Arizona Real Estate Insights

From Someone Who Thinks

Like a Financial Advisor

Market analysis, tax strategy, investment guides, client case studies, and community deep-dives — written personally by Eric Ravenscroft, CRS. Not a marketing team. Not AI.

Updates

City-by-city breakdowns of the Greater Phoenix Metro — buyer's, seller's, and balanced markets analyzed.

& Wealth Building

Bonus depreciation, cost segregation, 1031 exchanges, STR tax loopholes — the strategies most agents never discuss.

Guides

Builder incentives, community launches, lot analysis, and negotiation strategy across the Valley.

Case Studies

Real transactions, real numbers, and the strategy behind each result — from record sales to STR acquisitions.

Guides

Moving from California, Texas, or out of state? Everything you need to know before you arrive.

Resources

PCS guides, BAH strategy, VA loan comparisons, and the best neighborhoods near Luke AFB.

All Publications &

Commentary

Phoenix Real Estate Advisor | New Construction, Relocation & Investment Property Strategy

Recently, I was named among the Top 100 real estate professionals in the Greater Phoenix Metro. Recognition like that is meaningful — but it also prompted reflection. Awards are the outcome.Strategy is the cause. In today’s market, nearly every Phoenix real estate agent claims to be “top-ranked.” Ti

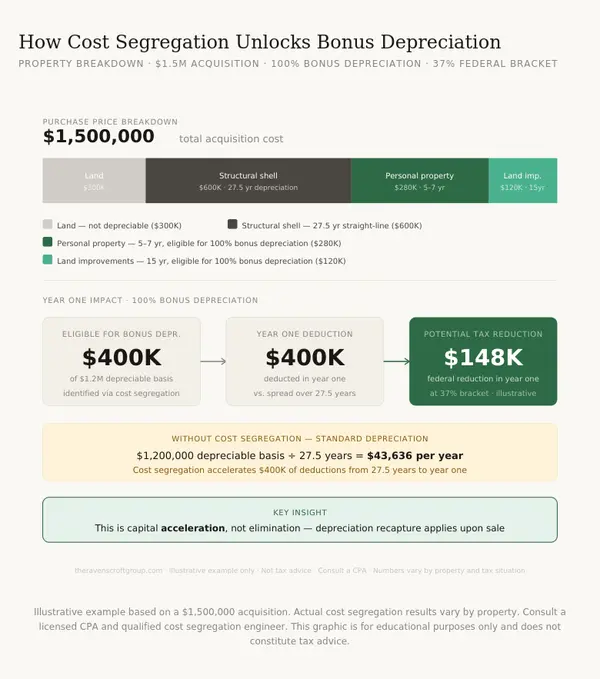

Goodyear, Arizona Basement & Casita STR Case Study: A Tax-Efficient Bonus Depreciation Strategy in Palm Valley

A Bonus Depreciation Strategy Built Around Rarity, Flexibility & Exit Protection Over the last several years, I’ve become increasingly selective when helping clients acquire short-term rental properties. Not because the opportunity has disappeared. But because strategy matters more than ever. This P

Palm Valley STR Case Study: $100K+ Annual Revenue, Top 5% Airbnb Ranking & Strategic Bonus Depreciation Planning in Goodyear, AZ

Palm Valley | Goodyear, Arizona There are short-term rentals you “try.” And there are assets you engineer. This Palm Valley investment was structured around three core pillars: Durable, layered demand Guest-experience differentiation Tax-aligned acquisition strategy The outcome? A fully remodeled 5-

Short-Term Rental Tax Loophole (2026): How to Offset W-2 Income with Bonus Depreciation

A structured guide for high-income W-2 earners on the short-term rental tax strategy — covering the IRS 7-day rule, material participation, cost segregation, and 100% bonus depreciation to potentially offset W-2 income. Updated March 2026. { "@context": "https://schema.org", "@type": "Article",

AI Bubble Risk Is Building in 2026: Why Strategic Investors Are Increasing Exposure to Real Estate

AI Spending, Valuation Risk, and Why Phoenix Real Estate Is Re-Emerging as a Strategic Hedge Artificial intelligence is driving one of the most aggressive capital investment cycles in modern financial history. Technology firms are deploying hundreds of billions of dollars into semiconductors, advanc

Why Phoenix Is One of the Best Places to Live, Buy, and Invest in Real Estate in 2026

A Deep Look at Economic Growth, Housing Opportunity, and Long-Term Market Strength Updated for 2026 market conditions Over the past decade, the Greater Phoenix Metro has undergone a quiet but powerful transformation. Once viewed primarily as a fast-growing Sun Belt city driven by affordability and l

North Scottsdale Client Win: How Strategic Positioning Sold a Non-Updated Home in a Gated Community

In today’s North Scottsdale real estate market, it’s not unusual to see multiple single-family homes competing for the same buyers — often within the same gated communities, price ranges, and neighborhoods. Similar floor plans. Similar lot sizes. Similar asking prices. Yet some homes sell quickly —

