features in major publications including the Wall Street Journal, MarketWatch, MSN, and Morningstar. Clients across the Greater Phoenix Metro rely on his clarity, strategic insight, and results-driven guidance.

Ready to make a confident real estate move? Call or text Eric today.