Phoenix Housing Market 2026: Supply, Demand, Interest Rates, and What Buyers and Sellers Should Expect

Data and observations reflect market conditions across Greater Phoenix as of early January 2026. The start of 2026 has brought a noticeable shift in the Greater Phoenix housing market. While headline numbers may suggest conditions look similar to a year ago, the underlying dynamics tell a more nuanc

Scottsdale 85254 Turn-Key Short Term Rental (STR) Case Study (2026): $170K Below List and Bonus Depreciation

A Turn-Key Short-Term Rental Acquired $170K Below List — With a Bonus Depreciation Strategy Built In From Day One Fully furnished. Already earning. A brand-new roof and seller-paid closing costs. A tax framework mapped out before the first property tour. Eric Ravenscroft, CRS Real Estate Strategist

How a California Investor Turned a $2M Property Into Stronger Cash Flow With Half the Risk in Arizona (2026)

A California investor sold a $2M multifamily property and used a 1031 exchange to redeploy that capital into two single-family rentals in Vistancia (Peoria) and Verrado (Litchfield Park), Arizona — increasing monthly rent by $1,000, cutting the annual property tax bill by 75%, and eliminating rent c

Why Most Buyers Choose the Wrong House and How the Right Real Estate Agent Helps

Buying a home is one of the most significant financial decisions most people will ever make. Yet many buyers don’t realize they’ve chosen the wrong house until years later — not at the closing table, but after life changes, costs compound, or flexibility disappears. The issue usually isn’t poor judg

Builder Incentives on New Builds in Phoenix: What Buyers Should Know

Last updated: December 2025 to reflect current Phoenix Metro new construction incentive trends. Builder incentives are nothing new in real estate. Interest rate buydowns, closing cost assistance, and design center credits have long been tools used to move inventory — particularly homes that are alre

Selling a Home in Phoenix in 2026? What to Know About Timing, Options, and What’s Actually Working

The Phoenix real estate market isn’t broken — it’s just different. As we move toward 2026, more homeowners are starting to ask questions. Not because they’re ready to sell tomorrow, but because they want to understand how today’s market works, what timing looks like, and what options exist if sellin

A Rare Mesa Arizona Home Offering Lifestyle Flexibility and $120K+ Short-Term Rental Potential

Homes that genuinely support multiple living and income strategies are becoming increasingly rare — especially in established Mesa neighborhoods where lot size, layout flexibility, and zoning advantages already exist. That’s exactly what sets 5255 E Greenway Circle in Mesa, Arizona (85205) apart. Th

THE YEAR-END ADVANTAGE: Why December Is the Most Powerful Time of Year to Buy Real Estate in Phoenix

A comprehensive guide to tax strategy, new construction incentives, resale negotiation power, and the real opportunities behind Phoenix’s year-end market surge. 📌 Table of Contents Why Year-End Is the Strongest Window of the Year Builder Incentives: Why December Is Their Most Aggressive Month Resal

Phoenix Housing Market Update 2025: Year-End Surge, Falling Payments, and What Buyers & Sellers Need to Know

**Inside the Final Chapter of Phoenix Real Estate in 2025** (Prefer to listen instead? Catch the full breakdown on the latest episode of The House of Ravenscroft Podcast.) As 2025 winds down, the Greater Phoenix real estate market is entering one of its most active—and most strategic—phases of the y

5608 W Soft Wind Drive Sold $1,313,000 Cash | Rare Basement Home | Saddleback Foothills Glendale AZ | The Ravenscroft Group

Rare 5,565 sq ft basement home at 5608 W Soft Wind Drive, Saddleback Foothills, Glendale AZ sold $1,313,000 cash with zero concessions. Out-of-state buyer sourced via targeted campaign. 20 verified private showings. Full case study by Eric Ravenscroft, CRS — The Ravenscroft Group. The Ravenscrof

The 50-Year Mortgage Debate: Smart Innovation or Bad Idea? What Buyers Must Know About Portable Mortgages & Affordability

There’s been a lot of noise lately about two concepts that are shaking up the housing world:the 50-year mortgage andthe portable mortgage. Depending on which headline you follow, these ideas are either: 👉 “The end of responsible homeownership,”or👉 “The solution to America’s affordability crisis.”

The Truth About Phoenix Real Estate: Myths, Misconceptions, and What Buyers & Sellers Need to Know As We Near the End of 2025

The Phoenix Metro has become one of the most influential and closely watched real estate markets in the country. With rapid population growth, major corporate relocations, rising new construction, and national attention on Arizona’s affordability, it’s no surprise that Phoenix attracts both new resi

Why Planning for 2026 Could Be the Most Important Financial Move You Make

Most people wait until January to think about planning. But by then, opportunity has already passed them by. The truth is, the most successful homeowners, investors, and professionals don’t just react to changes — they anticipate them. And with 2026 bringing new tax laws, market shifts, and investme